[Under Section 45ZL of the Reserve Bank of India Act, 1934] The fifteenth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held from February 5 to 7, 2019 at the Reserve Bank of India, Mumbai. 2. The meeting was attended by all the members – Dr. Chetan Ghate, Professor, Indian Statistical Institute; Dr. Pami Dua, Director, Delhi School of Economics; Dr. Ravindra H. Dholakia, former Professor, Indian Institute of Management, Ahmedabad; Dr. Michael Debabrata Patra, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Viral V. Acharya, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely: -

the resolution adopted at the meeting of the Monetary Policy Committee; -

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and -

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting. 4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. On the basis of an assessment of the current and evolving macroeconomic situation at its meeting today, the Monetary Policy Committee (MPC) decided to: - reduce the policy repo rate under the liquidity adjustment facility (LAF) by 25 basis points from 6.5 per cent to 6.25 per cent with immediate effect.

Consequently, the reverse repo rate under the LAF stands adjusted to 6.0 per cent, and the marginal standing facility (MSF) rate and the Bank Rate to 6.5 per cent. The MPC also decided to change the monetary policy stance from calibrated tightening to neutral. These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment 6. Since the last MPC meeting in December 2018, there has been a slowdown in global economic activity. Among key advanced economies (AEs), economic activity in the US lost some steam in Q4:2018. The outlook for Q1:2019 is clouded by the partial government shutdown, though the labour market conditions remain strong. In the Euro area, economic activity lost momentum on weak industrial activity. The Japanese economy is gradually recovering and an accommodative monetary policy stance is expected to buttress domestic spending. 7. Economic activity also slowed in some major emerging market economies (EMEs). In China, growth decelerated in Q4:2018. Economic activity in Russia lost pace, with soft oil prices posing a downside risk to growth. The Brazilian economy appeared to have ended 2018 on a firmer note, driven by improved domestic spending and exports, though industrial activity continued to struggle to recover from the disruptions of H1:2018. In South Africa, the economic recovery in Q4:2018 remained gradual, tempered by weak industrial activity and subdued exports. 8. Crude oil prices recovered from their December lows in early January on production cuts, but remain below their peak levels in October. Base metals, which witnessed selling pressures in December on persisting uncertainty over US-China trade frictions, recouped losses in January on expectations of thawing of trade disputes and production disruptions. Gold prices have risen, underpinned by safe haven demand in response to geo-political uncertainty and volatility in equity markets. Inflation edged lower in major AEs and many key EMEs. 9. Global financial markets began the year on a calmer note after a turbulent December. Among AEs, equity markets in the US recovered from a sharp sell-off in December, triggered by monetary policy tightening by the Fed, trade tensions and an impending shutdown. EM stock markets, which declined in December on a slew of soft economic data, registered some gains recently on expectations of accommodative monetary policy stances in major economies. The 10-year yield in the US, which fell to a multi-month low in December, rose in January on the edging up of crude oil prices and positive risk sentiment, though softening of the Fed stance restricted the gains. Among other AEs, bond yields in the Euro area and Japan eased on diminishing optimism about global growth. In most EMEs, bond yields have eased as well. In currency markets, the US dollar remained under pressure, though expectations of easing trade tensions provided some support. EME currencies appreciated on the pause in the rate hiking cycle by the Fed and expectations of a positive outcome from US-China trade negotiations. 10. Moving on to the domestic economy, on January 7, 2019 the Central Statistics Office (CSO) released the first advance estimates (FAE) for 2018-19, placing India’s real gross domestic product (GDP) growth at 7.2 per cent – the same level as in 2017-18 (first revised estimates). The FAE for 2018-19 featured an acceleration in gross fixed capital formation (GFCF) and a slowdown in consumption expenditure (both private and government). The drag from net exports is estimated to decline in 2018-19. 11. Some indicators of investment demand, viz., production and imports of capital goods, contracted in November/December. Credit flows to industry remain muted. Available data suggest that while revenue expenditure of the Centre, excluding interest payments and subsidies, contracted in Q3, that of States increased sharply, thus maintaining overall growth in government spending. 12. On the supply side, the FAE have placed the growth of real gross value added (GVA) at 7.0 per cent in 2018-19 as compared with 6.9 per cent in 2017-18. The estimates incorporated a slowdown in agricultural GVA growth and an acceleration in industrial GVA growth. Services GVA growth is set to soften due to subdued activity in trade, hotels, transport, communication and other services. Growth in public administration and defence services is also likely to moderate. 13. Rabi sowing so far (up to February 1, 2019) has been lower than in the previous year, but the overall shortfall of 4.0 per cent across various crops is expected to catch up as the season comes to a close. The lower rabi sowing reflects a deficient north-east monsoon (44 per cent below the long period average); however, storage in major reservoirs – the main source of irrigation during the rabi season – at 44 per cent of the full reservoir level (as on January 31, 2019) was marginally higher than in the previous year. The extended period of cold weather in this year’s winter is likely to boost wheat yields, which would partly offset the shortfall, if any, in area sown. 14. After exhibiting an uptick in the festive month of October, industrial activity, measured by the index of industrial production (IIP), slowed down in November. The year-on-year (y-o-y) growth in core industries decelerated to 2.6 per cent (y-o-y) in December, pulled down by a slowdown in the production of electricity and coal; and contraction in petroleum refinery products, crude oil and fertilisers output. Capacity utilisation (CU) in the manufacturing sector, as measured by the Reserve Bank’s order books, inventory and capacity utilisation survey (OBICUS), increased to 74.8 per cent in Q2 from 73.8 per cent in Q1; seasonally adjusted CU also improved to 75.3 per cent from 74.9 per cent. While the Reserve Bank’s business assessment index of the industrial outlook survey (IOS) for Q3:2018-19 suggests a weakening of demand conditions in the manufacturing sector, the business expectations index (BEI) points to an improvement in Q4. The manufacturing purchasing managers’ index (PMI) for January remained in expansion on the back of increased output and new orders. 15. High-frequency indicators of the services sector suggest some moderation in the pace of activity. Sales of motorcycles and tractors imply weakening of rural demand in December. Sales of passenger cars – an indicator of urban demand – contracted, possibly reflecting volatility in fuel prices and mandated long-term insurance premium payments. Commercial vehicle sales also shrank in December 2018 from a high base of the previous year. Lead indicators for the hotels sub-segment, viz., foreign tourist arrivals and air passenger traffic, point to softening in November-December. In the communication sub-segment, the telephone subscriber base contracted in October-November, while that of broadband continued to expand in October. The services PMI continued to expand in January 2019 despite a dip from the previous month. Indicators of the construction sector, viz., consumption of steel and production of cement, continued to show healthy growth, though growth in cement production inched lower in November 2018, reflecting a base effect. 16. Retail inflation, measured by y-o-y change in the CPI, declined from 3.4 per cent in October 2018 to 2.2 per cent in December, the lowest print in the last eighteen months. Continuing deflation in food items, a sharp fall in fuel inflation and some edging down of inflation excluding food and fuel contributed to the decline in headline inflation. 17. Five constituents of the food group – vegetables, sugar, pulses, eggs and fruits, accounting for about 30 per cent of food group – were in deflation in December. Inflation in respect of other major food sub-groups – cereals, milk, and oils and fats – was subdued. Within cereals, rice prices declined for the fourth consecutive month in December. Inflation in prices of meat and fish and non-alcoholic beverages showed an uptick, while it remained sticky for prepared meals. 18. Inflation in the fuel and light group fell from 8.5 per cent in October to 4.5 per cent in December, pulled down by a sharp decline in the prices of liquefied petroleum gas (LPG), reflecting softening of international petroleum product prices. Kerosene inflation continued to edge up due to the calibrated increase in its administered price. 19. CPI inflation excluding food and fuel decelerated to 5.6 per cent in December from 6.2 per cent in October, dragged down mainly by the moderation in the prices of petrol and diesel in line with the decline in international petroleum product prices. Housing inflation continued to edge down as the impact of the house rent allowance (HRA) increase for central government employees dissipated. However, inflation in several of the sub-groups – household goods and services; health; recreation and amusement; and education – firmed up in December, offsetting much of the impact of lower inflation in petrol, diesel and housing. 20. Inflation expectations of households, measured by the December 2018 round of the Reserve Bank’s survey, softened by 80 basis points for the three-month ahead horizon and by 130 basis points for the twelve-month ahead horizon over the last round, reflecting the continued decline in food and fuel prices. Producers’ assessment of inflation in input prices eased in Q3 as reported by manufacturing firms polled by the Reserve Bank’s industrial outlook survey. 21. Inflation in the prices of farm inputs and industrial raw materials remained elevated, despite some softening. Growth in rural wages moderated in October. 22. The weighted average call rate (WACR) traded below the policy repo rate on 12 out of 20 days in December, all 23 days in January and 4 days in February (up to February 6). The WACR was below the repo rate on an average by 4 basis points in December and 11 basis points each in January and February. Currency in circulation expanded sharply during December and January. The liquidity needs arising out of expansion in currency were met by the Reserve Bank through injection of durable liquidity amounting to ₹500 billion each in December and January through purchases under open market operations (OMOs). Accordingly, total durable liquidity injected through OMOs has aggregated ₹2.36 trillion during 2018-19 so far. Liquidity injected under the LAF was ₹996 billion in December on an average daily net basis, and ₹329 billion in January. In February, however, the average daily liquidity position turned into surplus with an average absorption of ₹279 billion. 23. Export growth on a y-o-y basis was almost flat in November and December 2018, primarily due to a high base effect and weak global demand. While growth in exports of petroleum products remained positive, non-oil exports declined, dragged down by lower shipments of gems and jewellery, engineering goods, meat and poultry. Import growth slowed in November and turned negative in December 2018. While imports of petroleum (crude and products) rose in line with the increase in import volumes, non-oil imports such as pearls and precious stones, gold, electronic goods and transport equipment, recorded declines. The merchandise trade deficit for April-December 2018 was a shade higher than its level a year ago. Net services exports picked up in October and November 2018, which combined with low oil prices, could have a salutary impact on the current account deficit in Q3. On the financing side, net FDI flows to India during April-November 2018 were higher than a year ago. Foreign portfolio flows turned negative in January 2019, after rebounding in November and December 2018. India’s foreign exchange reserves were at US$ 400.2 billion on February 1, 2019. Outlook 24. In the fifth bi-monthly monetary policy resolution in December 2018, CPI inflation for 2018-19 was projected in the range of 2.7-3.2 per cent in H2:2018-19 and 3.8-4.2 per cent in H1:2019-20, with risks tilted to the upside. The actual inflation outcome at 2.6 per cent in Q3:2018-19 was marginally lower than the projection. There have been downward revisions in inflation projections during the course of the year, reflecting mainly the unprecedented soft inflation recorded across food sub-groups. 25. Several factors will shape the inflation path, going forward. First, food inflation has continued to surprise on the downside with continuing deflation across several items and a significant moderation in inflation in cereals. Several food groups are experiencing excess supply conditions domestically as well as internationally. Hence, the short-term outlook for food inflation appears particularly benign, despite adverse base effects. Secondly, the moderation in the fuel group was larger than anticipated. Inflation in items of rural consumption such as firewood and chips, which had remained sticky and at elevated levels, has collapsed in recent months. Electricity prices also showed an unexpected moderation, providing a softer outlook for the fuel group. Thirdly, while inflation excluding food and fuel remains elevated, the recent unusual pick-up in the prices of health and education could be a one-off phenomenon. Fourthly, the crude oil price outlook remains broadly the same as in the December policy. Fifthly, the Reserve Bank’s surveys show that inflation expectations of households as well as input and output price expectations of producers have moderated significantly. Finally, the effect of the HRA increase for central government employees has dissipated completely along expected lines. Taking into consideration these developments and assuming a normal monsoon in 2019, the path of CPI inflation is revised downwards to 2.8 per cent in Q4:2018-19, 3.2-3.4 per cent in H1:2019-20 and 3.9 per cent in Q3:2019-20, with risks broadly balanced around the central trajectory. 26. Turning to the growth outlook, GDP growth for 2018-19 in the December policy was projected at 7.4 per cent (7.2-7.3 per cent in H2) and at 7.5 per cent for H1:2019-20, with risks somewhat to the downside. The CSO has estimated GDP growth at 7.2 per cent for 2018-19. Looking beyond the current year, the growth outlook is likely to be influenced by the following factors. First, aggregate bank credit and overall financial flows to the commercial sector continue to be strong, but are yet to be broad-based. Secondly, in spite of soft crude oil prices and the lagged impact of the recent depreciation of the Indian rupee on net exports, slowing global demand could pose headwinds. In particular, trade tensions and associated uncertainties appear to be moderating global growth. Taking into consideration the above factors, GDP growth for 2019-20 is projected at 7.4 per cent – in the range of 7.2-7.4 per cent in H1, and 7.5 per cent in Q3 – with risks evenly balanced.

27. Headline inflation is projected to remain soft in the near term reflecting the current low level of inflation and the benign food inflation outlook. Beyond the near term, some uncertainties warrant careful monitoring. First, vegetable prices have been volatile in the recent period; reversal in vegetable prices could impart upside risk to the food inflation trajectory. Secondly, the oil price outlook continues to be hazy. Thirdly, a further heightening of trade tensions and geo-political uncertainties could also weigh on global growth prospects, dampening global demand and softening global commodity prices, especially oil prices. Fourthly, the unusual spike in the prices of health and education needs to be closely watched. Fifthly, financial markets remain volatile. Sixthly, the monsoon outcome is assumed to be normal; any spatial or temporal variation in rainfall may alter the food inflation outlook. Finally, several proposals in the union budget for 2019-20 are likely to boost aggregate demand by raising disposable incomes, but the full effect of some of the measures is likely to materialise over a period of time. 28. The MPC notes that the output gap has opened up modestly as actual output has inched lower than potential. Investment activity is recovering but supported mainly by public spending on infrastructure. The need is to strengthen private investment activity and buttress private consumption. 29. Against this backdrop, the MPC decided to change the stance of monetary policy from calibrated tightening to neutral and to reduce the policy repo rate by 25 basis points. 30. The decision to change the monetary policy stance was unanimous. As regards the reduction in the policy repo rate, Dr. Ravindra H. Dholakia, Dr. Pami Dua, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted in favour of the decision. Dr. Chetan Ghate and Dr. Viral V. Acharya voted to keep the policy rate unchanged. The MPC reiterates its commitment to achieving the medium-term target for headline inflation of 4 per cent on a durable basis. The minutes of the MPC’s meeting will be published by February 21, 2019. 31. The next meeting of the MPC is scheduled from April 2 to 4, 2019. Voting on the Resolution to reduce the policy repo rate by 25 bps to 6.25 per cent | Member | Vote | | Dr. Chetan Ghate | No | | Dr. Pami Dua | Yes | | Dr. Ravindra H. Dholakia | Yes | | Dr. Michael Debabrata Patra | Yes | | Dr. Viral V. Acharya | No | | Shri Shaktikanta Das | Yes | Statement by Dr. Chetan Ghate 32. In the last several reviews, I have highlighted the need for keeping inflationary expectations anchored durably at the 4% target. While the 3 month and 1 year ahead inflationary expectation numbers still remain elevated, the decline in median inflationary expectations in the most recent round for three months (by 80 basis points) and for 1 year ahead (by 130 basis points) is encouraging. This is the first time since the history of the survey that the change in inflationary expectations has been as large as it has from a “low” level. 33. Going forward, lower oil and food prices – if sustained – will help inflationary expectations further taper allowing for the durability of the 4% target. 34. Oil prices have declined by more than 30 percent since its peak in early October mainly reflecting increases and prospective increases in global supply. Food inflation was in deflation (-1.5%, Y-o-Y) in December. Few commodities (pulses, sugar) continue to have persisting deflation, although pulses deflation has reduced from double digits to a single digit. The existing glut in international markets for various food commodities will limit the scope for food exports keeping a lid on food commodities inflation in the months ahead. Inadequate procurement has also helped limit the pass through from higher MSP prices to headline inflation. 35. RBI’s projections for Q3 FY 19-20 headline inflation stand at 3.9%. These projections are however sensitive to the assumed momentum on food inflation. If, for instance, vegetable prices rebound in April-August in a stronger way, these projections will be easily breached. The bouncing back of vegetable prices is not an unreasonable assumption when seen from the perspective of the high weighted contribution of vegetables to food inflation in the last 6 years or so. Also, area under Rabi crops sown so far is lower. Factors like these make it opportune to wait and watch to see how the food price sub-index evolves in the next couple of months. 36. The elevated level of inflation ex food and fuel continues to be challenging, despite the fall from 5.8% in November to 5.6% in December. Offsetting base and momentum effects have kept inflation ex food and fuel sticky. The m-o-m seasonally adjusted annualised rate (saar) for inflation ex food fuel in December 2018 was elevated at 5.4 per cent. 37. Inflation has thus softened but not in a broad-based way. 38. I see the growth picture as robust despite the emergence of soft spots. Economic growth in the last four years (since the advent of inflation targeting) based on CSO’s latest revisions averaged 7.7%, which is consistent with elevated core inflation and a virtually closed output gap. While non-food bank credit (NFBC) growth has declined marginally in the last few months, it continues to be high (14.6% on January 18, 2019). Credit growth to Non-Banking Financial Companies (NBFCs) was also high at 55.1% in December 2018 according to RBI data. This level has been above 40% since July 2018. Both the service and manufacturing PMIs continue to be in expansion mode for the last several months. Seasonally adjusted capacity utilization rose for the 2nd consecutive quarter in Q2: 18-19 to 75.3%. There was also a significant improvement in consumer sentiment. 39. On the downside, the IIP fell to a 17 month low at 0.5% Y-o-Y, although this reflects the somewhat higher volatility typical of the October-December window because of festive holidays. Consumer durable goods production also contracted by 0.9 per cent in November 2018. Growth in a number of economies has slowed this year due to trade tensions and the associated uncertainty. This clouds India’s export outlook and should be carefully watched. 40. I also worry that India is not consolidating fiscally although the extra budgetary spending on social welfare and stimulative programs may not materialize (unless states match it with their own initiatives). The quality of fiscal expenditures after the election may also improve. 41. Given the above reasons, maintaining status quo on the rates would be consistent with sustainable growth in the economy and achieving the inflation target over the medium-term. 42. I vote, however, to change the stance to neutral from ‘calibrated tightening’. Statement by Dr. Pami Dua 43. Headline inflation softened to 2.2 per cent in December from 2.3 per cent in November and 3.4 per cent in October, primarily due to a drop in food inflation from -0.1 per cent in October to -1.7 per cent in November and -1.5 per cent in December. Inflation excluding food and fuel fell from 6.2 per cent in October to 5.7 per cent and 5.6 per cent in November and December, respectively. The impact of house rent allowance of central government employees has now faded, while there is an unusual spike in inflation in health and education. At the same time, there was also a moderation in inflation in transport and communication. 44. RBI’s projected trajectory of headline inflation has also somewhat softened to 2.8 per cent in Q4 of 2018-19 (down from 3.2 per cent in the last policy round) and 3.4 per cent in Q2 of 2019-20 (down from 4.2 per cent). Furthermore, various surveys signal moderation in inflation expectations. Inflation expectations in the December 2018 round of the Reserve Bank’s Survey of Households softened by 80 basis points and 130 basis points for three-month ahead and one-year ahead horizons, respectively, vis-à-vis the last round. The Reserve Bank’s Industrial Outlook Survey indicates moderation in input prices in the fourth quarter of 2018-19, as reported by manufacturing firms. The Purchasing Managers’ Index for January 2019 suggests that input costs and selling prices remain modest. The Economic Cycle Research Institute’s (ECRI) Indian Future Inflation Gauge, a harbinger of inflation, has also declined, signalling a moderation in future inflation. One-year-ahead Business Inflation Expectations also declined in December, as per the Business Inflation Expectations Survey conducted by IIM-Ahmedabad for the month of December. 45. Looking forward, downside risks to the inflation outlook include continuing moderation in food inflation. The slowdown in global growth may also lead to softening of crude oil prices and moderation in inflation. Upside risks include supply disruptions in crude oil and geopolitical tensions. 46. On the output side, although RBI lowered its growth projection, GDP is expected to grow by 7.2 per cent in the first quarter of 2019-20, rising to 7.5 percent in Q3. Consumer Confidence has improved in the December 2018 round, with the future expectations index close to the all-time high of the December 2016 round. Forward looking indicators such as RBI’s Business Expectations Index for the manufacturing sector signal an improvement in the fourth quarter based on upbeat sentiments on production, order books, exports and capacity utilisation. These movements are corroborated by the January PMI. Meanwhile, growth in the Indian Leading Index, a predictor of the direction of Indian economic growth maintained by the Economic Cycle Research Institute (ECRI), New York, has risen lately, indicating some improvement in economic growth prospects. 47. A major downside risk to growth is the continued global growth slowdown, along with trade tensions and associated uncertainties. Indeed, growth in ECRI’s Indian Leading Exports Index has weakened, dimming the exports growth outlook. According to ECRI’s leading indexes, U.S. economic growth is expected to continue to decelerate, while the inflation cycle is expected to remain in a downswing in the coming months, despite the Fed's abrupt U-turn. Furthermore, based on ECRI’s Chinese leading indexes, overall Chinese growth is expected to continue to languish for the time being, while Chinese industrial growth will stay in a downturn, in the months ahead. Eurozone economic growth prospects remain dismal, with Italy in recession and Germany and France getting closer to recessionary conditions. Thus, as per ECRI’s prognosis, overall global economic growth will continue to stay in a cyclical downswing, while inflation will decline in every major economy. This may not only halt central bank plans for policy "normalization", but also afford leeway for policy easing. 48. In light of the benign inflation outlook and a moderation in inflation expectations, as well as the likely headwinds due to the global growth slowdown, I vote for decreasing the policy repo rate by 25 basis points and changing the stance from calibrated tightening to neutral. Statement by Dr. Ravindra H. Dholakia 49. In the MPC meeting of December 2018, I had argued that given the sudden favourable changes in the macroeconomic environment during November 2018 and their magnitude, it was the most opportune time for the MPC to cut the policy rate. However, because the MPC had insistently changed its stance from neutral to calibrated tightening with a 5:1 majority vote only in the previous meeting of October stating explicitly that any rate cuts were off the table, it would not be appropriate to cut the rate in the December 2018 policy. My strong plea to change the stance to neutral was also not accepted by my other colleagues in the MPC, though it was made clear in the subsequent communication that in future the MPC could consider a rate cut if the upside risk to inflation did not materialize. The subsequent two prints of monthly CPI headline inflation for November and December 2018, which are now available, confirm that the upside risks have considerably subdued with the predicted inflation over the next 3-4 quarters coming down further. On the other hand, there are concerns about the GDP growth slowing down, which is reflected in the marginal reduction in the RBI’s growth forecast. Therefore, it would be appropriate to consider a rate cut not only to correct the past inaction but also provide impetus to growth without materially risking inflation beyond the targeted 4 percent. Under these circumstances, I think space has opened up for a substantial rate cut of about 50 to 60 bps going forward. There is, therefore, an immediate need to change the stance formally from calibrated tightening to neutral and cut the policy rate by 25 bps to begin with. More specific reasons for my vote are as follows: -

The implicit volatility in the oil prices was unusually high during November 2018, but now, during December 2018 and particularly January 2019, has significantly come down to almost its long-term average. There is an expectation of oil prices stabilizing at current levels of about $ 60 - $ 65 per barrel. The risks of significant overshooting on a sustained basis have substantially receded. -

Food prices are likely to remain subdued over the next 3-4 quarters as per the detailed exercise of forecast undertaken by the RBI staff in consultation with the subject matter experts. -

Inflation ex-food and fuel is also predicted to fall from its current level of about 5.9 percent in Q3 of 2018-19 to about 5.1 percent in Q3 of 2019-20. It may fall even more if the current spike in health and education price index turns out to be only one off phenomenon. Thus, the core (or ex-food and fuel) inflation also shows a declining trend. This is quite consistent with the finding of my study with a co-author published in EPW (March 03, 2018) that persistence of core inflation is coming down in India perhaps because the inflation targeting regime in India has resulted in anchoring of people’s inflationary expectations and as a result the core inflation is also declining. -

As a result of all this, the headline inflation forecast one year ahead by RBI staff has turned out to be less than the target of 4 percent for the first time. With the policy rate of 6.5 percent, this implies the real policy rate of about 2.6 percent, which is one of the highest in the world as I have been arguing. We do not need such a high real policy rate. It only discourages private investment and impedes growth and employment. There is an urgent need to correct the situation by bringing down the real policy rate to a more reasonable and acceptable level particularly when the expected inflation 3-4 quarters ahead is within the target of 4 percent. -

It is important to note that the inflationary expectations in the economy have also been falling now at least for the last three survey rounds. Median household inflationary expectations 3 and 12 months ahead in the RBI surveys have shown considerable decline of about 120 and 130 bps and business expectations of headline CPI inflation 12 months ahead in the IIMA surveys have shown 53 bps decline. Moreover, the absolute number in the latter is 3.8 percent, which is almost the same as the RBI forecast. This provides more comfort for our quantitative assessment going forward. -

Recently announced budget of the Central Government shows no fiscal slippage from the path of fiscal and debt consolidation during 2018-19 when we consider the first revised estimates of GDP published on 31st January 2019. The slippage during 2019-20 without additional resource mobilization (since it was an interim budget) also turns out to be less than 20 bps from the fiscal consolidation path. In all probability, in the regular budget to be presented after the general election, such a minor gap may be covered with additional resource mobilization. It may not, therefore, have any significant inflationary impact on the economy and a very limited impact on the real interest rates in the system. With the institutional reforms in the recent past, significant fiscal slippage from the states side taking place is also not very likely. -

With the latest revisions in the GDP and unemployment estimates over the recent past there is a need to have a serious relook at the estimates of potential output and potential output growth in the economy. My views expressed earlier on the issue and estimates given by renowned scholars with rich policy making experience in the country need to be considered seriously. Accordingly, the potential output growth for the Indian economy going forward seems to be in the range of 8 to 8.5 percent and not 7 to 7.5 percent as was implicitly assumed now for quite some time. If we consider this more plausible estimate, the output gap is widening rather than closing. Generally, as the economic policy reforms are implemented, the potential output growth rises because it opens up new opportunities for productivity growth and efficiency. The current marginal downward revision in the growth forecast for the next 3-4 quarters, therefore, suggests that a substantial output gap is likely to open up exercising downward pressure on wage growth and inflation. -

The experience of this MPC corroborates a negative correlation between the real policy rate (as measured by the excess of the actual policy rate over the projected inflation one year ahead at the time of the policy announcement) and the real GDP growth. One cannot reject the hypothesis that the recent slowdown in the real GDP growth in India is on account of high real policy rates among other factors. If so, now is the ripe time to correct the real interest rates and create policy space for future actions if required. 50. Given all these reasons, in my view this is the time to act decisively by changing the stance from calibrated tightening to neutral and cutting the policy rate by 25 bps to begin with. The future rate actions may be data driven particularly with respect to the target of 4 percent headline inflation sustaining over time and the direction and magnitude of output gap. Statement by Dr. Michael Debabrata Patra 51. My sense from recent readings is that inflation is troughing and its path over the 12-months ahead horizon is likely to be one that rises from current lows. 52. Given that inflation excluding food and fuel is elevated but sticky (fuel inflation is easing and its weight in the CPI is small relatively speaking), the future trajectory of headline inflation will be determined essentially by the momentum of food price changes, especially in the first half of 2019-20 when typically, there is a pre-monsoon firming up. 53. The critical judgment call is: will the momentum of food prices revert to the typical pattern from the unusually subdued pace observed in 2018-19 (April-August), or, will it take some time for large excess supplies in several food items to balance out before the usual momentum takes hold? My sense is the latter, given that the prices of some items like pulses and sugar are sluggishly emerging out of a deep cyclical downswing, while those of oils and fats are muted by the turning down of international commodity prices, and other prices such as those of fruits, vegetables and milk are experiencing irregular and unusual softness. The outlook for cereal prices has also turned benign, with prospects of drawing down of sizable excess buffer stocks in the months ahead. 54. Meanwhile, outside the food group, upside risks to the headline inflation path from crude prices have also ebbed considerably and the recent upsurges in prices of education and health could possibly be short-lived. 55. In an inflation targeting framework, the forecast becomes the intermediate target because it congeals all available information on the final goal variables – inflation and growth – which are invisible. The forecast indicates that headline inflation is likely to course below 4 per cent up to the third quarter of 2019-20, thus securing the target over a one-year ahead time horizon. Significantly, the path of inflation has been adjusted downwards by 40-80 basis points since the last meeting of the MPC in December 2018. This is consistent with the stylised evidence – surveyed households, businesses and professional forecasters have made sizable corrections in their inflation expectations over the next twelve months; consumers are more sanguine about the evolving price situation than before; and cost pressures are moderate with delayed and incomplete pass-through to selling prices. The key insight is provided by the direction of these adjustments, not their levels. 56. As the amended RBI Act enjoins us, if the primary target for headline inflation is achieved on a reasonably lasting basis, it opens up some headroom to address the objective of growth. The MPC will need to closely monitor the evolution of these disparately driven price movements and calibrate the monetary policy stance accordingly. If the momentum of food price changes in the next few months indicates that inflation is likely to rise above 4 per cent and persist in the upper reaches of the tolerance band, pre-emptive action will be warranted to ensure that the primary objective of maintaining price stability is defended and achieved lastingly. 57. Turning to the outlook for growth, domestic activity remains resilient, but it appears to be shedding some speed in the second half of 2018-19. Dark clouds seem to be gathering over the horizon. High frequency indicators suggest that the pick-up in investment in the first half of 2018-19 may have lost some strength in the second half and considerable uncertainty shrouds the prospects of an improvement in private investment – especially into new capacity addition – and capacity utilisation in manufacturing is straining above trend in view of the still weak capex cycle. 58. The biggest downside risk to growth is likely to stem from global developments – the weakening of global growth in the second half of 2018 may prolong into coming quarters; global trade and investment may be impacted by ongoing trade tensions; and tail risks from policy uncertainties in systemically important economies may crystallise. Should a deeper than currently anticipated global slowdown take hold, domestic activity could be dragged down by retarding impulses transmitted through the channels of exports and investment. In this scenario, it is prudent to preserve sufficient policy space to insulate the economy from adverse external shocks and boost the domestic economy in an opportune manner rather than deplete it in haste. 59. Accordingly, I vote for a 25 basis points reduction in the policy rate and a pre-emptive shift to a neutral policy stance. Statement by Dr. Viral V. Acharya 60. Since the December monetary policy meeting, food inflation prints have continued to be soft, mainly due to vegetables and fruits witnessing healthy domestic production combined with imports (in some cases). In fact, several food groups are now in deflation, continuing with the momentum of recent food inflation prints that were available at the time of the December policy. Fuel inflation has eased due to a drop in international Liquefied Petroleum Gas (LPG) prices. Headline inflation excluding food and fuel has moderated somewhat due to a fall in crude oil prices and complete waning of central government employees’ House Rent Allowance (HRA) effects; nevertheless, it remains at a highly elevated level, ranging between 5.6-6.2% over the past three prints, with inflation in health and education components showing a spike in December due to unexpected rise in prices of medicines and private tuition costs. 61. The RBI headline inflation projections were already revised substantially downward from October to December by between 40-80 basis points (bps) for different quarters over a 12-month projection horizon. The additional downside surprise relative to December projections has been small, around 10 bps on a quarterly basis. Inflation expectations of households as measured by RBI’s survey (IEH) reveal a softening by 80 bps at 3-month horizon and 130 bps at 12-month horizon, possibly reflecting the adaptive nature of household expectations in response to the softness of recent inflation prints; importantly, they too indirectly confirm the ground reality and revision in inflation perceptions, especially in food and fuel categories. 62. Based on these data and other considerations, RBI’s quarterly inflation projections over the next 12-month horizon have been further revised downward and imply headline inflation steadily rising but remaining below the target rate of 4%. 63. My understanding of composition effects and risks around these projections is as follows: 64. One, inflation excluding food and fuel remains elevated and persistent, so it seems crucial to understand if the sharp increase in momentum observed in health and education components is one-off or not. While it seems reasonable to treat it as one-off for now, if it does sustain then it could push inflation excluding food and fuel into uncomfortable territory. Unfortunately, there is no decisive way to resolve this issue other than to wait for and analyse a few more prints. 65. Second, international Brent crude prices have stabilised in the short run. Nevertheless, it is too early to forget or rule out the wild gyrations from geopolitical risks, as were observed over the past six months. Given our oil imports and the implied current account deficit effects, headline inflation responds particularly adversely to upside risk from crude oil prices. 66. Third, the recent low momentum in food prices is assumed to have a structural component over the next 12-month horizon as there appears to be a supply glut in several food items at both domestic and international levels. Vegetable prices, however, are vulnerable to sudden reversal from their deflationary momentum. 67. More importantly, the assumption of sustained low momentum in food prices leads to a consideration of the risk of agrarian distress. Such distress will necessitate a political-economy response in the form of fiscal support to the agrarian economy in the short run; effects of such fiscal support may play out partly over the next 12 months and partly beyond. Besides stimulating rural demand and restoring rural wages, such a response could get generalised into headline inflation; this could arise, for example, by aggravating the input cost push arising in the financing of the real economy from fiscal and quasi-fiscal financing, especially from national small savings fund (NSSF) into bank deposit rates and from fiscal/quasi-fiscal market borrowings into corporate bond yields. Our counterfactual exercises suggest that such upward pressure on headline inflation would require commensurate policy rate action over the next 12 months. 68. In other words, the assumption of particularly benign food inflation in the short run imparts significant upside risk to the inflation trajectory, at the short- and/or medium-term horizons, from the fiscal adjustments that would be necessary to address resulting agrarian distress and to boost rural demand. 69. Fourth, while inflation expectations have moved downward in the most recent survey, when compared to the December 2017 survey, they remain higher at 3-month horizon. In other words, anchoring of inflation expectations of households is still an ongoing process and it is somewhat early to assume its sustenance going forward based on the most recent adjustment. 70. On balance, I remain concerned about (i) the elevated level of inflation excluding food and fuel; (ii) upward risks that could emanate from oil prices and fiscal implications of sustained food deflation; and, (iii) lack of adequate and sustained downward adjustment in household inflation expectations over the past 12 months. 71. Turning to growth, concerns around global growth, especially in major advanced economies and emerging markets embroiled in tariff wars, have gathered momentum. In response, several central banks have decided to be patient with their rate hike plans and/or have revised growth projections downwards. My assessment is that unless these concerns turn into recessionary risks, they could in fact be positive for the Indian economy as a reduction in aggregate global demand keeps Brent crude oil prices under check. 72. Domestic indicators for economic activity are overall mixed. Overall corporate performance in Q3 of 2018-19 was stable; capacity utilisation – absolute or seasonally-adjusted – has remained robust and close to or above 75 for past two quarters; PMI manufacturing and services continue to remain in expansion mode at healthy levels; and consumer sentiment surveyed by the RBI has improved. The primary weak coincident economic indicators have been auto sales and production. Our internal research suggests that this weakness reflects in part the lagged impact of high fuel prices during Q2 and part of Q3 of 2018-19, an effect that should gradually reverse, as well as due to one-off policy changes such as in emission standards and third-party insurance requirement. 73. Traditional measures of the output gap suggest some opening up, i.e., realised output below the potential output; however, my preferred measure, the finance-neutral output gap, remains positive, i.e., realised output is slightly above the potential output, as it captures the healthy aggregate credit growth and stable stock market performance. This is also consistent with the elevated level of inflation excluding food and fuel. 74. Combining my inflation and growth assessments, and given the Monetary Policy Committee (MPC)’s mandate to target headline inflation at 4% on a durable basis while paying attention to growth, I prefer to “take off the helmet” but “stay within the crease”. That is, I vote for a change in the stance from “calibrated tightening” to “neutral” to retain policy flexibility at future dates based on incoming data, but to hold the policy rate at 6.5%. Given the elevated level of inflation excluding food and fuel, our counterfactual exercises do not suggest any room for accommodation; keeping the policy rate at 6.5% under these exercises turns out to be “just right” over the medium term. 75. In my view, a rate cut decision now would be heavily dependent on the assumption of sustained weak momentum of food prices all through the next 12 months, which, as I explained, must be viewed as coincident with significant upside risk from fiscal measures needed to address agrarian distress. It seems better to me, in times of presently healthy levels of growth, to wait till the next policy by when uncertainties I have highlighted, especially around one-off surprises in health and education inflation, oil prices, and global recessionary risks, could resolve. The growth print for Q3 would also be available by then for understanding any soft spots in the domestic real economy and their drivers. 76. Finally, recall that I did vote for a rate cut in August 2017; at that point of time, all components of inflation had experienced downward trends, upside risks to inflation had reduced, and growth was weaker. That constellation of parameters gave me greater comfort to cut the policy rate than at the present juncture. Should a similar situation evolve in the next two months, I would have greater clarity for future policy action. Statement by Shri Shaktikanta Das 77. The CPI inflation print of December at 2.2 per cent continued to surprise on the downside. The overall food group continued to remain in deflation with the decline in food prices becoming more broad-based. Five constituents of the food group – vegetables, sugar, pulses, eggs and fruits – were in deflation in December. Fuel inflation also decelerated significantly mainly due to a sharp decline in the price of liquefied petroleum gas (LPG). Inflation excluding food and fuel also moderated, dragged down mainly by the decline in the prices of petrol and diesel in line with the decline in international petroleum product prices. Housing inflation continued to edge down. However, inflation in household goods and services; health; recreation and amusement; and education firmed up in December 2018. 78. Going forward, the outlook for food inflation is expected to be benign in the backdrop of excess domestic supply conditions in many food items. The lower prices in the international markets in food items also limit the avenues for exports to address the domestic surplus. This will be an important factor in keeping the overall inflation low. Soft crude oil prices augur well for keeping the petroleum product inflation under check and this will help in containing the input costs for goods and services. Inflation expectations of households have declined significantly in the last round, which is a welcome development. CPI inflation is projected at below four per cent in the remaining four quarters – 2.8 per cent in Q4:2018-19, 3.2-3.4 per cent in H1:2019-20 and 3.9 per cent in Q3:2019-20 – with risks broadly balanced. Beyond the near-term, however, there is a need to guard against some uncertainties surrounding the inflation outlook such as (i) abrupt reversal in vegetable prices; (ii) haziness in the oil price outlook; (iii) the recent unusual spike in the prices of health and education, which calls for vigilance; and (iv) the impact of several budget proposals on the aggregate demand, though the full effect of the measures will materialise over a period of time. 79. Turning to the growth outlook, the CSO has placed India’s real GDP growth at 7.2 per cent in 2018-19. Looking further ahead, there are signs of domestic growth slowing down somewhat, compared to the Reserve Bank’s earlier projections. The more recent high frequency indicators point to investment demand losing some traction, with production of capital goods and import of capital goods contracting in recent months. High frequency indicators also suggest moderation in demand (passenger cars, consumer durables, motorcycles and tractor sales). 80. On the supply side, rabi sowing so far has been marginally lower than the previous year, with shortfall across crops. There is, however, an expectation that the acreage will increase in the remaining part of the sowing season. Extended winter conditions are also likely to have a positive impact on overall wheat productivity. High-frequency and survey-based indicators for the manufacturing and services sectors suggest some slowdown in the pace of activity. In the services sector, growth of foreign tourist arrivals and international air passenger traffic decelerated in recent months. However, indicators of the construction sector such as consumption of steel and production of cement continued to show healthy growth, though growth in cement production was lower in November 2018. 81. Overall financing conditions have been improving, with bank credit growth in double digits and the total flow of resources to the commercial sector significantly higher than a year ago. Credit flows to services (such as non-banking financial companies, transport operators and trade) and in the personal loans category, especially housing, have been robust. However, credit growth has yet to become broad-based. Credit flows to industry, in particular, have been anaemic; credit to micro and small industry contracted in December 2018, while credit to large industry expanded at a moderate pace. 82. Global growth is also losing traction amidst lingering trade tensions and uncertainty around Brexit. On the positive side, crude oil prices remain soft, though the benefit for net exports could be restricted due to slowing global demand. GDP growth for 2019-20 is projected at 7.4 per cent – in the range of 7.2-7.4 per cent in H1, and 7.5 per cent in Q3 – with risks evenly balanced. 83. Growth impulses have weakened and there is a need to spur private investment and strengthen private consumption, especially in the wake of slowing global growth. Inflation readings since the December 2018 policy have shown a sharp decline. The overall food outlook remains benign and the headline inflation one-year ahead is projected to remain below the target level of 4 per cent. Risks to inflation at this stage are also broadly balanced around the baseline. Hence, space has opened up for policy action to address the growth concerns in pursuance of the provisions of the RBI Act as amended in 2016. The favourable macroeconomic configuration that is evolving underscores the need to act decisively. The time is opportune to seize the initiative and create a congenial environment for growth to revive and ensure a sustained trajectory. Hence, I vote for a reduction in the policy repo rate by 25 basis points. I also vote for a change in the stance of monetary policy from calibrated tightening to neutral. This change in the stance has been largely factored in by market participants after the December MPC meeting and the post policy press conference. The neutral stance will provide flexibility and the room to address challenges to sustained growth of the Indian economy over the coming months, as long as the inflation outlook remains benign. Jose J. Kattoor

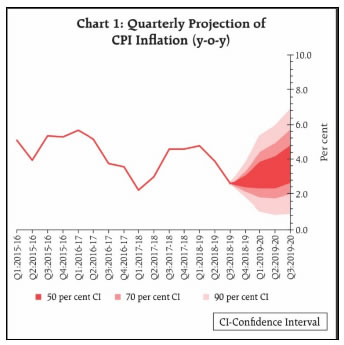

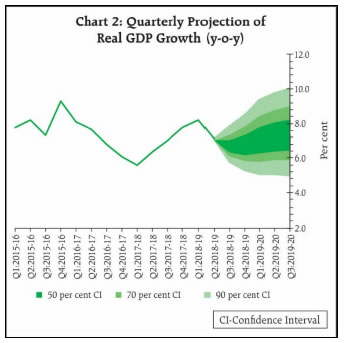

Chief General Manager Press Release: 2018-2019/2002 |