On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (April 6, 2023) decided to: - Keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.50 per cent.

The standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent. - The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 2. Global economic activity remains resilient amidst the persistence of inflation at elevated levels, turmoil in the banking system in some advanced economies (AEs), tight financial conditions and lingering geopolitical hostilities. Recent financial stability concerns have triggered risk aversion, flights to safety and heightened financial market volatility. Sovereign bond yields fell steeply in March on safe haven demand, reversing the sharp increase in February over aggressive monetary stances and communication. Equity markets have declined since the last MPC meeting and the US dollar has pared its gains. Weakening external demand, spillovers from the banking crisis in some AEs, volatile capital flows and debt distress in certain vulnerable economies weigh on growth prospects. Domestic Economy 3. The second advance estimates (SAE) released by the National Statistical Office (NSO) on February 28, 2023 placed India’s real gross domestic product (GDP) growth at 7.0 per cent in 2022-23. Private consumption and public investment were the major drivers of growth. 4. Economic activity remained resilient in Q4. Rabi foodgrains production is expected to increase by 6.2 per cent in 2022-23. The index of industrial production (IIP) expanded by 5.2 per cent in January while the output of eight core industries rose even faster by 8.9 per cent in January and 6.0 per cent in February, indicative of the strength of industrial activity. In the services sector, domestic air passenger traffic, port freight traffic, e-way bills and toll collections posted healthy growth in Q4, while railway freight traffic registered a modest growth. Purchasing managers’ indices (PMIs) pointed towards sustained expansion in both manufacturing and services in March. 5. Amongst urban demand indicators, passenger vehicle sales recorded strong growth in February while consumer durables contracted in January. Among rural demand indicators, tractor and two-wheeler sales were robust in February. As regards investment activity, growth in steel consumption and cement output accelerated in February. Merchandise exports and non-oil non-gold imports contracted in February while the strong growth in services exports continued. 6. CPI headline inflation rose from 5.7 per cent in December 2022 to 6.4 per cent in February 2023 on the back of higher inflation in cereals, milk and fruits and slower deflation in vegetables prices. Fuel inflation remained elevated, though some softening was witnessed in February due to a fall in kerosene (PDS) prices and favourable base effects. Core inflation (i.e., CPI excluding food and fuel) remained elevated and was above 6 per cent in January-February. The moderation observed in inflation in clothing and footwear, and transportation and communication was largely offset by a pick-up in inflation in personal care and effects and housing. 7. The average daily absorption under the LAF moderated to ₹1.4 lakh crore during February-March from an average of ₹1.6 lakh crore in December-January. During 2022-23, money supply (M3) expanded by 9.0 per cent and non-food bank credit rose by 15.4 per cent. India’s foreign exchange reserves were placed at US$ 578.4 billion as on March 31, 2023. Outlook 8. The inflation trajectory for 2023-24 would be shaped by both domestic and global factors. The expectation of a record rabi foodgrains production bodes well for the food prices outlook. The impact of recent unseasonal rains and hailstorms, however, needs to be watched. Milk prices could remain firm due to high input costs and seasonal factors. Crude oil prices outlook is subject to high uncertainty. Global financial market volatility has surged, with potential upsides for imported inflation risks. Easing cost conditions are leading to some moderation in the pace of output price increases in manufacturing and services, as indicated by the Reserve Bank’s enterprise surveys. The lagged pass-through of input costs could, however, keep core inflation elevated. Taking into account these factors and assuming an annual average crude oil price (Indian basket) of US$ 85 per barrel and a normal monsoon, CPI inflation is projected at 5.2 per cent for 2023-24, with Q1 at 5.1 per cent, Q2 at 5.4 per cent, Q3 at 5.4 per cent and Q4 at 5.2 per cent, and risks evenly balanced (Chart 1). 9. A good rabi crop should strengthen rural demand, while the sustained buoyancy in contact-intensive services should support urban demand. The government’s thrust on capital expenditure, above trend capacity utilisation in manufacturing, double digit credit growth and the moderation in commodity prices are expected to bolster manufacturing and investment activity. According to the RBI’s surveys, businesses and consumers are optimistic about the future outlook. The external demand drag could accentuate, given slowing global trade and output. Protracted geopolitical tensions, tight global financial conditions and global financial market volatility pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2023-24 is projected at 6.5 per cent with Q1:2023-24 at 7.8 per cent; Q2 at 6.2 per cent; Q3 at 6.1 per cent; and Q4 at 5.9 per cent, with risks evenly balanced (Chart 2).  10. With CPI headline inflation ruling persistently above the tolerance band, the MPC decided to remain resolutely focused on aligning inflation with the target. It is essential to rein in the generalisation of price pressures and anchor inflation expectations. An environment of low and stable prices is necessary for the resilience in domestic economic activity to be sustained. While the policy rate has been increased by a cumulative 250 basis points since May 2022, which is still working through the system, there can be no room for letting down the guard on price stability. Taking these factors into account, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting, with readiness to act, should the situation so warrant. The MPC will continue to keep a strong vigil on the evolving inflation and growth outlook and will not hesitate to take further action as may be required in its future meetings. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth. 11. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 6.50 per cent. 12. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth. Prof. Jayanth R. Varma expressed reservations on this part of the resolution. 13. The minutes of the MPC’s meeting will be published on April 20, 2023. 14. The next meeting of the MPC is scheduled during June 6-8, 2023. (Yogesh Dayal)

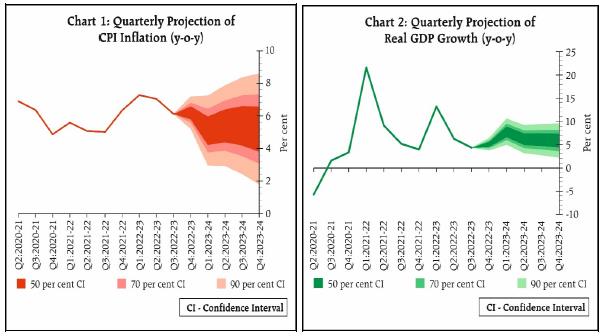

Chief General Manager Press Release: 2023-2024/22 |