On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (October 9, 2020) decided to: - keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

Consequently, the reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent. - The MPC also decided to continue with the accommodative stance as long as necessary – at least during the current financial year and into the next financial year – to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 2. Incoming data point to a recovery in global economic activity in Q3 of 2020 in sequential terms, although downside risks have risen with the renewed surge in infections in many countries. Global trade is expected to be subdued. The rebound could turn out to be stronger among advanced economies (AEs) than in emerging market economies (EMEs). Global financial markets remain supported by highly accommodative monetary and liquidity conditions. Soft fuel prices and weak aggregate demand have kept inflation below target in AEs, although in some EMEs, supply disruptions have imparted upward price pressures. Domestic Economy 3. On the domestic front, high frequency indicators suggest that economic activity is stabilising in Q2:2020-21 after the 23.9 per cent year-on-year (y-o-y) decline in real GDP in Q1 (April-June). Cushioned by government spending and rural demand, manufacturing – especially consumer non-durables – and some categories of services, such as passenger vehicles and railway freight, have gradually recovered in Q2. The outlook for agriculture is robust. With merchandise exports slowly catching up to pre-COVID levels and some moderation in the pace of contraction of imports, the trade deficit widened marginally sequentially in Q2. 4. Headline CPI inflation increased to 6.7 per cent during July-August 2020 as pressures accentuated across food, fuel and core constituents on account of supply disruptions, higher margins and taxes. One year ahead inflation expectations of households suggest some softening in inflation from three months ahead levels. Selling prices of firms remain muted, reflecting the weak demand conditions. 5. Domestic financial conditions have eased substantially, with systemic liquidity remaining in large surplus. Reserve money increased by 13.5 per cent on a year-on-year basis (as on October 2, 2020), driven by a surge in currency demand (21.5 per cent). Growth in money supply (M3), however, was contained at 12.2 per cent as on September 25, 2020. Banks’ non-food credit growth remains subdued. India’s foreign exchange reserves stood at US$ 545.6 billion on October 2, 2020. Outlook 6. Turning to the outlook for inflation, kharif sowing portends well for food prices. Pressures on prices of key vegetables like tomatoes, onions and potatoes should also ebb by Q3 with kharif arrivals. On the other hand, prices of pulses and oilseeds are likely to remain firm due to elevated import duties. International crude oil prices have traded with a softening bias in September on a weak demand outlook, but domestic pump prices may remain elevated in the absence of any roll back of taxes. Pricing power of firms remains weak in the face of subdued demand. COVID-19-related supply disruptions, including labour shortages and high transportation costs, could continue to impose cost-push pressures, but these risks are getting mitigated by progressive easing of lockdowns and removal of restrictions on inter-state movements. Taking into consideration all these factors, CPI inflation is projected at 6.8 per cent for Q2:2020-21, at 5.4-4.5 per cent for H2:2020-21 and 4.3 per cent for Q1:2021-22, with risks broadly balanced (Chart 1). 7. Turning to the growth outlook, the recovery in the rural economy is expected to strengthen further, while the turnaround in urban demand is likely to be lagged in view of social distancing norms and the elevated number of COVID-19 infections. While the contact-intensive services sector will take time to regain pre-COVID levels, manufacturing firms expect capacity utilisation to recover in Q3:2020-21 and activity to gain some traction from Q4 onwards. Both private investment and exports are likely to be subdued, especially as external demand is still anaemic. Taking into consideration the above factors and the uncertain COVID-19 trajectory, real GDP growth in 2020-21 is expected to be negative at (-)9.5 per cent, with risks tilted to the downside: (-)9.8 per cent in Q2:2020-21; (-)5.6 per cent in Q3; and 0.5 per cent in Q4. Real GDP growth for Q1:2021-22 is placed at 20.6 per cent (Chart 2).  8. The MPC is of the view that revival of the economy from an unprecedented COVID-19 pandemic assumes the highest priority in the conduct of monetary policy. While inflation has been above the tolerance band for several months, the MPC judges that the underlying factors are essentially supply shocks which should dissipate over the ensuing months as the economy unlocks, supply chains are restored, and activity normalises. Accordingly, they can be looked through at this juncture while setting the stance of monetary policy. Taking into account all these factors, the MPC decides to maintain status quo on the policy rate in this meeting and await the easing of inflationary pressures to use the space available for supporting growth further. 9. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted for keeping the policy repo rate unchanged and continue with the accommodative stance as long as necessary to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to continue with this accommodative stance at least during the current financial year and into the next financial year, with Prof. Jayanth R. Varma voting against this formulation. 10. The minutes of the MPC’s meeting will be published by October 23, 2020. (Yogesh Dayal)

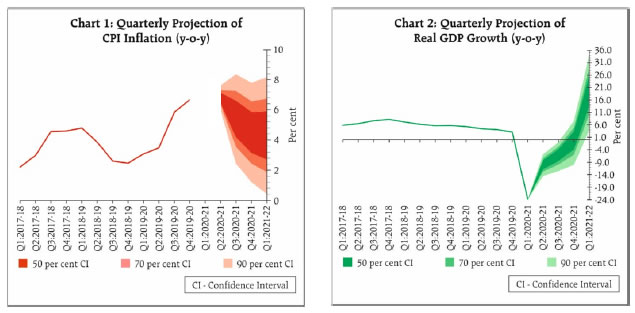

Chief General Manager Press Release: 2020-2021/453 |