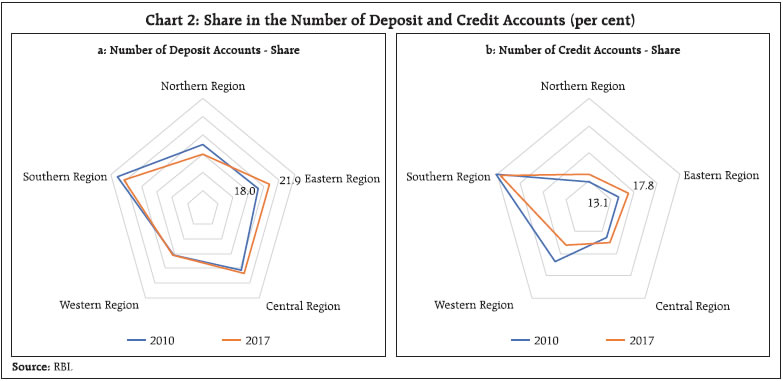

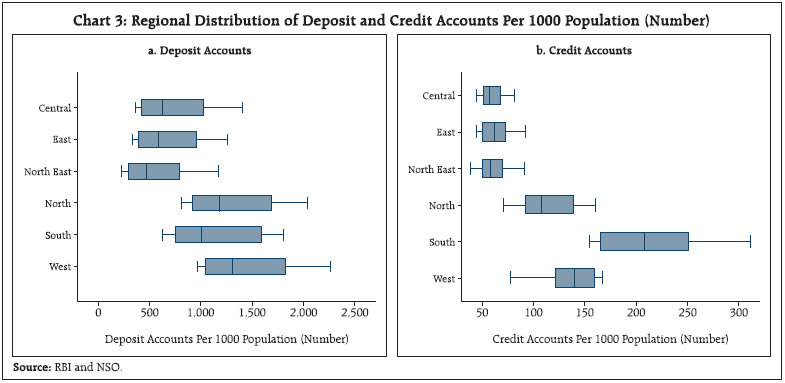

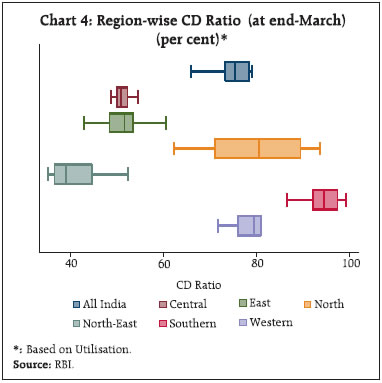

This article highlights that the eastern region of India continues to lag behind other regions in harnessing the potential of bank credit as an instrument to promote growth and development, notwithstanding concerted policy efforts to further financial inclusion in the region. While enhancing access to credit remains critical to strengthen credit penetration in the region, empirical findings suggest that factors influencing demand for credit – per capita income, level of industrial activity and availability of infrastructure such as road network and power supply – also matter. Introduction Access to financial services, in particular credit, is a well-established harbinger of economic prosperity. At the sub-national level in India, banking outreach in terms of penetration of credit, however, remains quite heterogeneous. Southern and western regions have witnessed relatively stronger penetration of credit with credit to deposit (CD) ratio of 93.2 per cent and 90 per cent, respectively, as at end-March 2018 coinciding with higher per capita income and relatively better levels of industrialisation. The eastern area (EA)1, especially the north-east, (with CD ratio of 44.1 per cent and 41 per cent, respectively) clearly lag behind, coterminous with their lower per capita income and weaker industrial base. Constricted financial inclusion of the EA, especially the north-eastern region (NER) has for long engaged the attention of various committees set up by the Government of India and Reserve Bank of India (RBI) [such as the Financial Sector Plan for NER (2006); Committee on Financial Inclusion (2008); Committee on Comprehensive Financial Services for Small Businesses and Low-income Households (2014); and Committee on Medium-term Path on Financial Inclusion (2015)]. For improving branch penetration, the Reserve Bank relaxed the branch authorisation policy in December 2009, specifically for the north-eastern states and Sikkim, and allowed domestic scheduled commercial banks (SCBs) to open branches in rural, semi-urban and urban centres without having the need to take permission from the Reserve Bank in each case2. While this policy push has brought about a significant improvement in usage of deposit services, credit intermediation, which is crucial for fostering growth, remains inadequate in the region. Against this backdrop, this article seeks to investigate empirically the factors influencing banking outreach in EA. Analysis suggests that relatively weaker credit penetration in the EA has coincided with its lower per capita income level, industrial activity as also inadequate availability of infrastructural facilities. Empirical estimation reveals that these factors have played a constraining influence on the extent of credit penetration in the region. This article uses a richer database for all states and 3 union territories.3 Section II highlights how the banking outreach parameters of the region compare vis-à-vis other regions of the country. Section III describes data used for empirical analysis, while section IV presents empirical findings. Section V concludes. II. Banking Outreach in the Eastern Area Access and usage of banking services in the EA appear disproportionate relative to its share in the population of the country and the geographical area.4 The average population served per bank branch in the EA remains higher (Chart 1). Between 2010 and 2017, the share of EA in total number of credit and deposit accounts in the country has improved significantly (Charts 2a and 2b). An analysis of distribution of the number of deposit and credit accounts per 1,000 population from 2005 also confirms a secular expansion in the usage of deposit and credit services during this period.5 However, the analysis also lays bare the regional disparity in banking penetration. the east and north-east regions lag behind the south, west and north regions in terms of median usage of financial services (Charts 3a and 3b). Given its developmental challenges, financial inclusion efforts in the country cannot succeed unless due attention is bestowed to the EA.6 Banking activity in the EA remains tilted towards deposit mobilisation, which far outweighs credit disbursement. While the share of the EA in outstanding bank deposits stood at 15.1 per cent, it was lower at 8.1 per cent for bank credit as at end-March 2018. Accordingly, credit-intermediation (credit-deposit ratio) in the eastern region has remained significantly lower (Chart 4). Despite its stronger agrarian orientation, not only does the region have the lowest share in agriculture credit disbursement, there has also been a slackening of pace in farm credit deployment by the SCBs in the last couple of years.

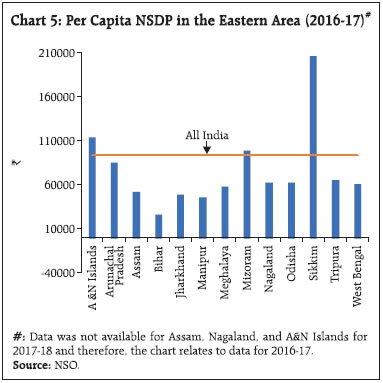

Empirical research on financial development suggests that while supply-oriented financial inclusion policies (like branch penetration) help foster the delivery of financial services (Burgess and Pande, 2005), demand dynamics, in turn, gets influenced by economic growth (Zang and Kim, 2007). Economic prosperity, in particular industrial development, plays a vital role in spurring the use of financial services in a region (Beck, et al, 2008; Rajan and Zingales, 1998). To this end, all the states of EA, barring Sikkim and Mizoram, are characterised by below national average per capita income (Chart 5). In terms of industrial development, lower figures for the number of factories per 1,000 population for the EA highlights the extent of gap that needs to be bridged for catching-up with the front-running regions (Chart 6).

Lower banking outreach of the EA could also be attributed to inadequate availability of physical infrastructure facilities such as roads and power, which create enabling conditions for boosting economic activity and thereby improve demand for banking services. Although road network has notably improved, situation remains less than satisfactory (Charts 7 and 8).

III. Data Description Banking penetration does not mean mere availability of more bank branches, usage of its services is equally important as it is the latter, which ultimately brings the desired results in terms of growth and development. Access to banking services implies only the availability aspect, which can be assessed through an indicator such as the number of bank branches per thousand population. Usage of banking services, in turn, can be gauged through the number of deposit and credit accounts per 1,000 population. For the analysis in this article, data, both on the access and usage indicators of banking services have been used. A rich sub-national annual database for 32 states and union territories (UTs) [excluding Lakshadweep, Dadra and Nagar Haveli, and Daman and Diu] for various indicators has been used (Table 1). The variables have been normalised appropriately. Per capita income captures the level of economic development of the state/ UT. Higher per capita income is expected to be associated with increased banking activity as people increasingly take recourse to financial transactions. Average population per bank branch (APPB) is the ratio of population to the total number of branches in the concerned state/ UT. A higher APPB implies greater population pressure on bank branches. | Table 1: Description of Variables | | Notations | Variables | Sources | | CDU | Credit-deposit ratio (per cent) | RBI | | CRAC | Number of credit accounts per thousand population | RBI and NSO | | DPAC | Number of deposit accounts per thousand population | RBI and NSO | | APPB | Average population per branch | RBI and NSO | | POWER | Per capita power availability (Kilowatt-Hour) | RBI and CEA | | ROAD | Road density (Length of road per square Km area) | RBI and NSO | | LOGPCI | Logarithm of per capita income | RBI | | FAC | Number of factories per ‘000 population | NSO | | INVCAP | Invested capital in factories per ‘000 population (Rupees) | NSO | | AGCR | Per capita agricultural credit (Rupees) | RBI and NSO | Number of factories per thousand population (FAC) is considered as a proxy for industrial activity. Pick-up in industrial activity is expected to foster banking transactions as salary disbursement, household savings and credit disbursals are made through deposit/credit accounts. Better access to power is expected to foster not only availability of banking services in the present era of core banking but also provide a fillip to industrialisation, economic activity and thereby generate a higher demand for financial services. Empirical evidence suggests the critical role of infrastructure in influencing banking outreach in major states of India (Ghosh, 2015). Availability of denser road network is expected to provide better regional connectivity and transportation facilities and thereby boost economic activity, individual income levels and banking activity. Improved agricultural credit offtake is expected to boost economic activity in rural areas and through inter-linkages generate demand impulses in other sectors and thereby reinvigorate demand for banking services. IV. Empirical Findings Summary statistics of the variables used in estimation suggests that the eastern area states/ UTs fare poorly across all parameters vis-à-vis corresponding all India figures (Table 2). CD ratio remains very low. The number of credit accounts and deposit accounts per 1,000 population remain about 60 per cent of all India averages during the period of analysis. From the policy perspective, it is important to understand the dynamics as to what factors influence banking outreach in the EA so that appropriate policy interventions could be made. | Table 2: Summary Statistics of Variables (2005 to 2018) | | Variables | Region | Mean | Std. Dev. | Min. | Max. | No. of Obs. | | CDU | All India | 58.8 | 25.0 | 23.2 | 133.7 | 448 | | CDU | Eastern Area | 42.2 | 13.3 | 23.2 | 113.9 | 182 | | CDU | North-East | 39.9 | 12.6 | 23.2 | 113.9 | 112 | | APPB | All India | 11608.5 | 6259.6 | 0.0 | 34879.3 | 448 | | APPB | Eastern Area | 14759.8 | 6908.1 | 0.0 | 34879.3 | 182 | | APPB | North-East | 14695.3 | 7904.8 | 0.0 | 34879.3 | 112 | | CRAC | All India | 104.7 | 74.5 | 20.3 | 522.0 | 432 | | CRAC | Eastern Area | 62.0 | 25.3 | 20.3 | 205.3 | 174 | | CRAC | North-East | 60.5 | 27.2 | 20.3 | 205.3 | 105 | | DPAC | All India | 900.5 | 641.5 | 0.6 | 3805.8 | 432 | | DPAC | Eastern Area | 541.9 | 342.8 | 0.6 | 1538.2 | 174 | | DPAC | North-East | 521.4 | 309.9 | 115.7 | 1538.2 | 105 | | POWER | All India | 825.0 | 578.8 | 78.0 | 3511.6 | 446 | | POWER | Eastern Area | 358.3 | 172.3 | 78.0 | 798.1 | 180 | | POWER | North-East | 354.2 | 165.2 | 134.4 | 798.1 | 111 | | ROAD | All India | 2.7 | 4.7 | 0.1 | 25.7 | 384 | | ROAD | Eastern Area | 1.4 | 1.2 | 0.2 | 4.2 | 156 | | ROAD | North-East | 1.4 | 1.2 | 0.2 | 4.2 | 96 | | PCI | All India | 10.6 | 0.5 | 9.0 | 12.2 | 342 | | PCI | Eastern Area | 10.4 | 0.5 | 9.0 | 11.6 | 138 | | PCI | North-East | 10.4 | 0.4 | 9.9 | 11.5 | 84 | | AGCR | All India | 5124.6 | 6805.4 | 177.8 | 55182.6 | 415 | | AGCR | Eastern Area | 1488.4 | 1027.4 | 177.8 | 6787.3 | 157 | | AGCR | North-East | 1239.2 | 787.4 | 177.8 | 4380.3 | 95 | | FAC | All India | 0.162 | 0.149 | 0.0 | 0.709 | 421 | | FAC | Eastern Area | 0.054 | 0.037 | 0.0 | 0.146 | 164 | | FAC | North-East | 0.056 | 0.043 | 0.0 | 0.146 | 95 | | INVCAP | All India | 19988.9 | 24503.0 | 0.0 | 134302.9 | 432 | | INVCAP | Eastern Area | 8763.6 | 17196.0 | 0.0 | 134302.9 | 172 | | INVCAP | North-East | 6043.8 | 16358.4 | 0.0 | 134302.9 | 105 | Using annual data for 2005 to 2018, a panel data regression was employed to investigate empirically the factors influencing the behavior of three variables of interest - deposit accounts per 1,000 population, credit accounts per 1,000 population, and the CD ratio. Separate estimations were carried out for all India and the EA. The explanatory variables included; branch penetration, basic infrastructure, economic condition, level of industrial activity and credit absorption by major sectors in the economy. The hypotheses to be tested derive weights from the relevant literature – relating to availability of basic infrastructure to economic growth (Rosenstein- Rodan, 1943; Nurkse, 1955; Hirschman, 1958; Rostow, 1965); and connecting economic development to finance (Robinson, 1952). The Hausman test was found to favour fixed effects7 over the random effects model. The static fixed effects model, however, could suffer from endogeneity problem of joint determination of the cause and effect variables. It also biases the estimates when the dynamic nature of the economic variables needs to be controlled for. Generalised Method of Moments (GMM) estimators are better suited for such conditions (Arellano and Bond, 1991; Arellano and Bover, 1995). The system GMM approach has been applied in the article as opposed to the difference GMM method because the former has been reported to be a more efficient and stable estimator when the autoregressive process of the dependent variable is highly persistent (Blundell and Bond, 1998). The two equations - in levels and in differences - in a system GMM are presented as below:  where Yit represents the dependent variable of interest for the ith state at the tth period, Xit is the matrix of explanatory variables (average population per branch, per capita availability of power, per capita income, number of factories and invested capital per 1,000 population and agricultural credit absorption), αi is the state-specific fixed effect parameter for capturing idiosyncratic features of state i and εit is the stochastic disturbance term distributed normally with mean 0 and variance σ2. System GMM estimation (which is suitable for a ‘small T, large N’ panel) was undertaken separately for broken time periods 2005-10 and 2011-18, respectively. Breaking of time periods was guided by the Chow break-point8 test as also the introduction of the financial inclusion plan in April 2010, which provided a policy push for creation of a significant number of deposit and credit accounts. Results of the estimation are as follows. For the EA as also at the all India level, improvement in income level and industrial activity were found to prop up number of deposit accounts per 1,000 population (Table 3). APPB is found to be positively related to the number of deposit accounts for both the EA as well all India until 2010. Post 2010, however, at the all India level, it is found to be inversely related. At the all India level, the average number of deposit accounts per 1,000 population in 2017 was 8,492, while for the eastern area it was 2,418. Recent initiatives towards branch rationalisation by banks on the back of penetration of technology add weight to this finding. For the eastern area, on the contrary, the positive effect of APPB on the number of deposit accounts in the short-run seems to suggest the need for furthering financial inclusion through branch expansion in this region. | Table 3: Dynamic Panel Estimation for Deposit Accounts | | [Dependent Variable – Deposit Accounts (DPAC)] | | | (1) | (2) | (3) | (4) | | | EA

(2005-10) | All India

(2005-10) | EA

(2011-18) | All India

(2011-18) | | DPACt-1 | 1.069*** | 0.792*** | 1.353*** | 0.968*** | | | (0.025) | (0.047) | (0.068) | (0.016) | | LOGPCIt-1 | 56.88*** | 374.2*** | | | | | (15.66) | (32.85) | | | | ΔLOGPCI | | | 1795.3*** | 942.1*** | | | | | (204.6) | (39.33) | | APPBt-1 | 0.003* | 0.008* | 0.008** | -0.016*** | | | (0.001) | (0.003) | (0.0025) | (0.002) | | ΔFAC | 592.1*** | 274.7*** | 2581.1*** | 482.5*** | | | (99.23) | (54.37) | (649.8) | (69.55) | | constant | -627.9*** | -3849.2*** | -343.7*** | 292.9*** | | | (176.2) | (321.2) | (71.95) | (34.95) | | Observations | 60 | 155 | 43 | 114 | | AR(2) (p-value) | 0.07 | 0.53 | 0.66 | 0.89 | | Sargan (p-value) | 0.67 | 0.10 | 0.70 | 0.28 | Notes: 1. Standard errors in parentheses.

2. +p< 0.10, *p< 0.05, **p< 0.01, ***p< 0.001. | While during 2005-10, the level of per capita income was found to increase the number of deposit accounts directly, growth in income was found to expand it in recent times. Possibly, bank deposits have become more closely associated with economic activity from 2010-11 (Saxena and Sreejith, 2018). Growth in per capita income is found to translate into more deposit accounts per 1,000 population in the EA than at all India level given the lower per capita income level of the former. An increase in the number of factories and resultant higher income generating capacity leads to more deposit penetration in the (relatively underbanked) EA vis-a-vis all India. The above findings indicate that financial inclusion efforts would bear fruits for the EA if concerted efforts are made for augmenting per capita income as also industrial activity. A rise in per capita income in the EA is also found to positively influence the number of credit accounts. Reflecting lower credit absorption capacity of the region - given its agrarian orientation and low industrial base - the impact of rising income on credit accounts was found to be significantly lower compared with estimates for all India during 2005-10 (Table 4).9 However, during 2011-18, an increase in income is found to have propelled higher demand for credit accounts in the EA vis-a-vis all India. | Table 4: Dynamic Panel Estimation for Credit Accounts | | [Dependent Variable – Credit Accounts (CRAC)] | | | (1) | (2) | (3) | (4) | | | EA

(2005-10) | All India

(2005-10) | EA

(2011-18) | All India

(2011-18) | | CRACt-1 | 0.451*** | 0.343*** | 0.436*** | 0.708*** | | | (0.089) | (0.0162) | (0.108) | (0.0237) | | LOGPCIt-1 | 9.214+ | 71.97*** | 52.06** | 41.34*** | | | (4.894) | (4.649) | (17.89) | (4.099) | | INVCAPt-1 | 0.00012 | -0.00031*** | 0.00076*** | -0.00047*** | | | (0.0002) | (0.00005) | (0.0002) | (0.00004) | | ΔAGCR | 0.006*** | | 0.006*** | | | | (0.0005) | | (0.0008) | | | POWERt-1 | | 0.018*** | | 0.0112*** | | | | (0.003) | | (0.003) | | constant | -65.73 | -701.5*** | -514.3** | -404.7*** | | | (48.63) | (45.31) | (181.3) | (41.35) | | Observations | 54 | 158 | 55 | 150 | | AR(2) (p-value) | 0.06 | 0.15 | 0.82 | 0.35 | | Sargan (p-value) | 0.99 | 0.22 | 0.73 | 0.29 | Notes: 1. Standard errors in parentheses.

2. +p< 0.10, *p< 0.05, **p< 0.01, ***p< 0.001. | Growth in the number of credit accounts in the EA is found to prop up credit to deposit ratio significantly and by a larger magnitude vis-à-vis all India (Table 5). Higher sensitivity of CD ratio during 2005-10 in the EA may reflect high credit growth recorded during this period. The responsiveness of CD ratio to the number of credit accounts per 1,000 population during 2011-18 in EA, however, has been muted. As noted by CRISIL (2018), the mean number of credit accounts per 1,000 population increased sharply in India during 2011-18 because of proliferation of credit accounts in the eastern area, post Jan Dhan Yojana (JDY). This may reflect the effort to reach out than actual demand for credit. At the all India level, higher availability of power per capita and greater road density is found to have a significant positive impact on the amount of credit utilised per unit of deposit. In the EA, progress of power and roads did not move together during 2005-10 (Chart 9a). Nevertheless, when both power and roads improved during 2011-18 (Chart 9b), it had a favourable impact on the CD ratio in the EA. Lack of complementarity in development of related infrastructure facilities could hinder their individual effectiveness (Markard and Hoffman, 2016; OECD, 2007). | Table 5: Dynamic Panel Estimation for CD ratio | | [Dependent Variable – CD ratio (CDU)] | | | (1) | (2) | (3) | (4) | | | EA

(2005-10) | All India

(2005-10) | EA

(2011-18) | All India

(2011-18) | | CDUt-1 | 0.789*** | 0.262*** | -0.129*** | 0.421*** | | | (0.096) | (0.067) | (0.035) | (0.007) | | DPACt-1 | -0.064*** | -0.018* | -0.017*** | -0.004*** | | | (0.013) | (0.008) | (0.003) | (0.0004) | | POWERt-1 | 0.051* | 0.010* | 0.0429*** | 0.003*** | | | (0.021) | (0.005) | (0.009) | (0.0005) | | ΔCRAC | 1.847*** | 0.174*** | 0.136** | 0.033*** | | | (0.554) | (0.0488) | (0.0418) | (0.003) | | ROADt-1 | | 2.301** | 4.295** | 1.642*** | | | | (0.722) | (1.509) | (0.055) | | constant | 12.71+ | 38.89*** | 31.98*** | 30.24*** | | | (7.257) | (3.123) | (4.329) | (1.179) | | Observations | 63 | 158 | 77 | 191 | | AR(2) (p-value) | 0.47 | 0.65 | 0.27 | 0.28 | | Sargan (p-value) | 0.69 | 0.18 | 0.91 | 0.51 | Notes: 1. Standard errors in parentheses.

2. +p< 0.10, *p< 0.05, **p< 0.01, ***p< 0.001. |

V. Concluding Observations Given the limited outreach of the banking sector in the eastern area relative to other regions of the country, there remains a significant scope for the financial sector to play its due role in spurring growth and addressing socio-economic challenges. Rise in income level, a stronger industrial base and better infrastructural facilities (such as power availability and road network) are found to facilitate higher penetration of credit. Complementarity in the development of infrastructural facilities is also found to be crucial for promoting industrialisation and thereby increasing the demand for credit. While recent financial inclusion initiatives such as JDY have succeeded in making available No Frills Accounts/ ‘Basic Savings Bank Deposit Accounts’ to households across the country, mere increase in deposit accounts per 1,000 population is not sufficient to realise the potential contribution of financial inclusion to economic growth. As the estimation results suggest, linking such bank accounts with credit is equally important, which might help improve the CD ratio. There is also a need for tailor-made policy interventions in individual states/ UTs of the eastern area for financial outreach efforts to be successful, given the marked heterogeneity in landscape, socio-economic conditions, agro-climatic regions, endowment of human resources and infrastructural conditions. References Arellano, M. and O. Bover (1995), ‘Another Look at the Instrumental Variables Estimation of Error Components Models’, Journal of Econometrics, 68: 29-51. Arellano, M. and S. Bond (1991), ‘Some tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations’, Review of Economic Studies, 58: 277-297. Beck, Thorsten, Erik Feyen, Alain Ize, and Florencia Moizeszowicz (2008), ‘Benchmarking Financial Development’, World Bank Policy Research Working Paper, WPS4638. Blundell, R. and S. Bond (1998), ‘Initial Conditions and Moment Restrictions in Dynamic Panel Data Models’, Journal of Econometrics, 87:11-143. Burgess, Robin and Rohini Pande (2005), ‘Do Rural Banks Matter? Evidence from the Indian Social Banking Experiment’, American Economic Review, 95(3), 780-795. CRISIL (2018), ‘Financial inclusion surges, driven by Jan-Dhan Yojana’, Vol. 4, February. Available [Online] https://www.crisil.com/en/home/our-analysis/reports/2018/02/crisil-inclusix-financial-inclusion-surges-driven-by-Jan-Dhan-yojana.html (Accessed on June 21, 2019) Ghosh, Saibal (2012), ‘Determinants of banking outreach: An empirical assessment of Indian states’, Journal of Developing Areas, 46(2): 269-295. Available [Online] https://mpra.ub.uni-muenchen.de/38650 (Accessed on June 20, 2019) Government of India (2008), ‘Report of the Committee on Financial Inclusion in India’. Hirschman, A.O. (1958), ‘The Strategy of Economic Development’, New havens: Yale University Press. Kumar, Nitin (2013), ‘Financial inclusion and its determinants: evidence from India’, Journal of Financial Economic Policy, 5(1): 4-19. Available [Online] https://doi.org/10.1108/17576381311317754 (Accessed on April 05, 2019) Markard, Jochen and Hoffmann, Volker H. (2016), ‘Analysis of complementarities: Framework and examples from the energy transition’, Technological Forecasting and Social Change, Elsevier, Vol. 111(C), pp. 63-75. Nurkse, R. (1955), ‘Problems of Capital Formation in Underdevelopment Countries’, Basil Blackwell: Oxford. OECD (2007), ‘Infrastructure to 2030’, Volume 2, Mapping Policy for Electricity, Water and Transport, June. Rajan, R. G. and Zingales, L. (1998), ‘Financial dependence and growth’, American Economic Review, 88, 559–86. Reserve Bank of India (2015), ‘Report of the Committee on Medium-term Path on Financial Inclusion’, December. Robinson, J. (1952), ‘The Generalization of The General Theory, in The Rate of Interest and Other Essays’, MacMillan, London. Rosenstein-Rodan, P. (1943), ‘Problems of Industrialization of Eastern and South-eastern Europe’, Economic Journal, 53: 202–211. Rostow, W.W. (1965), ‘The Economics of Take-Off into Self – Sustained Growth’, New York: St. Martin’s Press. Saxena, T. K. and Thoppil Bhargavan Sreejith (2018), ‘Post-Demonetisation Patterns of Deposits with Scheduled Commercial Banks: 2016-17 and 2017-18’, RBI Bulletin, December. Zang, H. and Kim, Y. C. (2007), ‘Does Financial Development Precede Growth? Robinson and Lucas Might Be Right’, Applied Economics Letters, 14:15-19.

|