[Under Section 45ZL of the Reserve Bank of India Act, 1934] The twentieth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held during December 3 to 5, 2019 at the Reserve Bank of India, Mumbai. 2. The meeting was attended by all the members – Dr. Chetan Ghate, Professor, Indian Statistical Institute; Dr. Pami Dua, Director, Delhi School of Economics; Dr. Ravindra H. Dholakia, former Professor, Indian Institute of Management, Ahmedabad; Dr. Michael Debabrata Patra, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Shri Bibhu Prasad Kanungo, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely: -

the resolution adopted at the meeting of the Monetary Policy Committee; -

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and -

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting. 4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (December 5, 2019) decided to: Consequently, the reverse repo rate under the LAF remains unchanged at 4.90 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 5.40 per cent. These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 6. Since the MPC’s meeting in October 2019, global economic activity has remained subdued, though some signs of resilience are becoming visible. Among the advanced economies (AEs), GDP growth in the US picked up in Q3 on strong private investment and personal consumption expenditure. More recent data, however, indicate that factory activity contracted for the fourth consecutive month in November, while retail sales and industrial production declined in October. In the Euro area, GDP growth remained stable in Q3 relative to the previous quarter on improved household consumption and government spending, although manufacturing activity continued to struggle with lingering geo-political uncertainties. With weak global demand pulling down exports, the Japanese economy lost momentum in Q3. Economic activity in the UK accelerated in Q3, primarily driven by the services sector and construction activity. 7. Among emerging market economies (EMEs), GDP growth in China decelerated further in Q3, reflecting weak industrial production and declining exports amidst trade tensions with the US. While retail sales edged lower in October, fiscal and monetary stimuli are expected to temper the slowdown. In Russia, GDP growth accelerated in Q3 on the back of an upturn in agricultural output and industrial activity. In South Africa, economic activity contracted in Q3, pulled down by slowing mining and manufacturing activity. In Brazil, GDP growth accelerated further in Q3, driven by agriculture, industry and business investment activity. 8. Crude oil prices have moved in a narrow range in both directions since the last meeting of the MPC, reflecting changing sentiments relating to progress in US-China trade talks. Gold prices traded sideways before falling in early November as a revival of risk appetite eased safe haven demand. Inflation remained benign in major AEs and EMEs in Q3, except in China where it firmed up to its highest level in eight years. 9. Global financial markets were buoyed in October by risk-on sentiment stemming from renewed optimism on a trade truce between the US and China and possibility of a Brexit deal. In the US, equity markets rallied in this environment, also supported by better than expected corporate earnings and strong jobs data. Stock markets in EMEs too registered gains in October before some selling pressure took hold in the second half of November on renewed fears of US-China trade talks stalling on the Hong Kong stand-off. Bond yields in the US firmed up from early October on risk-on sell-offs; however, they softened from mid-November on waning hopes of a near-term resolution of trade disputes. Bond yields in the Euro area remained negative, but expectations that a no-deal Brexit is less likely improved sentiment. In EMEs, bond yields showed mixed movements, driven initially by optimism on US-China trade talks and country-specific factors. In currency markets, the US dollar weakened against other major currencies, while EME currencies have been trading with an appreciating bias. Domestic Economy 10. On the domestic front, gross domestic product (GDP) growth moderated to 4.5 per cent year-on-year (y-o-y) in Q2:2019-20, extending a sequential deceleration to the sixth consecutive quarter. Real GDP growth was weighed down by a sharp slowdown in gross fixed capital formation (GFCF), cushioned by a jump in government final consumption expenditure (GFCE). Excluding GFCE, GDP growth would have been at 3.1 per cent. Growth in real private final consumption expenditure (PFCE) recovered from an 18-quarter trough. The drag from net exports eased on account of a sharper contraction in imports than in exports. 11. On the supply side, gross value added (GVA) growth decelerated to 4.3 per cent in Q2:2019-20, pulled down by a contraction in manufacturing. The slowdown in manufacturing activity was also reflected in a decline in capacity utilisation (CU) to 68.9 per cent in Q2:2019-20 from 73.6 per cent in Q1 in the early results of the Reserve Bank’s order books, inventories and capacity utilisation survey (OBICUS). Seasonally adjusted CU also fell to 69.8 per cent from 74.6 per cent during the same period. Growth in the services sector moderated, weighed down mainly by trade, hotels, transport, communication, broadcasting services and construction activity. However, growth in public administration, defence and other services accelerated in line with the surge in government final consumption expenditure. Agricultural GVA growth increased marginally, despite contraction in kharif foodgrains production in the first advance estimates. 12. Looking beyond Q2, rabi sowing is catching up from the setback caused by delay in kharif harvesting and unseasonal rainfall in October and early November. By November 29, it was only 0.5 per cent lower than the acreage covered a year ago. North-east monsoon precipitation was 34 per cent above the long-period average up to December 4. Storage in major reservoirs, the main source of irrigation during the rabi season, was at 86 per cent of the full reservoir level as on November 28 as compared with 61 per cent in the same period a year ago. 13. Contraction in output of eight core industries – which constitute 40 per cent of the index of industrial production (IIP) – extended into the second consecutive month in October and became more pronounced, dragged down by coal, electricity, cement, natural gas and crude oil. However, output of fertilisers rose sharply, reflecting expectations of robust sowing activity in the rabi season. According to the early results of the Reserve Bank’s industrial outlook survey, overall sentiment in the manufacturing sector remained in pessimism in Q3:2019-20 due to continuing downbeat sentiments on production, domestic and external demand, and the employment scenario. The purchasing managers’ index (PMI) for manufacturing increased from 50.6 in October to 51.2 in November 2019, driven up by an increase in new orders and output. 14. High frequency indicators suggest that service sector activity generally remained weak in October. Tractors and motorcycles sales – indicators of rural demand – continued to contract but at a moderated pace; however, passenger vehicle sales – an indicator of urban demand – posted a slender positive growth in October after 11 months of decline, reflecting festival season demand and promotional measures by auto companies. Commercial vehicle sales and railway freight traffic contracted. The PMI for services remained in negative zone in October (49.2) due to a decline in new export business and turning down of business expectations. However, it moved into expansion zone to 52.7 in November on a pick-up in new business. 15. Retail inflation, measured by y-o-y changes in the CPI, increased sharply to 4.6 per cent in October, propelled by a surge in food prices. Fuel group prices remained in deflation, while inflation in CPI excluding food and fuel moderated further from its level a month ago. 16. Turning to the drivers of CPI, food inflation spiked to 6.9 per cent in October – a 39-month high – pushed up by a sharp increase in prices of vegetables due to heavy unseasonal rains. Prices of onions, in particular, shot up by 45.3 per cent in September and further by 19.6 per cent in October. Inflation in several other food items such as fruits, milk, pulses and cereals also increased, reflecting diverse factors – the cost push of fodder prices in the case of milk; decline in production and sowing area of pulses; and minimum support price effects. Sugar and confectionery prices moved out of deflation in October as sugarcane output shrank on a y-o-y basis. 17. Fuel group prices remained weak for the fourth consecutive month in October due to deflation in prices of LPG, firewood and chips. Electricity prices, however, picked up in October following a rise in user charges by power distribution companies (DISCOMs) across 13 states as reflected in the CPI. 18. Inflation in CPI excluding food and fuel softened further from 4.2 per cent in September to 3.4 per cent in October, primarily due to favourable base effects. Price increases also moderated across several services as reflected in transportation fares, telephone charges, tuition fees and house rentals. 19. Households’ inflation expectations, measured by the Reserve Bank’s November 2019 round of the survey, increased by 120 basis points over the 3-month ahead horizon and 180 basis points over the 1-year ahead horizon as they adapted to the spike in food prices in recent months. Based on the Reserve Bank’s consumer confidence survey, spending on non-essential items of consumption has shrunk compared to a year ago; however, consumers expect their overall spending to remain unchanged going forward largely due to an increase in prices. Manufacturing firms polled in the industrial outlook survey of the Reserve Bank expect (i) weak demand conditions and reduced input price pressures in Q3:2019-20 and Q4; and (ii) muted output prices reflecting further weakening of pricing power. 20. Overall liquidity in the system remained in surplus in October and November 2019 despite an expansion of currency in circulation due to festival demand. Average daily net absorption under the LAF amounted to ₹ 1,98,566 crore in October. The Centre availed of ways and means advances (WMA) in the first week and the last three days of the month to fund its expenditure. In November, the average daily net absorption of surplus liquidity soared to ₹ 2,40,566 crore with more frequent and larger recourse to WMA by the Government. Consequently, the Reserve Bank decided to conduct longer-term variable rate reverse repo auctions with effect from November 4, 2019 in addition to overnight variable rate reverse repo auctions. So far, four longer term reverse repo auctions have been conducted – two auctions of 21 days tenor and one each of 35 days and 42 days tenor – absorbing ₹ 78,934 crore. Reflecting easy liquidity conditions, the weighted average call rate (WACR) traded below the policy repo rate (on an average) by 8 basis points (bps) in October and by 10 bps in November. 21. Monetary transmission has been full and reasonably swift across various money market segments and the private corporate bond market. As against the cumulative reduction in the policy repo rate by 135 bps during February-October 2019, transmission to various money and corporate debt market segments ranged from 137 bps (overnight call money market) to 218 bps (3-month CPs of non-banking finance companies). Transmission to the government securities market, however, has been partial at 113 bps (5-year government securities) and 89 bps (10-year government securities). Credit market transmission remains delayed but is picking up. The 1-year median marginal cost of funds-based lending rate (MCLR) has declined by 49 basis points. The weighted average lending rate (WALR) on fresh rupee loans sanctioned by banks declined by 44 basis points, while the WALR on outstanding rupee loans increased by 2 basis points during this period. However, transmission is expected to improve going forward as (i) the share of base rate loans, interest rates on which have remained sticky, declines; and (ii) MCLR-based floating rate loans, which typically have annual resets, become due for renewal. 22. After the introduction of the external benchmark system, most banks have linked their lending rates to the policy repo rate of the Reserve Bank. The median term deposit rate has declined by 47 bps during February-November 2019. The weighted average term deposit rate declined by 9 bps in October as against a decline of just 7 bps in eight months during February-September. This augurs well for transmission to lending rates, going forward. 23. Exports contracted in September-October 2019, reflecting the persisting weakness in global trade. Excluding petroleum products, however, the decline in exports was less pronounced and, in fact, non-oil export growth returned to positive territory in October after a hiatus of two months. Imports contracted faster than exports, with lower international crude oil prices resulting in a decline in the oil import bill. A sharp contraction in the volume of gold imports kept outgoes on this account in check. Non-oil non-gold imports also contracted, pulled down by electronics, coal and pearls and precious stones. Reflecting these developments, the trade deficit narrowed in September-October. On the financing side, net foreign direct investment rose to US$ 20.9 billion in H1:2019-20 from US$ 17.0 billion a year ago. Net foreign portfolio investment was of the order of US$ 8.8 billion in April-November 2019 as against net outflows of US$ 14.9 billion in the same period of last year. In addition, net investment by FPIs under the voluntary retention route have amounted to US$ 6.3 billion since March 11, 2019. Net disbursals of external commercial borrowings rose to US$ 11.5 billion during April-October 2019 as against US$ 1.2 billion during the same period a year ago. India’s foreign exchange reserves were at US$ 451.7 billion on December 3, 2019 – an increase of US$ 38.8 billion over end-March 2019. Outlook 24. In the fourth bi-monthly resolution of October 2019, CPI inflation was projected at 3.4 per cent for Q2:2019-20, 3.5-3.7 per cent for H2:2019-20 and 3.6 per cent for Q1:2020-21 with risks evenly balanced. The actual inflation outcome for Q2 evolved broadly in line with projections – averaging 3.5 per cent. The inflation print for October, however, was much higher than expected. 25. Going forward, the inflation outlook is likely to be influenced by several factors. First, the upsurge in prices of vegetables is likely to continue in immediate months; however, a pick-up in arrivals from the late kharif season along with measures taken by the Government to augment supply through imports should help soften vegetables prices by early February 2020. Second, incipient price pressures seen in other food items such as milk, pulses, and sugar are likely to be sustained, with implications for the trajectory of food inflation. Third, both the 3-month and 1-year ahead inflation expectations of households polled by the Reserve Bank have risen and these latent sentiment upsides are being reflected in other surveys as well. Fourth, domestic financial markets have exhibited volatility. Fifth, domestic demand has slowed down, which is being reflected in the softening of inflation excluding food and fuel. Sixth, crude oil prices are expected to remain range bound, barring any supply disruptions due to geo-political tensions. Taking into consideration these factors, the CPI inflation projection is revised upwards to 5.1-4.7 per cent for H2:2019-20 and 4.0-3.8 per cent for H1:2020-21, with risks broadly balanced (Chart 1). 26. Turning to the growth outlook, real GDP growth for 2019-20 in the October policy was projected at 6.1 per cent – 5.3 per cent in Q2:2019-20 and in the range of 6.6-7.2 per cent for H2:2019-20 – with risks evenly balanced; and 7.2 per cent for Q1:2020-21. GDP growth for Q2:2019-20 turned out to be significantly lower than projected. Various high frequency indicators suggest that domestic and external demand conditions have remained weak. Based on the early results, the business expectations index of the Reserve Bank’s industrial outlook survey indicates a marginal pickup in business sentiments in Q4. On the positive side, however, monetary policy easing since February 2019 and the measures initiated by the Government over the last few months are expected to revive sentiment and spur domestic demand. Taking into consideration these factors, real GDP growth for 2019-20 is revised downwards from 6.1 per cent in the October policy to 5.0 per cent – 4.9-5.5 per cent in H2 and 5.9-6.3 per cent for H1:2020-21 (Chart 2). While improved monetary transmission and a quick resolution of global trade tensions are possible upsides to growth projections, a delay in revival of domestic demand, a further slowdown in global economic activity and geo-political tensions are downside risks.   27. The MPC notes that economic activity has weakened further and the output gap remains negative. However, several measures already initiated by the Government and the monetary easing undertaken by the Reserve Bank since February 2019 are gradually expected to further feed into the real economy. Data on corporate finance and on projects sanctioned by banks and financial institutions suggest some early signs of recovery in investment activity, though its sustainability needs to be watched closely. The need at this juncture is to address impediments, which are holding back investments. The introduction of external benchmarks is expected to strengthen monetary transmission. In this context, there is also a need for greater flexibility in the adjustment in interest rates on small saving schemes. In the judgement of the MPC, inflation is rising in the near-term, but it is likely to moderate below target by Q2:2020-21. It is, therefore, prudent to carefully monitor incoming data to gain clarity on the inflation outlook. Similarly, the forthcoming union budget will provide better insight into further measures to be undertaken by the Government and their impact on growth. 28. The MPC recognises that there is monetary policy space for future action. However, given the evolving growth-inflation dynamics, the MPC felt it appropriate to take a pause at this juncture. Accordingly, the MPC decided to keep the policy repo rate unchanged and continue with the accommodative stance as long as it is necessary to revive growth, while ensuring that inflation remains within the target. 29. All members of the MPC – Dr. Chetan Ghate, Dr. Pami Dua, Dr. Ravindra H. Dholakia, Dr. Michael Debabrata Patra, Shri Bibhu Prasad Kanungo and Shri Shaktikanta Das – voted in favour of the decision. 30. The minutes of the MPC’s meeting will be published by December 19, 2019. 31. The next meeting of the MPC is scheduled during February 4-6, 2020. | Voting on the Resolution to keep the policy repo rate unchanged at 5.15 per cent | | Member | Vote | | Dr. Chetan Ghate | Yes | | Dr. Pami Dua | Yes | | Dr. Ravindra H. Dholakia | Yes | | Dr. Michael Debabrata Patra | Yes | | Shri Bibhu Prasad Kanungo | Yes | | Shri Shaktikanta Das | Yes | Statement by Dr. Chetan Ghate 32. Inflationary expectations are important in driving actual inflation. Since the last review, there has been a sharp spike in both the 3-month ahead (by 120 bps) inflationary expectations from 8% to 9.2% and 1-year ahead (by 180 bps) inflationary expectations from 8.1% to 9.9%. 33. Such a sharp increase has not been seen in the past three years. Even the 3- month ahead trimmed mean (from 8.7% to 9.7%) and one year ahead trimmed mean (8.6% to 9.9%) have increased. While these trends may be adaptively reflecting the rise in food inflation, they also may possibly reflect the rise in economic policy uncertainty in the current growth climate. 34. October food inflation printed at 6.9% which is a 39-month high. The cumulative momentum in food between April-October FY:19-20 is higher than that in the previous three financial years. Unseasonal rainfall has led to both a damage to Kharif output and to a delay in the sowing of the Rabi crop. This is building into price pressures. While some of the impulses could be idiosyncratic, it may also be that food surprises sustain going forward. For instance, the cumulative momentum of food excluding vegetables by October was higher this financial year. I have been concerned about the trajectory of food inflation in the last several reviews. 35. Headline inflation at 4.6% printed at a 16-month high. In contrast, inflation excluding food and fuel, moderated by 80 bps from 4.2% in September to 3.4% in October. Inflation excluding food and fuel still indicates relatively soft cumulative momentum so far in FY:2019-20, reflecting lacklustre demand in the economy. The price build up in services has also remained soft in groups such as housing, health, and education, which has helped contribute to low momentum in inflation excluding food and fuel. Low service sector inflation however is unlikely to sustain. This is because the service sector in India tends to be heavily supply constrained. 36. Economic growth continues to be lacklustre. Growth in Q2: FY19-20 fell further to 4.5%, the lowest in 26 quarters with investment growing at 1%. The Index of Industrial Production (IIP) continued to be in contraction in September (-4.3%) compared to -1.4% in August. The weakness in the IIP was manifest across all segments. The truncated IIP also contracted by -5.5% in September. Based on RBI’s Industrial Outlook Survey (IOS), demand conditions remained pessimistic in Q3: FY 19-20. 37. Despite lacklustre growth, and rising inflation, I think monetary policy is in a good place right now. 38. There are mitigating factors that would suggest that it is best to obtain greater clarity on the evolving growth-inflation risk picture. 39. First, counter-cyclical monetary policy has not been as effective as expected due to inadequate monetary policy transmission. Weak monetary transmission is one of the factors that has resulted in the poor macroeconomic equilibrium the economy is currently in and it could lead to excesses in the financial sector. 40. Transmission will no doubt improve with external benchmarking as the proportion of loans linked to the MCLR falls and more loans become linked to the external benchmark. Further, reducing risk aversion in the NBFC sector, problems in which have led to elevated term premia, is more in the domain of “macro-prudential policy”, rather than monetary policy. 41. Second, a few positive factors have emerged since the last review. This suggests that a wait and watch approach is appropriate. 42. First, the WALR on fresh rupee loans has fallen by 44 bps (from 29 bps in the last review). A large quantum of rate cuts has still not been transmitted, and the MPC loses nothing by waiting for a couple of months. Second, net FDI into India, at 20.9 Billion USD between April-September 2019 continues to be strong. Third, within exports, the share of sectors recording negative growth has reduced to 38.2% in October 2019. Fourth, in October, some high frequency indicators have begun to contribute to a positive momentum in growth, suggesting that it is best to wait for a few months to see whether the slowdown has bottomed out or not. Fifth, it is best to wait to see how the corporate tax cuts have impacted the economy. Since the tax cut was announced on September 20, and RBI’s analysis of corporate performance corresponded to the end of September, this data did not pick up the effects of the tax cut. Further, the corporate tax cut for new companies will only apply after October 1. Sixth, the large decline in capacity utilization (CU) to 68.9% in Q2: FY 19-20 based on early results of Order Books, Inventory and Capacity Utilisation Survey, needs further clarification. Importantly, using sentiments on CU in the IOS, Q3: FY 19-20 is forecasted to improve somewhat. Seventh, consumption expenditure (PFCE) growth has strengthened to a little over 5% in Q2: FY 19-20 from 3.1% in Q1: FY19-20 which is noteworthy notwithstanding the deflator effect. Eighth, the PMI in both manufacturing and services has strengthened in their most recent readings. Ninth, the risk environment in the global economy appears to have abated a bit suggesting that global recession risks seem to have waned. 43. I worry however that real wage growth in the organized sector has further weakened since the last review. In the rural sector, weak demand conditions add to the prospect of a “one-legged” recovery driven by the urban sector. 44. I vote to pause. I also vote to retain the stance as accommodative. I will remain data dependant, going forward; further monetary policy action will depend on the evolving growth-inflation dynamics. Statement by Dr. Pami Dua 45. Headline inflation, measured by CPI inflation, increased from 3.3% in August and 4% in September 2019 to 4.6% in October. Food inflation increased from 4.7% in September to 6.9% in October, mainly due to an increase in inflation in vegetables, fruits, pulses, milk and cereals. Inflation excluding food and fuel moderated to 3.4% in October from 4.2% in September, reflecting favourable base effects, as well as softening domestic demand. 46. Looking forward, inflation expectations of households, as captured through RBI’s Inflation Expectations Survey of Households, increased in the November 2019 round, compared to the September round, by 120 basis points for the three-month-ahead horizon and by 180 basis points for the one-year-ahead horizon, possibly due to the sharp increase in food prices. At the same time, the Industrial Outlook Survey (IOS) shows an expectation of subdued selling prices of manufacturing in Q4:2019-20, as well as reduced input cost pressures. 47. The increase in prices of vegetables is expected to continue in the near future, but moderate by February 2020 due to higher arrivals in the late kharif and subsequently from the rabi season, as well as measures taken by the government to augment the supply through imports. 48. On the output side, GDP growth fell for the sixth consecutive quarter to 4.5% (y-o-y) in Q2:2019-20 from 5% in the previous quarter. Growth in private final consumption expenditures was 5.1%, up from 3.1% in the previous quarter, and growth in government final consumption expenditure increased to 15.6%, while growth in gross capital formation slowed sharply. Excluding government final consumption expenditure, GDP growth is 3.1%, underlining the weakness in private domestic demand. Growth in GVA also fell to 4.3% in Q2:2019-20, pulled down by manufacturing sliding into contractionary territory, as well as moderation in services. 49. Turning to survey data, early results of RBI’s Order Books, Inventory and Capacity Utilisation Survey (OBICUS) suggest a drop in capacity utilisation in the manufacturing sector. The Business Assessment Index (a composite of demand indicators), based on the early results of the RBI’s Industrial Outlook Survey for the manufacturing sector, remained in the contractionary zone for Q3:2019-20. According to RBI’s Consumer Confidence Survey, the Current Situation Index and the Future Expectations Index both dropped in the November 2019 round, implying lower current activity and a less optimistic outlook. Meanwhile, the Manufacturing Purchasing Managers’ Index increased from 50.6 in October to 51.2 in November, reflecting an increase in new orders and output. 50. Thus, overall, private consumption and investment activity are weak, and business and consumer sentiment are somewhat downbeat. Further, exports growth has contracted by less than imports growth, indicating that the slowdown in domestic demand may be somewhat more acute than the weakness in global growth. 51. On the international front, some signs of a cyclical upturn in global industrial growth are now in sight. Industrial growth prospects have improved for both France and Germany, although the US industrial outlook remains subdued. The outlook for the Chinese economy remains constrained, while Japan is flirting with recessionary conditions. Overall, the global economy is expected to experience uneven improvement in economic growth in the next few months, according to Economic Cycle Research Institute’s (ECRI’s) international leading indexes. However, the world’s largest economies are in no position to act as locomotives to pull global growth out of the doldrums, and will therefore not be able to provide much impetus to the Indian economy. Thus, the drivers of growth for the Indian economy would have to be from within the economy. Meanwhile, growth in ECRI’s Indian Coincident Index looks to have bottomed, having improved modestly of late. 52. On the domestic front, from the monetary policy perspective, monetary transmission of the cumulative reduction in the policy repo rate by 135 basis points from February to October 2019 to the various money and corporate debt markets has been in the range of 137 basis points in the overnight call money market to 218 basis points in 3-month CPs of non-banking finance companies. Transmission to the government securities market has been partial at 113 basis points for 5-year government securities and 89 basis points for 10-year government securities. The weighted average lending rate (WALR) on fresh rupee loans sanctioned by banks fell by 44 basis points during this period. Going forward, the recent linking of the lending rate to external benchmarking is expected to expedite the pending transmission, with most banks having linked their lending rates to the policy repo rate. 53. Further, to reiterate what I said in the last policy, the policy heavy-lifting to reverse the growth slowdown has to be a multi-pronged approach. In this regard, a number of measures have already been undertaken by the government with a focus on reviving growth. These include steps to relax norms for FDI, focus on seamless tax administration, improve ease of doing business, consolidate public sector banks, and encourage the flow of credit from the banking sector to the financial and real economy sectors. The government has also undertaken fiscal stimulus in the form of a major overhaul in corporate income tax aimed at reducing the overall tax burden on corporates and, in turn, improving India's global competitiveness. Such measures should help to improve the investment climate and attract more capital flows into India. 54. At the same time, lacklustre revenue collections, alongside lower nominal GDP growth rate add to the risk of fiscal slippage. Thus, at this juncture, it would be prudent to take a cue from the upcoming Budget on the government’s initiatives to revive growth. 55. Thus, with the pending monetary transmission expected to be realised in the near future, measures already undertaken by the government to address the growth slowdown expected to play out, and growth initiatives expected to be announced in the upcoming Budget, there is merit in a wait-and-watch approach to see how these measures pan out and impact real economic activity, including investment, going forward. 56. At the same time, while growth is slowing, headline inflation is projected to rise in the near-term, but moderate to below target by Q2:2020-21. At this juncture, it is, therefore, best to monitor incoming data on both inflation and growth. 57. I, therefore, vote to keep the policy rate unchanged and continue with the accommodative stance. Statement by Dr. Ravindra H. Dholakia 58. After the October 2019 meeting of MPC, the inflation readings of September and October 2019 turned out to be substantially higher, resulting in RBI’s forecast to be higher by 160 bps for the Q3 of 2019-20 with significant upward revisions in the forecast over the next year. Similarly, the estimate of the GDP growth for Q2 of 2019-20 has not only turned out to be 80 bps below but was also contrary to RBI’s assessment that the growth slowdown would bottom out in Q1 of 2019-20. As I had pointed out in my statement in October MPC minutes, the RBI’s forecast of 6.1% growth during the current year was on an optimistic side and would not materialize. Now the RBI has revised its expectation substantially downward to 5%, which seems plausible. The sharp spike in food inflation may continue for the next two-three months driving the headline inflation above the mid-point target and closer to the upper bound of the flexible target range. The forecast of inflation by RBI for the 4 quarters up to Q2 of 2020-21 is based on certain assumptions where considerable uncertainties are involved. I, therefore, take the RBI forecast of the headline inflation of 3.8% for Q2 of 2020-21 with some reservation at this point. Inflationary expectations that were reasonably anchored till recently can shoot up during this period as evident from the RBI Survey of Households and IIMA Survey of Businesses although the situation may not go out of control. Moreover, there are some green shoots of growth recovery during the third and fourth quarters of the current year perhaps in response to the counter-cyclical measures on the fiscal and monetary policy fronts, but they need to be confirmed with more data. I had argued for a 40 bps rate cut in the last policy and I still maintain that there is space for further rate cuts even now. The question is of the timing and magnitude. In my view, it is prudent to wait and watch out for clarity on growth – inflation dynamics and gain some more confidence at this juncture before taking a decisive action on the policy rate front. In the meantime, there is enough slack for the markets to adjust to the rate cuts already made. I, therefore, vote to hold the policy repo rate at 5.15% for now and continue with the accommodative stance. More specific reasons for my vote are as follows – -

While the current spike in the headline inflation is arguably due to the temporary supply shocks on the food front, the impact is not confined only to a few items. It is important to understand how much would be the impact and for how long. The household inflationary expectations as per the latest RBI survey showed a sharp increase by 120 bps and 180 bps for three months and twelve months ahead horizon. Thus, the surveyed households believe that the increased inflation is not a temporary phenomenon but can go on increasing over the whole of the year to come. On the other hand, IIM Ahmedabad Survey of Businesses shows an increase of only 10 bps in their inflationary expectation 12 months ahead indicating that the current spike is temporary. RBI’s own forecasts support the latter, but they are based on some crucial assumptions, which are surrounded by several uncertainties. Clarity on this with more data is important. -

My own research with a co-author published in the Economic and Political Weekly on 3rd March 2018 shows that as per recent inflation dynamics the second round effects of an external shock (like food or fuel prices) on the core inflation are, if at all, quite weak. Unlike in the past, it is the headline inflation that now reverts to the core rather than the core reverting to the headline. RBI’s recent survey on consumer confidence provides some support to this argument. It has shown that in response to the sharp rise in the food prices, the consumption of the non-essential items has declined implying very low substitutability between food and non-food consumption. It may, therefore, be argued that inflationary expectations based largely on food inflation may not result in a rise in the core inflation. We may, however, need some more observations to confirm or contradict this argument. -

Although the capacity utilization as per the early results of RBI survey has fallen substantially to less than 70% in Q2 of 2019-20, there are several green shoots of growth recovery in the economy. PMI in manufacturing as well as services has shown substantial increase with the latter turning into an expansionary mode from the earlier contraction. RBI survey has shown that corporates have turned investors from savers earlier. After a long time, corporates are increasing their physical assets and not financial assets. Transmission of rate cuts in the credit markets is picking up and with the policy of external benchmark for lending rates, it is likely to further pick up. RBI’s own forecast suggests that the growth slowdown has bottomed out in Q2 of 2019-20 and gradual recovery would take place in Q3 and Q4 and continue in the next year. High frequency data and advance estimates of GDP for the current year need to be watched carefully to examine the extent and speed of this recovery since it can have implications for the headline inflation. -

Union Budget for 2020-21 and the Economic Survey for 2019-20 are due in the next couple of months. As I have argued earlier, the growth recovery has to be addressed fundamentally and durably by the fiscal policy with the monetary policy, if at all, playing only a facilitating role. The stance, content and commitment of the fiscal measures outlined in the Budget and the Economic Survey should, therefore, provide extremely useful guidance on the growth concerns. In my opinion, monetary policy should supplement those efforts provided inflation risks are contained within the given target range. In this context, I would like to repeat my earlier arguments on the concerns about fiscal slippage. When there is a cyclical downturn due to serious growth slowdown, it is logical to expect a fiscal slippage even without any change in the fiscal policy parameters. If the estimates of nominal income growth are seriously undershot, revenues are bound to fall short of the target. If under such circumstances, expenditures are cut to maintain the fiscal deficit target, it would amount to a contractionary fiscal policy during a downturn!! Generally, the stabilization policies like fiscal and monetary policies should be counter-cyclical and not pro-cyclical. The fiscal discipline target of 3% of GDP under such circumstances should not be overemphasized and can be temporarily ignored. Even though the N.K. Singh Committee has provided for a slippage by 50 bps under such exigencies, there is hardly any rationale for only 50 bps slippage. In my opinion, therefore, the slippage of more than 50 basis points may also be justified under the present circumstances. It is important in my opinion to wait for the clarity of the government’s commitment and action to tackle the growth slowdown before further action on the monetary front at present. 59. Given all these arguments, it is pragmatic to wait for more clarity to emerge for a firm action on policy rate. In the meantime, the expected better transmission of the past rate cuts will serve the purpose in any case. The stance should continue to be accommodative but in this policy, we should hold the repo rate at 5.15%. Statement by Dr. Michael Debabrata Patra 60. The configuration of macroeconomic and financial conditions facing the MPC in this meeting exerts conflicting pulls. Arguably, the slump in real GDP growth warrants accommodative monetary policy actions and stance whereas the upturn in headline inflation for the third month in succession after a quiescent phase of nine months calls for an opposite response or at least status quo until there is ground to infer that the food price spirals that are driving it are on the ebb. 61. In this context, two features of the recent upsurge in inflation weigh upon the monetary policy decision. First, it is prudent to expect higher than current readings over the next two or three months. This warrants a pause in the sequence of rate reductions that began in February 2019. Second, inflation pressures are rotating from vegetable prices to those of other elements of food and beverages. By current reckoning, vegetables prices can be expected to reverse by Q4:2019-20 as the supply situation improves. They can, therefore, be looked through while setting monetary policy. The key question is: will the upside in other food prices reverse or persist, especially those of pulses and milk? If it persists, will it spill over into non-food inflation? This too warrants close monitoring of incoming data over the next few months and, therefore, a pause. 62. Turning to the real economy, the weakness in overall activity may likely prolong into Q3, if not turn weaker. In particular, the sharp downturn in the growth of investment calls for urgent policy responses, reinforcing the actions already taken. The contribution of monetary policy in this endeavour can be to reduce the cost of capital. To bring about the turnaround, however, the net present value of future income streams from investment must exceed the cost of capital. This will hinge around a rekindling of animal spirits in a business-conducive environment, highlighting the importance of close and continuous policy coordination. Monetary policy has been pre-emptive in supporting growth and is committed to remaining in accommodative mode until growth revives. With 135 basis points of interest rate reductions and fiscal policy actions working their way into the economy, it is apposite in this meeting to allow this pass-through and be in readiness to back signs of traction with resolute and calibrated policy actions. 63. While voting for status quo in this meeting, it is important to note that headroom is available to act and arrest any further weakening of growth impulses. With this objective in the fore, I also vote for maintaining the accommodative monetary policy stance. Statement by Shri Bibhu Prasad Kanungo 64. Since the October policy, growth and inflation outcomes have deviated significantly from their paths projected by the RBI in the October policy. Real GDP growth at 4.5 per cent (y-o-y) in Q2:2019-20 turned out to be much weaker than 5.3 per cent projected earlier, despite a robust growth of 15.6 per cent in Government Final Consumption Expenditure (GFCE). While private consumption improved, fixed investment grew at a measly rate of 1 per cent. On the GVA side, industrial and services growth slowed down, while agriculture growth picked up slightly. 65. Beyond Q2, the index of eight core industries further contracted by 5.8 per cent during October 2019 to register the lowest growth in 2011-12 series after contracting by 5.1 per cent in September 2019. Among other high frequency indicators, cement production, international air cargo traffic and railway freight traffic contracted further in October. On the positive side, passenger vehicles sales and domestic air passenger traffic – indicators of urban demand - saw positive growth in October, while motor cycles sales – an indicator of rural demand – witnessed lower contraction vis-à-vis September. The PMI for manufacturing and services improved in November. Rabi sowing is catching up. Adequate reservoir levels augur well for the rabi prospects. Growth projection for 2019-20 has been revised downwards to 5 per cent from 6.1 per cent in the last policy. 66. On the inflation front, unseasonal rains in October and early November damaged certain crops and also disrupted the mandi arrival patterns. As a result, the temporary demand-supply imbalance led to price pressures in several vegetables, especially onion prices. During H1: 2020-21, food prices are projected to soften in response to rabi supplies. Inflation pressures in CPI excluding food and fuel have softened further on account of continuing moderation in demand conditions. Median inflation expectations of households, which are somewhat backward looking and also highly sensitive to food inflation, firmed up significantly from 8 per cent to 9.2 per cent for three months ahead horizon, and from 8.1 per cent to 9.9 per cent for one year ahead horizon. 67. The headline inflation path for H2: 2019-20 is projected to rise to 5.1 to 4.7 per cent now as against 3.5 to 3.7 per cent earlier. However, inflation will moderate gradually below the target in Q2:2020-21. 68. The cumulative repo rate reduction of 135 bps effected since February 2019 has resulted in 44 bps reduction in weighted average lending rate (WALR) on fresh rupee loans till October, which is lower than expected. It is, however, encouraging that there has been some improvement in transmission following the introduction of external benchmarking of new floating rate loans to the retail (housing, vehicle, education loans, etc.) and micro and small enterprises (MSE) sectors. After the introduction of external benchmarking system in October 2019, most of the banks have linked their lending rates to the policy repo rate. The weighted average term deposit rate (WATDR) declined by 9 bps in October, which bodes well for monetary transmission, going forward. 69. The MPC has cumulatively reduced the repo rate by 135 basis points, the impact of which will gradually be felt on the real economy. The current uptick in inflation driven by a sharp increase in food prices is expected to reverse. However, there exists considerable uncertainty on the food price trajectory, and the quantum of impact of unseasonal rains on kharif output would be known only early next year. The incoming data may also provide greater clarity on the growth outlook. I vote for a pause in the policy rate at this juncture. It is better to wait and watch for the incoming data. Even as space exists for future monetary policy action, a pause at this juncture would help calibrate the appropriate policy response in future. I also vote for persevering with the accommodative stance as long as it is necessary to revive growth while ensuring that inflation remains within the target. Statement by Shri Shaktikanta Das 70. Economic activity has continued to weaken with GDP growth decelerating for the sixth consecutive quarter for Q2:2019-20. Of the two main components of GDP, while investment activity weakened further, private consumption showed signs of recovery. CPI inflation has surged in last three consecutive months reflecting a spike in vegetable prices and price pressures in some other food items. However, inflation excluding food and fuel glided below four per cent, suggesting subdued domestic demand conditions. Global economic activity has remained weak, weighed down by continuing uncertainty relating to trade conflicts. Major central banks have maintained accommodative monetary policy stances. 71. Headline inflation rose sharply in September and further in October, driven up by a sudden spike in prices of vegetables as kharif crop was damaged due to unseasonal rains in many parts of the country; increase in prices of onion was particularly sharp. Prices of certain non-vegetable foods items such as pulses, cereals, fruits and sugar increased at a faster pace than in previous two years. On the whole, food group inflation was at a 39-month high in October. Fuel group inflation remained in deflation for the fourth consecutive month in October mainly due to continuing deflation in LPG prices. Electricity prices, however, picked up in many states. 72. CPI inflation excluding food and fuel moderated to an all-time low of 3.4 per cent in October. Apart from the strong favourable base effect, price increases also moderated in several services such as transport fares, telephone charges, tuition fees, recreation and amusement and house rentals. Inflation expectations of households polled in the last round of the survey conducted by the Reserve Bank, however, increased sharply for both the 3-month ahead and 12-month ahead horizons, possibly reflecting the sharp rise in food prices. CPI inflation is projected to rise to 5.1-4.7 per cent for H2:2019-20 before moderating to 4.0-3.8 per cent for H1:2020-21. 73. Turning to economic activity, GDP growth decelerated to 4.5 per cent for Q2:2019-20 from 5.0 per cent in Q1; the Reserve Bank had projected GDP growth for Q2 at 5.3 per cent in its October policy. Though growth in private consumption recovered to 5.1 per cent in Q2 from 3.1 per cent in Q1, it needs to be seen whether it will be sustained. Government final consumption expenditure surged to provide a strong support to economic activity, in the absence of which growth would have been still lower. On the supply side, manufacturing activity contracted. Early results of the order books, inventory and capacity utilisation (OBICUS) survey conducted by the Reserve Bank suggest that capacity utilisation in the manufacturing sector declined to 68.9 per cent in Q2:2019-20 from 73.6 per cent in Q1. Services sector activity also moderated, despite a pick up in growth in public administration, defence and other services (PADO). 74. Beyond Q2, however, some positive signs have emerged. Rabi sowing has caught up considerably from the setback caused by delay in kharif harvesting and unseasonal rainfall in October and early November. Storage in major reservoirs at 86 per cent of the full reservoir level as on November 28 was much higher as compared with 61 per cent a year ago. This augurs well for the rabi season. While the output of eight core industries contracted in October, PMI manufacturing increased to 51.2 in November from 50.6 in October. Certain high frequency indicators of the services sector showed positive growth in October/November vis-à-vis September. Passenger vehicle sales, domestic and international air passenger traffic, foreign tourist arrivals, and finished steel consumption showed higher growth in October in comparison with the previous month. Though commercial vehicle and two-wheeler sales contracted in October, the pace of contraction slowed down. The PMI for services, which was in contraction in October (49.2), moved into expansion zone to 52.7 in November. Real GDP growth for 2019-20 has been revised downwards from 6.1 per cent in the October policy to 5.0 per cent – 4.9-5.5 per cent in H2:2019-20; GDP growth has been projected at 5.9-6.3 per cent for H1:2020-21. While improved monetary transmission and a quick resolution of global trade tensions could push the growth above the projected trajectory, a delay in revival of domestic demand, a further slowdown in global economic activity and geo-political tensions could pull it down below the projected path. 75. Monetary transmission has been full and almost instantaneous across various money market segments and private corporate bond yields, while the transmission to the government securities market has been partial. Despite some improvement in the recent period, monetary transmission to lending rates of banks remains inadequate. The 1-year median marginal cost of funds-based lending rate (MCLR) declined by 49 basis points during February-November 2019. The weighted average lending rate (WALR) on fresh rupee loans sanctioned by banks declined by 44 basis points during February-October 2019, while the WALR on outstanding rupee loans increased by 2 basis points during the same period. With the introduction of the external benchmark system, transmission is expected to improve going forward as the existing MCLR-based floating rate loans, which typically have annual resets, become due for renewal. Overall liquidity in the system remains in sizable surplus. The weighted average term deposit rate declined by 9 bps in October and 16 basis points during February-October 2019. This bodes well for transmission to lending rates. 76. Overall, several uncertainties cloud the growth-inflation outlook. First, the surge in food inflation in last three months, driven up by a spike in onion and other vegetable prices, could be transitory. It is likely to reverse gradually as late kharif output comes to the market. In view of this, even as current food price spike driven by vegetables can be looked through, there is a need for greater clarity as to how the overall food inflation path is going to evolve, as there is some uncertainty about the outlook of prices of certain non-vegetable food items such as cereals, pulses, milk and sugar. It is also not clear at this stage as to how the recent increase in telecom charges will play out even as CPI inflation excluding food and fuel has moderated. 77. Second, though domestic demand conditions have weakened, certain high frequency indicators have improved in the more recent period. There are also some indications that the capex cycle may be turning up as reflected in (i) an increase in the share of funds deployed in fixed assets to 45.6 per cent during H1:2019-20 from 18.9 per cent during H1:2018-19, based on the results of 1539 listed private manufacturing companies; and (ii) an increase in total cost of projects sanctioned in the private sector by banks/financial institutions to ₹ 79,525 crore in Q2:2019-20 from ₹ 45,781 crore in Q1. These are positive developments but need to be carefully assessed with incoming data for their sustainability. 78. Third, monetary transmission has improved in recent months. The impact of past policy rate reductions on monetary transmission, however, is still unfolding. 79. Fourth, the impact of recent counter-cyclical measures taken by the Government is playing out. The next budget is due for presentation in about two months and it will provide greater clarity about the further measures that the Government may initiate. It is imperative that monetary and fiscal policies work in close coordination. 80. Fifth, global financial markets have remained volatile caused by trade related uncertainties. 81. Considering all these aspects in their totality, on balance, I vote for keeping the policy repo rate on hold at the present level of 5.15 per cent in this meeting and for maintaining the accommodative stance as long as necessary to revive growth, while ensuring that inflation remains within the target. There is policy space, the use of which, however, needs to be appropriately timed for ensuring its optimal impact. (Yogesh Dayal)

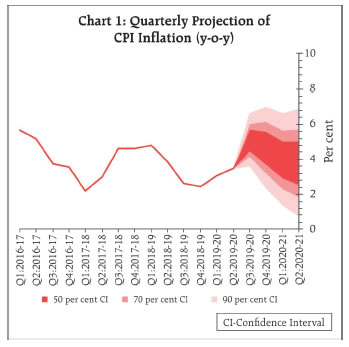

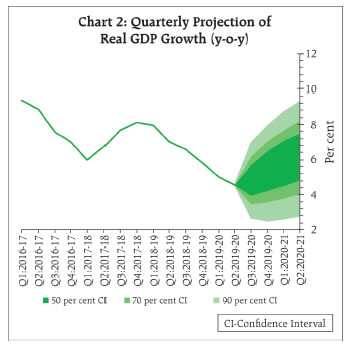

Chief General Manager Press Release: 2019-2020/1465 |