| This article reviews India’s merchandise trade performance

during April-March 2012-13 on the basis of the data

released by the Directorate General of Commercial

Intelligence and Statistics (DGCI&S). It also analyses

disaggregated commodity-wise and direction-wise details

during April-December 2012.

Highlights

The stress on the external sector persisted in

2012-13 as India’s trade deficit continued to grow.

While merchandise export performance remained

subdued, import growth decelerated. However, owing

to a sharp decline in exports, the trade deficit widened

to US$ 190.9 billion in 2012-13 as compared with US$

183.4 billion in 2011-12. The contraction in exports

was more on account of decline in exports of

manufactured goods, especially engineering goods and

labour intensive sectors such as gems and jewellery.

A major factor that weighed on India’s external

demand was the subdued global demand conditions

as export to destinations like EU and China declined

considerably. In the wake of subdued global trade

conditions, domestic policy efforts aimed at diversifying

exports to other emerging countries also did not seem

to have given much impetus to India’s exports. Major

highlights of India’s trade performance during 2012-13

are set out below:

-

India’s merchandise exports stood at US$ 300.6

billion in 2012-13, showing a decline of 1.8 per

cent as compared to a growth of 21.8 per cent in

2011-12 amounting to US$ 306.0 billion.

-

Commodity-wise disaggregated figures reveal that

the setback in merchandise exports in 2012-13

was led by decline in exports of manufacturing items like engineering goods, textiles, gems &

jewellery and also primary products like iron ore

and minerals.

-

Lackluster performance of India’s exports mainly

reflected the sluggish global demand as exports to

almost all the major destinations, particularly, EU,

UAE, US and China either declined or showed a

lower growth.

-

Imports during the year grew by 0.4 per cent to

US$ 491.5 billion as against a growth of 32.3 per

cent in 2011-12 (US$ 489.3 billion).

-

While the overall imports grew by only 0.4 per

cent, oil imports showed a rise of 9.3 per cent.

Other components such as gold and non-oil non

gold imports declined by 4.8 per cent and 3.4 per

cent, respectively.

I. India’s Merchandise Trade

Exports (April-March 2012-13)

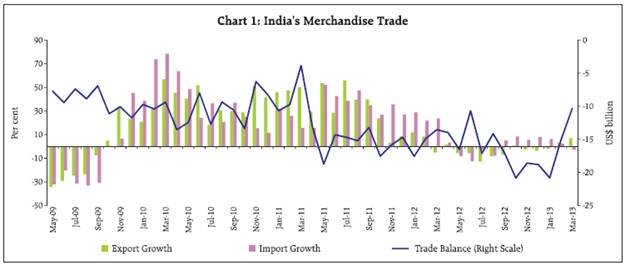

India’s exports showed a decline of 1.8 per cent

in FY 2012-13. Owing to the global uncertainties and

weak external demand, export contraction was largely

evident in H1 of 2012-13. However, since December

2012, export growth has turned positive which may be

reflecting the modest increase in trade activities across

emerging markets and developing economies (EMDEs)

as well as the impact of promotional measures

undertaken by the Government (Box 1) and the Reserve

Bank of India during 2012-13 (Chart 1).

On a cumulative basis, however, merchandise

exports stood at US$ 300.6 billion, declining by 1.8 per

cent, in FY 2012-13 as compared to the export of US$

306.0 billion in FY 2011-12 (21.8 per cent) (Table 1).

Commodity-wise and Destination-wise Exports

(April-December 2012)

Disaggregated commodity-wise data show that

exports remained subdued across all major commodity

groups. Within manufacturing sector, which accounted for nearly 62 per cent of India’s exports, exports of

engineering goods, textiles & textile products and gems & jewellery showed a contraction while that of

chemicals & related products showed a decelerated growth during April-December 2012. Owing mainly to

the subdued demand conditions in the EU countries and the US, exports of engineering goods declined by

5.0 per cent as against a rise of 17.6 per cent a year ago.

Labour intensive sectors like gems and jewellery and

handicrafts also recorded a negative growth of 5.5 per

cent and 11.2 per cent, respectively in April-December

2012-13 as against a respective growth of 30.1 per cent

and 23.1 per cent in the corresponding period of

previous year.

Box 1: Recent Policy Measures to Promote India’s Exports

Global trade conditions remained subdued in 2012 and

India’s exports were severely impacted. Keeping in view

the reduced global demand in general and advanced

economies in particular, the Government of India took

additional measures during 2012-13 (June 5 and December

26). Measures announced in December 2012 mainly

included (i) extension of interest subvention scheme for

select employment oriented sectors (including SMEs in all

sectors) upto end-March 2014, (ii) introduction of pilot

scheme of 2 per cent interest subvention for project exports

through EXIM Bank for countries of SAARC region, (iii)

broadening the scope of Focus Market Scheme and Special

Focus Market Scheme, Market Linked Focus Product Scheme

(MLFPS) and (iv) incentive on incremental exports to USA,

EU and countries of Asia during the period January-March

2013 over the base period.

On April 18, 2013, a package of measures was announced

by the Ministry of Commerce and Industry as part of the

Foreign Trade Policy to revive investors’ interest in SEZs

and to boost exports. Besides, zero duty Export Promotion

Capital Goods (EPCG) scheme and 3 per cent EPCG scheme

have been combined into one scheme which will be zero

duty EPCG scheme covering all sectors subject to certain

conditions. Other major measures announced were the

following:

-

Export obligation for domestic sourcing of capital goods

has been reduced by 10 per cent to promote domestic

manufacturing of capital goods. Export obligation for

under EPCG scheme for units in Jammu & Kashmir has

been reduced.

-

Interest subvention scheme has further widened to

include items covered under Chapter 63 of ITC (HS)

(other made up textile articles, sets, rags) and additional

specified tariff lines of engineering sector items under

the scheme. These sectors would be able to avail benefit

under this scheme during the period from May 2013

March 2014.

-

Scope of Market and Product Diversification schemes

has been broadened. Norway has been added under

Focus Market Scheme and Venezuela has been added

under Special Focus Market Scheme. The total number

of countries under Focus Market Scheme and Special

Focus Market Scheme becomes 125 and 50 respectively.

-

Approximately, 126 new products have been added under

Focus Product Scheme. These products include items

from engineering, electronics, and chemicals,

pharmaceuticals and textiles sector.

-

About 47 new products have been added under Market

Linked Focus Product Scheme (MLFPS). These products

are from engineering, auto components and textiles

sector. 2 new countries, i.e., Brunei and Yemen have been

added as new markets under MLFPS.

-

The scope of Incremental Export Incentivisation Scheme

has been increased. This scheme, available for exports

made to USA, EU and Asia, has been extended for the

year 2013-14. The Government has also agreed to include

53 countries of Latin America and Africa to increase

India’s share in these markets.

Table 1: India’s Merchandise Trade |

(US$ billion) |

Items |

April–March |

2011-12 R |

2012-13P |

1 |

2 |

3 |

Exports |

306.0 |

300.6 |

|

(21.8) |

(-1.8) |

Of which: Oil |

56.0 |

60.0 |

|

(35.1) |

(7.1) |

Non-oil |

249.9 |

240.6 |

|

(19.2) |

(-3.7) |

Gold |

6.7 |

6.5 |

|

(10.8) |

(-3.1) |

Non-Oil Non-Gold |

243.2 |

234.1 |

|

(19.5) |

(-3.8) |

Imports |

489.3 |

491.5 |

|

(32.3) |

(0.4) |

Of which: Oil |

155.0 |

169.4 |

|

(46.2) |

(9.3) |

Non-oil |

334.4 |

322.1 |

|

(26.7) |

(-3.6) |

Gold |

56.5 |

53.8 |

|

(39.2) |

(-4.8) |

Non-Oil Non-Gold |

277.9 |

268.4 |

|

(24.5) |

(-3.4) |

Trade Deficit |

-183.4 |

-190.9 |

Of which: Oil |

-98.9 |

-109.4 |

Non-oil |

-84.4 |

-81.6 |

Non-Oil Non-Gold |

-34.7 |

-34.4 |

Source: DGCI&S |

Among other major categories, exports of

petroleum products and primary products showed

substantially lower growth during April-December 2012

as compared with the corresponding period of 2011-12

(Table 2). Among the primary products, exports of iron

ore continued to decline attributing to increase in

freight charges, ban on mining activity in certain states,

coupled with the hefty export duty levied by the

government and differential freight rate imposed by

the railways. Some minor sectors, however, recorded a

positive growth during this year which mainly include

tobacco, processed mineral, manufacture of metals and

carpets.

Destination-wise export data reveal that there has

been a significant change in the composition of India’s trade during April-December 2012 (Table 3). Exports to

major destinations such as EU, UAE, US and China

showed either a decline or lower growth during this

period. Decline in exports to China was evident mainly

on account of substantial fall in exports of cotton, ores,

iron and steel and petroleum products. However,

export to countries like Iran, Iraq, Saudi Arabia, Russia

and some African countries, particularly, Egypt, Kenya

showed considerable uptrend. Exports to Saudi Arabia

increased by 75.5 per cent mainly reflecting growing

demand for items relating to mineral fuels, mineral

oils and products of their distillation, bituminous

substances, mineral waxes and organic chemicals.

Table 2: India’s Exports of Principal Commodities |

(Per cent) |

Commodity Group/ Period |

Percentage Share |

Relative Weighted Variation |

2011-12 |

2010-11 |

2011-12 |

2012-13 |

2011-12 |

2012-13 |

April-December |

April-December |

Primary Products |

15.0 |

13.3 |

13.9 |

15.1 |

4.8 |

0.6 |

Agriculture and Allied Products |

12.2 |

9.4 |

11.3 |

13.2 |

5.2 |

1.4 |

Ores and Minerals |

2.8 |

3.8 |

2.7 |

1.9 |

-0.4 |

-0.9 |

Manufactured Goods |

60.6 |

63.0 |

60.5 |

61.6 |

15.4 |

-1.4 |

Leather and Manufactures |

1.6 |

1.6 |

1.6 |

1.7 |

0.5 |

-0.01 |

Chemicals and Related Products |

12.1 |

11.7 |

12.0 |

13.5 |

3.8 |

1.0 |

Engineering Goods |

22.2 |

24.5 |

22.2 |

22.0 |

4.3 |

-1.1 |

Textiles and Textile Products |

9.2 |

9.7 |

9.1 |

9.0 |

2.1 |

-0.5 |

Gems and Jewellery |

14.7 |

14.6 |

14.7 |

14.4 |

4.4 |

-0.8 |

Petroleum Products |

18.3 |

16.2 |

18.7 |

20.2 |

8.0 |

0.7 |

Others |

6.1 |

7.5 |

6.9 |

3.1 |

1.4 |

-3.9 |

Total |

100 |

100 |

100 |

100 |

29.6 |

-4.0 |

Source: Compiled from DGCI&S data. |

Table 3: India’s Exports to Principal Regions |

(Percentage Shares) |

Region/Country |

2010-11 |

2011-12 |

2011-12 |

2012-13 |

April-March |

April-December |

1 |

2 |

3 |

4 |

5 |

I. OECD Countries |

33.2 |

33.8 |

33.7 |

34.6 |

EU |

18.3 |

17.2 |

17.5 |

16.8 |

North America |

10.6 |

12.0 |

11.9 |

13 |

US |

10.1 |

11.4 |

11.2 |

12.3 |

Asia and Oceania |

2.8 |

3.0 |

2.6 |

3 |

Other OECD Countries |

1.5 |

1.6 |

1.7 |

1.8 |

II. OPEC |

21.3 |

19.0 |

18.5 |

21 |

III. Eastern Europe |

1.1 |

1.1 |

1.1 |

1.3 |

IV. Developing Countries |

38.2 |

40.8 |

40 |

41.5 |

Asia |

27.9 |

29.7 |

29.1 |

28.3 |

SAARC |

4.6 |

4.4 |

4.2 |

5 |

Other Asian Developing Countries |

23.3 |

25.3 |

24.9 |

23.3 |

People’s Republic of China |

6.2 |

6.0 |

5.8 |

4.5 |

Africa |

6.3 |

6.7 |

6.5 |

8.1 |

Latin America |

4.0 |

4.4 |

4.4 |

5.1 |

V. Others / Unspecified |

6.2 |

5.3 |

6.7 |

1.6 |

Total Exports |

100 |

100 |

100 |

100 |

Source: Compiled from DGCI&S data. |

In terms of share in India’s total merchandise

exports, the share of EU and China declined significantly

during April-December 2012. In contrast, the share of

other important export destinations, viz. , the US and

UAE, exhibited increase in April-December 2012 over

the corresponding period of 2011-12. Similarly, the

share of Africa and Latin America also increased.

Table 4: Growth Performance of Major Trade

Partner Economies |

(Per cent) |

Period |

2011 |

2012 Q1 |

2012 Q2 |

2012-Q3 |

2012-Q4 |

2013-Q1 |

Country |

|

|

|

|

|

|

Japan |

-0.6 |

3.2 |

4.0 |

0.4 |

0.4 |

0.0 |

Euro area |

1.4 |

-0.1 |

-0.5 |

-0.7 |

-0.9 |

-1.0 |

United States |

1.8 |

2.4 |

2.1 |

2.6 |

1.7 |

1.8 |

China |

9.3 |

8.1 |

7.6 |

7.4 |

7.9 |

7.7 |

Hong Kong |

4.9 |

0.7 |

0.9 |

1.5 |

2.8 |

2.8 |

Singapore |

5.2 |

1.5 |

2.3 |

0.0 |

1.5 |

-0.6 |

Korea |

3.6 |

2.9 |

2.3 |

1.5 |

1.4 |

1.5 |

Indonesia |

6.5 |

6.3 |

6.3 |

6.2 |

6.1 |

6.0 |

Malaysia |

5.1 |

5.1 |

5.6 |

5.3 |

6.5 |

4.1 |

Brazil |

2.7 |

0.7 |

0.4 |

0.9 |

1.4 |

– |

South Africa |

3.5 |

2.4 |

2.8 |

2.6 |

2.3 |

– |

– : Not Available.

Note: Growth Rates are seasonally adjusted (except for Hong Kong,

Singapore and Malaysia).

Source: OECD, IMF, Singstat database, Monthly Statistical Bulletin Bank

Negara Malaysia. |

Country-wise analysis shows that impact on

India’s exports was more pronounced mainly in

countries where domestic growth was subdued in 2012,

except Indonesia and Malaysia where domestic growth

was broadly intact (Table 4). Moderation in exports to

these countries was mainly evident in petroleum

products; ships, boats and floating structures (only

Indonesia); chemical and related products; articles of

iron & steel and electrical machinery. Overall, EU and

countries in developing Asia accounted for nearly threefourth

of decline in India’s exports.

Imports (April-March 2012-13)

Merchandise imports in the FY 2012-13 recorded

a marginal growth of 0.4 per cent amounting to

US$ 491.5 billion compared to a growth rate of 32.3

per cent at US$ 489.3 billion. The decline was mainly

led by a fall in gold and non-oil non-gold imports. Fall

in non-oil non-gold was more on account of a slowdown

in domestic activity and dampened demand for export

related items. Notwithstanding a marginal decline in

the international prices of crude oil (Indian basket),

imports of POL items registered a growth of 9.3 per cent in 2012-13 reflecting growing domestic

consumption of petroleum products (Table 6).

Table 5: Region-wise Relative Weighted Variation in

India’s Export Growth |

(Per cent) |

|

2010-11 |

2011-12 |

2012-13 |

April- December |

EU |

4.0 |

4.9 |

-1.4 |

North America |

3.2 |

4.7 |

0.6 |

Other OECD |

0.6 |

0.7 |

0.0 |

OPEC |

7.1 |

3.4 |

1.7 |

Eastern Europe |

0.5 |

0.3 |

0.2 |

Developing Asia |

10.2 |

9.1 |

-1.9 |

Africa |

3.0 |

1.9 |

1.2 |

Latin America |

2.3 |

1.7 |

0.5 |

Others |

6.5 |

0.8 |

-5.2 |

Total Exports |

37.4 |

27.5 |

-4.3 |

Source: Compiled from DGCI&S data. |

Commodity-wise and Destination-wise Imports

(April-December 2012)

Disaggregated commodity-wise import data

available for April-December 2012 show that among the

principal commodities, ‘petroleum, petroleum and

related material’ and gold & silver accounted for about

34 per cent and 10.8 per cent of India’s merchandise

imports, respectively. A growth of 12.3 per cent in POL products was mainly on account of rise in quantum of

imports given a marginal decline in the international

price of crude oil (Indian basket). The decline in gold

demand was witnessed mainly in H1 of 2012-13 which

may be attributed to the rise in customs duty and

various other measures to curb gold demand undertaken by the Government and the Reserve Bank of India. Gold

imports, however, have shown a sharp pick up since

November 2012 (except in March 2013). Among other

components, imports of capital goods, accounting for

18.8 per cent of total merchandise imports, declined

by 7.1 per cent owing to the slower investment activity

in domestic economy. Import of export related items

like ‘pearl precious semi-precious stones, chemicals,

textile yarn and cashew nuts also recorded either a

decline or a lower growth during this period (Table 7).

Table 6: Trends in Crude Oil prices |

(US$/barrel) |

Period |

Dubai |

Brent |

WTI* |

Indian Basket** |

1 |

2 |

3 |

4 |

5 |

2005-06 |

53.4 |

58.0 |

59.9 |

55.7 |

2006-07 |

60.9 |

64.4 |

64.7 |

62.5 |

2007-08 |

77.3 |

82.3 |

82.3 |

79.2 |

2008-09 |

82.1 |

84.7 |

85.8 |

83.6 |

2009-10 |

69.6 |

69.8 |

70.6 |

69.8 |

2010-11 |

84.2 |

86.7 |

83.2 |

85.1 |

2011-12 |

109.4 |

113.9 |

96.8 |

111.9 |

2012-13 |

106.9 |

110.5 |

92.0 |

108.0 |

2012-13 (Q1) |

106.2 |

108.9 |

93.4 |

106.9 |

2012-13 (Q2) |

106.2 |

110.0 |

92.2 |

107.4 |

2012-13 (Q3) |

107.2 |

110.5 |

88.1 |

108.3 |

2012-13 (Q4) |

108.0 |

112.9 |

94.3 |

109.6 |

* West Texas Intermediate

** the composition of Indian Basket of Crude represents Average of Oman & Dubai for sour grades and Brent (Dated) for sweet grade in the ratio of

68.2: 31.8 for 2012-13.

Sources: International Monetary Fund, International Financial Statistics,:

World Gem data & commodity: Ministry of Petroleum and Natural Gas,

Government of India. |

Table 7: Imports of Principal Commodities |

(Per cent) |

Commodity Group/Period |

2011-12 |

Percentage Share |

Relative Weighted variation |

2010-11 |

2011-12 |

2012-13 |

2011-12 |

2012-13 |

April-December |

April-December |

1. Petroleum, Crude and Products |

31.7 |

27.9 |

30.5 |

34.3 |

13.3 |

3.8 |

2. Capital Goods |

20.3 |

21.7 |

20.2 |

18.8 |

5.7 |

-1.4 |

3. Gold and Silver |

12.5 |

11 |

12.6 |

10.8 |

6.1 |

-1.8 |

4. Organic and Inorganic Chemicals |

3.9 |

4.2 |

3.9 |

4 |

1 |

0.1 |

5. Coal, Coke and Briquettes, etc. |

3.6 |

2.9 |

3.7 |

3.3 |

2.1 |

-0.4 |

6. Fertilisers |

2.4 |

2.3 |

2.6 |

2.1 |

1.2 |

-0.5 |

7. Metalliferrous Ores, Metal Scrap, etc. |

2.7 |

2.7 |

2.8 |

3.0 |

1.1 |

0.1 |

8. Iron and Steel |

2.5 |

2.9 |

2.5 |

2.3 |

0.4 |

-0.2 |

9. Pearls, Precious and Semi-Precious Stones |

5.7 |

8.4 |

6.1 |

4.3 |

-0.2 |

-1.8 |

10. Others |

14.7 |

16 |

15.1 |

17.1 |

4.5 |

2.0 |

Total Imports |

100 |

100 |

100 |

100 |

35.2 |

-0.1 |

Source: Compiled from DGCI&S data. |

Destination-wise data for India’s imports show

that India’s imports from EU, China, US, Australia, Hong

Kong and Singapore declined during April-December

2012. In contrast, import from Saudi Arabia, UAE, Iraq

and Kuwait, mainly the oil exporters, remained

positive. Growth in imports from Latin American

countries was significantly higher during the period as

compared with corresponding period of 2011-12. For

instance, increase in imports from Brazil has mainly

on account of sugar and sugar confectionery, items

relating to animal or vegetable fats and oils.

Even though there was a decline in import from

China, it continued to be the main import source

accounting for 11.3 per cent of India’s merchandise

imports. Other major source countries for import

include UAE, Saudi Arabia, Switzerland and USA with

a share of 7.8 per cent, 6.8 per cent, 5.5 per cent and

5.1 per cent, respectively. While the share of countries

like USA, EU and Switzerland in India’s total imports

declined in April-December 2012, the share of OPEC

countries (including UAE) and Latin American showed

a rise compared to the corresponding period a year ago

(Table 8).

Trade Deficit

Sharper deceleration in merchandise export than

imports led to a widening of trade deficit which

increased to US$ 190.9 billion in 2012-13 as against US$

183.4 billion in 2011-12. POL and gold together

accounted for 45.4 per cent of India’s merchandise imports and 117 per cent of merchandise trade deficit

during this period. Even though gold imports have

shown decline in 2012-13, they were still at a high level

and thus a cause for concern for India’s high trade

deficit.

Table 8: Shares of Groups/Countries in

India’s Imports |

(Percentage Shares) |

Region/Country |

2010-11 |

2011-12 |

2011-12 |

2012-13 |

April-March |

April-December |

1 |

2 |

3 |

4 |

5 |

I. OECD Countries |

30.6 |

30.2 |

30.4 |

27.7 |

EU |

12.0 |

11.9 |

12.0 |

10.9 |

France |

1.0 |

0.9 |

0.8 |

0.8 |

Germany |

3.2 |

3.3 |

3.4 |

3.0 |

UK |

1.5 |

1.6 |

1.6 |

1.4 |

North America |

6.0 |

5.6 |

5.8 |

5.6 |

US |

5.4 |

5.0 |

5.2 |

5.1 |

Asia and Oceania |

5.4 |

5.7 |

5.7 |

5.2 |

Other OECD Countries |

7.2 |

7.0 |

6.9 |

5.9 |

II. OPEC |

33.6 |

35.5 |

34.4 |

38.6 |

III. Eastern Europe |

1.5 |

1.7 |

1.6 |

1.9 |

IV. Developing Countries |

33.0 |

32.3 |

33.2 |

31.5 |

Asia |

27.1 |

25.9 |

26.9 |

24.6 |

SAARC |

0.6 |

0.5 |

0.5 |

0.6 |

Other Asian Developing |

26.5 |

25.3 |

26.3 |

24.0 |

Countries |

|

|

|

|

of which: |

|

|

|

|

People’s Republic of China |

11.8 |

11.8 |

12.4 |

11.3 |

Africa |

3.6 |

4.0 |

4.1 |

3.8 |

Latin America |

2.4 |

2.4 |

2.3 |

3.1 |

V. Others / Unspecified |

1.3 |

0.3 |

0.3 |

0.3 |

Total |

100 |

100 |

100 |

100 |

Source: Compiled from DGCI&S data. |

II. Trends in Global Trade

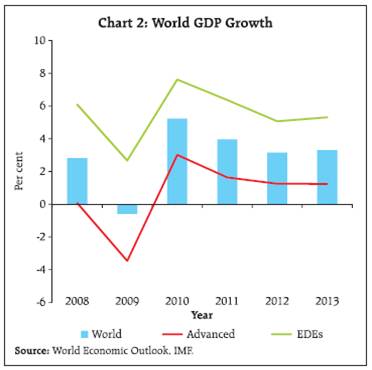

As the global recovery slowed further in 2012, it

mirrored in decelerating world trade growth (Chart 2).

The world trade remained sluggish as the economic

slowdown in global import demand in EU countries

and some other major economies remained suppressed.

Subdued demand conditions in EU economies affected

not only intra-EU trade but also fed through other

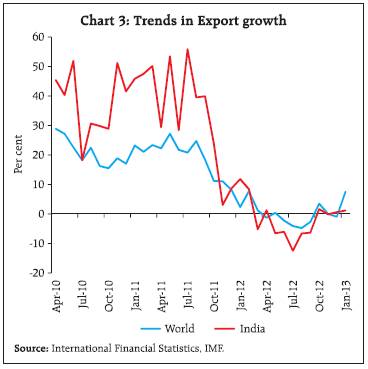

advanced countries and EMDEs. However, the global

trade cycle has shown incipient signs of recovery across

few EMDEs since the terminal quarter of 2012 (Chart 3). Nevertheless, overall world trade volume

could grow by 2.5 per cent in 2012 as compared with

6.0 per cent in 2011. Going forward, trade prospects

are expected to improve moderately. According to the

IMF (2013), the world trade volume (goods and services)

is projected to grow by 3.6 per cent in 2013. Similarly,

the WTO projects a growth of 3.3 per cent in world

goods trade volume in 2013 (2.2 per cent in 2012). However, such forecasts are subject to risks that may

emanate from divergent economic outlook for the US

and EU.

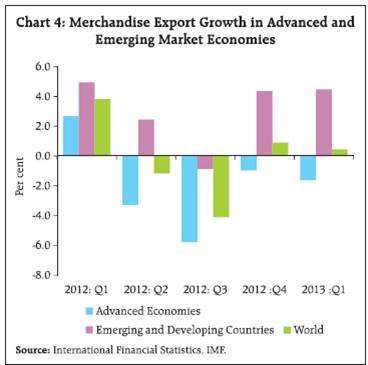

Chart 4 illustrates the divergent trade performances

of advanced and EMDEs economies over the course of

2012 and in Q1 of 2013. Slow growth in the advanced

economies (AEs) continued to remain a weak link in

global trade expansion, while EMDEs seem to be

contributing to global trade through increased intraindustry

and South-South trade. While the EMDEs

seem to have maintained export growth momentum

in Q1 of 2013, the decline in export growth in AEs has

become more pronounced as compared with the

previous quarter.

Even though there were incipient signs of

strengthening of some major economies, international

prices of most industrial commodities have eased since

mid-February 2013 (Chart 5). International crude oil

prices softened in Q1 of 2013 largely due to improved

supplies from the North Sea basin and slowing demand

from European refineries approaching their seasonal

maintenance cycle. Similarly, the prices of basic metal

have reversed their upward trend reflecting oversupply and growing inventories in recent months. Although

international food prices have followed mixed trends

in Q1 of 2013, better-than-expected global stocks

reported by the US Department of Agriculture and

improved production prospects of wheat led to easing

in grain prices in recent months.

III. Outlook

As mentioned earlier, India’s exports have shown

positive growth since December 2012. However, the

sustenance of the positive export growth momentum

would continue to depend on demand and growth

prospects of trading partner economies. According to

the WTO assessment on world trade prospects,

indicators of production and business sentiment in the

first quarter of 2013 present a mixed picture of current

economic conditions. Since the global growth is projected to pick up only marginally and key risks to

global economy still prevail, India’s export growth is

projected to pick up at a modest pace at best. Softening

trend in international prices of POL and gold,

supplemented by various measures undertaken by the

Government and the Reserve Bank to reduce imports

of these two items may bode well for containing import

growth. Since the signs of global recovery are not so

certain, sustaining Indian export recovery would be a

challenge that needs efforts to raise productivity-based

competitiveness.

Detailed information on monthly commodity-wise

and country-wise data on merchandise exports and

imports for 2011-12 and 2012-13 can be accessed at

http://www.rbi.org.in/scripts/BS_PressReleaseDisplay.aspx.

|