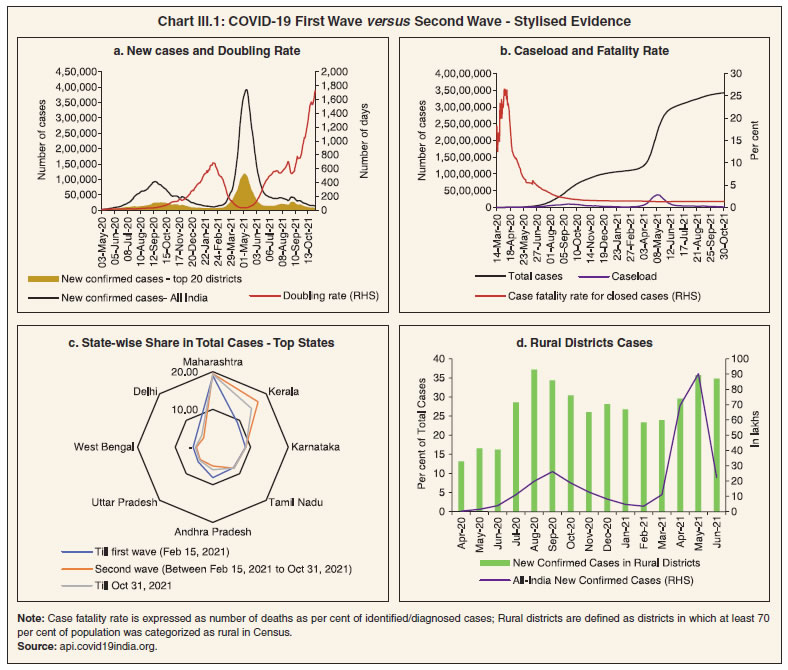

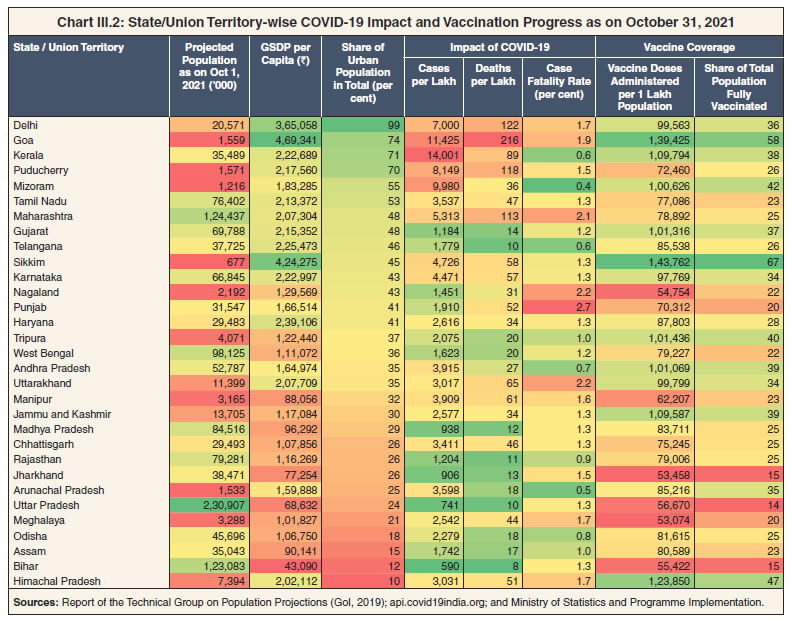

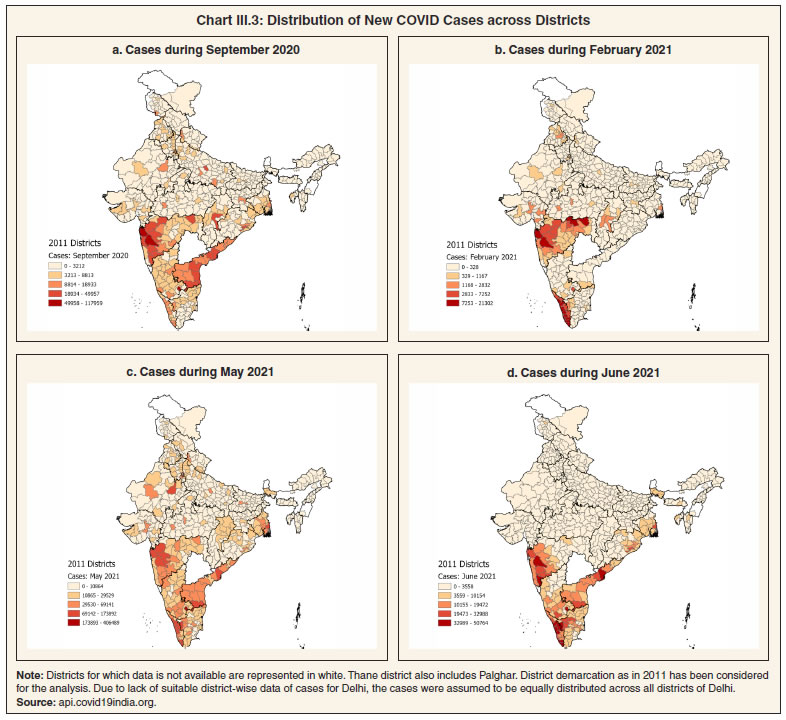

1. Introduction 3.1 The COVID-19 pandemic - a once-in-a-lifetime health crisis - is marked by heterogeneity in terms of its differentiated impact on health, economic and fiscal parameters across States, districts and cities. In response, all tiers of the government came together to work in coordination in order to contain its spread, mitigate its deleterious impact and alleviate the scars it left on lives and livelihoods. In this war effort against the pandemic, the role of local governments (LGs) has been pivotal, particularly from the point of view of mobilising a community-wide response. It is in this context that the theme “Coping with the Pandemic: A Third-Tier Dimension” has been chosen for this year’s report on State Finances, as a sequel to last year’s report which had adopted “Pandemic and its Spatial Dimensions in India” as its theme. 3.2 Like in the case of State governments, the finances of the third-tier governments were impacted severely during the pandemic. Restrictions on movement of people, goods and services, ramping up of health infrastructure, measures taken to protect livelihood and efforts taken to inoculate the citizens in a short span of time inflicted a heavy toll on their finances via a ‘scissor effect’ – an increase in expenditure due to a sharp rise in demand for public healthcare services with a simultaneous decrease in revenue resulting from the slowdown in economic activity. As local governments in India cannot run a deficit by law1, the adoption of innovative strategies to cope with the fiscal pressure became an imperative. The Central and State governments also extended support and LGs coordinated with the private sector and civil society to share the financial burden of the crisis. 3.3 This chapter drills down into the fiscal aspects of the role of third-tier governments across various States in India in containing the pandemic and bringing succour to those affected by it. The focus is on urban local bodies (ULBs), particularly municipal corporations (MCs). Qualitative responses obtained from 141 MCs across all the States in India through a primary survey conducted by the Reserve Bank have been used in this analysis. In addition, available budgetary data on 20 largest MCs spread across various States in India, which together account for around 60 per cent of revenue and 55 per cent of expenditures of the entire population of MCs, have been used. 3.4 The chapter is organised into 6 sections. Section 2 presents stylised facts on the spread and intensity of COVID-19 at the third-tier level. Section 3 discusses the efforts of local governments in terms of containment, vaccination and treatment. Section 4 examines the impact of the pandemic on local government finances. Section 5 delves into the steps taken by MCs to fill resource gaps. Section 6 concludes with the key lessons from this experience. 2. Spread and Intensity of COVID-19 in India 3.5 The first wave of the pandemic began with a gradual spurt in new cases from March 2020 onwards, and peaked around mid-September 2020, before reaching its lowest point in mid-February 2021. The second wave started from around mid-March 2021 and reached its peak on May 6, 2021. In contrast to the first wave, the rise in new cases during the second wave was steep and reached a much higher peak, primarily attributed to the significantly higher viral load of the Delta variant, rendering it more transmissible. Interestingly, the fall was equally sharp as cases reached about one-eighth of the peak by June 30, 2021. As regards concentration of cases, the share of top 20 districts2 in new cases was high in lean periods of low infections compared to phases in which cases were spiking at the all-India level (Chart III.1a). Reflecting the steep rise in new cases, the doubling rate3 declined sharply during the second wave as against a consistent increase during the first wave. While the sharp rise in new cases during the second wave significantly increased the caseload4, the case fatality rate5 remained stable (Chart III.1b).  3.6 Eight States accounted for close to 70 per cent of the total cases throughout and the relative share of each of these States remained broadly stable (Chart III.1c). Rural areas were relatively less affected as their share in new confirmed cases remained less than 40 per cent even at the peak of the first and second waves (Chart III.1d). While the most urbanised States in India tend to have higher number of COVID-19 cases per million, the case fatality rate does not show any clear association between infections and urbanisation (Chart III.2). 3.7 Furthermore, the spatial spread of COVID-19 was asymmetric across districts within a State. At the beginning of the first wave (May 2020), cases were concentrated in only a handful of districts – Mumbai, Chennai, Thane, Pune and Ahmedabad – but by September 2020, infections had spread more widely, with the higher number of cases mostly in Maharashtra, Andhra Pradesh and Delhi. As cases receded and reached a trough in February 2021, pockets of high infections remained restricted to certain districts of Maharashtra and Kerala. In March 2021, cases were on the uptick again and Maharashtra continued to witness a high concentration of cases, particularly in Pune, Mumbai, Nagpur and Thane districts. By May 2021, i.e., at the peak of the second wave, contagion had spread through peninsular India and some districts in north-western and eastern India. While 40 districts accounted for around 70 per cent of infections in March 2021, nearly 150 districts accounted for two-third of the spread in May 2021. With cases dropping sharply in June, infections remained concentrated mostly in peninsular India (Chart III.3).

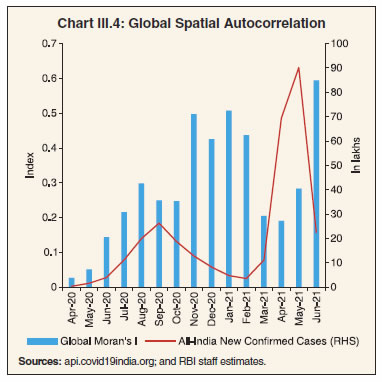

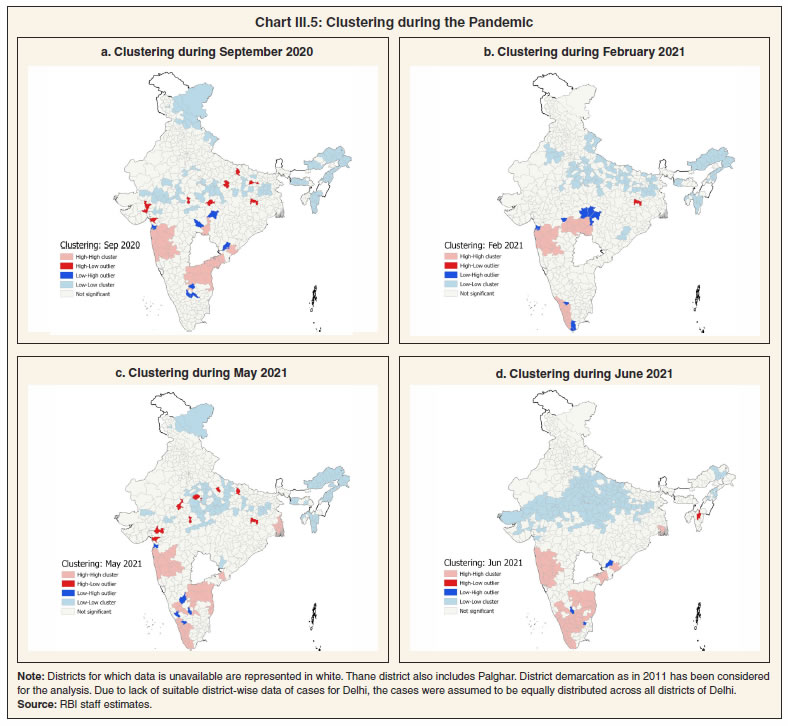

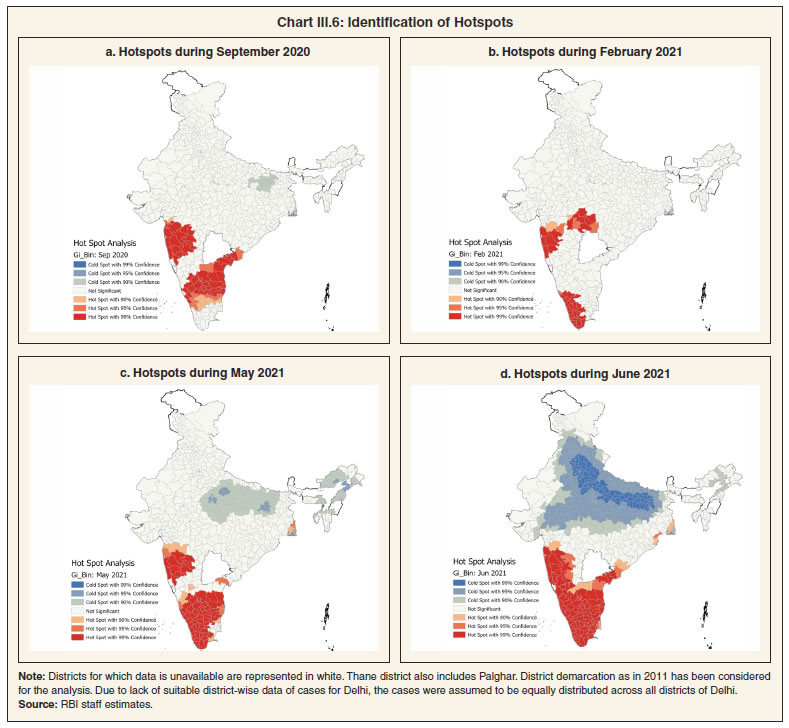

3.8 Spatial autocorrelation6 measured by Global Moran’s I7 is found to be positive and statistically significant during all months from May 2020 to June 2021, denoting the presence of clusters (Chart III.4). The value of the statistic is, however, higher when infections are low (e.g., during November 2020-February 2021), suggesting a higher degree of clustering when the cases are low than otherwise. 3.9 In a cluster and outlier analysis, a district with high infections which is also surrounded by districts with high infections, is represented as a high-high cluster. A high-low outlier refers to a district that has a high cases but is surrounded by districts with low cases. Likewise, low caseload districts that are surrounded by districts with high infections are denoted as low-high outliers and if the district as well as surrounding districts have low infections, it is represented as a low-low cluster. High-high clusters were mostly observed in Peninsular India. In contrast, districts in North-East India, Ladakh, and Uttar Pradesh were generally found to be low-low clusters. High-low outliers were mostly observed during the peak infection months of September 2020 and May 2021 in the districts of Ahmedabad, Surat, Bhopal, Jabalpur, Prayagraj, Ranchi, Kota, Patna, Vadodara, Gwalior, Lucknow and Gorakhpur. Only a few districts emerged as low-high outliers, majorly – Valsad, Krishnagiri, Malkangiri, Wardha, Balaghat (during peak of first wave) and Valsad, Chitradurg, Kodagu, Nilgiris (during peak of second wave) – pointing to successful mitigation strategies (e.g., strict checking at district entry points) or natural advantages (like low population density or better climatic conditions) in these districts (Chart III.5).  3.10 The identification of hotspots can help in devising control strategies to avoid the spread of infections. Accordingly, the Getis-Ord Gi* statistic8 identified statistically significant hotspots majorly in five districts – Mumbai, Pune, Thane, Raigad and Nellore – at the beginning of the outbreak in May 2020. By September 2020, however, hotspots covered much of Maharashtra, Andhra Pradesh, and parts of Karnataka, Tamil Nadu and Kerala. By February 2021, the number of hotspots had narrowed down to majorly certain districts of Maharashtra and Kerala, and got further confined to primarily within Maharashtra by March 2021. Thereafter, as the COVID cases resurged with the advent of the second wave, Kerala, Tamil Nadu, parts of Maharashtra, Karnataka and Andhra Pradesh, and few districts of West Bengal emerged as significant hotspots. Even when cases ebbed in June, these hotspots remained broadly unchanged (Chart III.6). There could be several factors, both natural (e.g., climatic factors; population density) and social (e.g., migration; severity of government response) that determine the spread of infections (Wang et al., 2021).

3. Role of Third-Tier Governments in the Pandemic 3.11 The core functions of local governments had to be scaled up rapidly during the pandemic to meet multiple objectives, viz., emergency healthcare need of the people, implementation and enforcement of lockdown restrictions, and uninterrupted delivery of essential services. 3.1 Strategies adopted by Urban Local Bodies 3.12 City government authorities in India9 had to escalate public healthcare services by ramping up testing facilities; setting up makeshift hospitals and quarantine centres; conducting door-to-door surveillance for tracking and contact-tracing; establishing COVID war rooms and 24*7 COVID helplines for providing tele-counselling and tele medicines; containing infections through sanitisation and solid waste management; and augmenting frontline staff capacity. The functioning of administrative and police systems in cities had to be reoriented to enforce lockdown restrictions, night curfews, demarcation of containment zones and entry restrictions in public places. As a part of citizen-centric support, many cities made arrangements for providing shelter, essentials and free food to the poor via community kitchens, tie-ups with food delivery aggregators and other State-run programmes. 3.13 The strategies adopted by various city authorities also leveraged on technology-based smart solutions. For instance, several cities deployed all-in-one mobile COVID-19 tracking apps for tracking and monitoring of COVID-19 cases; used the global positioning system (GPS) and geo-fencing to track the movement of quarantined and health workers; and employed heat mapping technology to draw up containment plans (Annex III.1). Survey Responses 3.14 Responses received from 141 MCs to an online qualitative survey show that some MCs responded in all the relevant areas of concern viz., public health; sanitisation; and enforcing social distancing norms, while others were only required to sanitise public places or enforce social distancing/ activity restrictions (Chart III.7). 3.15 Under healthcare services, MCs made arrangements for COVID testing mainly through the MC-owned hospitals, public health centres and other government hospitals. Given the inadequacy of public health infrastructure, some MCs also made testing arrangements through private hospitals (Chart III.8a). During the second wave of the pandemic, the MCs added hospital beds and created additional quarantine capacity (Chart III.8b). 3.16 MCs also took extensive support from private sector and non-governmental organisations (NGOs) to bridge the gap between the steep rise in demand for health and quarantine facilities and the existing infrastructure (Chart III.9). 3.2 Strategies adopted by Panchayati Raj Institutions 3.17 Even though rural districts account for less than 30 per cent10 of total COVID-19 cases in India, the caseload was huge in absolute terms vis-à-vis the medical facilities available in the hinterland. From time to time, the Union Ministry of Panchayati Raj issued advisories to State governments regarding preventive measures to be taken by Gram Panchayats (GPs) to curb the spread of COVID-19 in rural India.11 Based on these guidelines and advisories the GPs undertook a host of measures which inter alia included lockdowns, entry restrictions, formation of Corona Monitoring Committees at the village level, free online medical consultation, awareness programmes, creation of migrants database and free food distribution (Annex III.2).

3.3 Progress of Vaccination Roll Out 3.18 With the ebbing of the second wave, the pace of vaccination has picked up across various States in India in recent months. As per information available up to November 27, 2021, 31.0 per cent of India’s population has been fully vaccinated while 52.7 per cent received at least the first dose (Chart III.10).12 Local governments played an important role in the vaccination drive by making arrangements for inoculation in public and private hospitals; authorising and monitoring vaccination camps organised by civic and housing societies; making special transportation arrangement for senior citizens and differently abled people to vaccination centres; and spreading awareness to remove vaccine hesitancy among people. 4. Fiscal Impact of COVID-19 on Third-Tier Government 3.19 In line with the global experience, the pandemic has worsened the finances of local governments in India substantially in 2020-21 and 2021-22. It is estimated that local authorities would lose around 15-25 per cent of their revenues in 2021, which may make the maintenance of the current level of service delivery difficult to sustain (Wahba et al. 2021). In rural India, village panchayats struggled for funds during the pandemic (Gurusaravanan, 2021). Similar challenges were encountered by the ULBs. 98 per cent of the respondents to the Reserve Bank’s qualitative survey13 of MCs reported different financial challenges viz., increase in expenditure; decline in revenue collection; and lack (or delayed release) of funds from the State governments during the second wave of the pandemic. 70 per cent of MCs reported a decline in revenue while 71 per cent reported an increase in expenditure (Chart III.11). Several MCs had to cut down expenditure on other areas to make available funds for the COVID response. 3.20 The loss of revenue by MCs seems to have been steeper during the second wave - 22 per cent of them reported revenue loss of more than 50 per cent during the second wave as against 16 per cent during the first wave (Chart III.12a and III.12b). Like in the case of revenue, the impact on expenditure of MCs was more pronounced during the second wave with 11 per cent of them reporting expenditure growth of more than 50 per cent during the second wave as against 6 per cent during the first wave (Chart III.12c and III.12d).

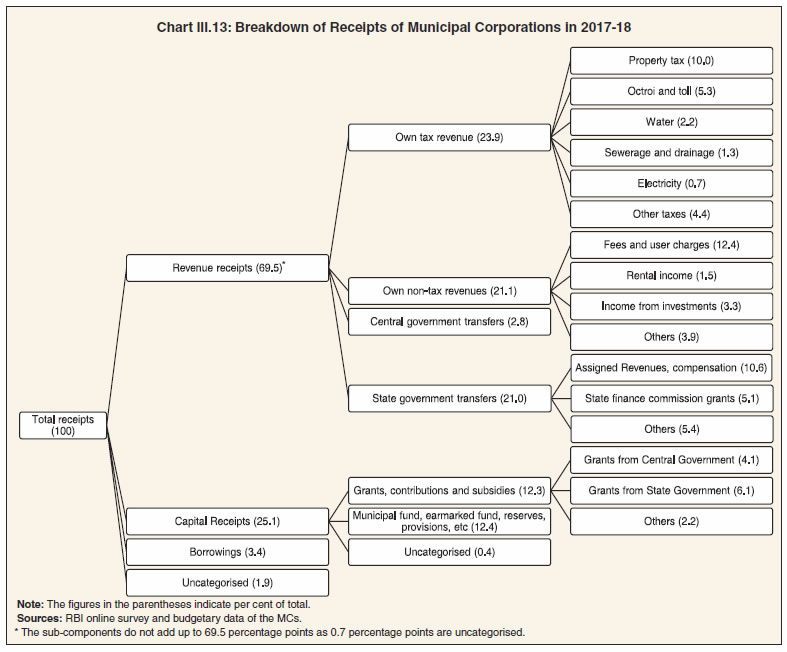

4.1 Impact on Revenue 3.21 Revenue receipts account for around 70 per cent of total receipts of MCs in India whereas capital receipts account for about 30 per cent (Chart III.13). MCs’ revenue receipts largely comprise own tax revenue; non-tax revenue; and transfers from the Central and the State governments. Property tax is the dominant component of own tax revenue, whereas fees and user charges constitute the largest sub-component of non-tax revenue. The share of transfers, predominantly State government transfers, in revenue receipts is significant. The capital receipts of MCs mainly comprise grants, contributions and subsidies from central and State governments and transfers from funds maintained by municipal bodies. The share of borrowings in total receipts of municipal bodies is relatively low (less than 5 per cent).  3.22 An analysis of budgetary data on 20 large municipal corporations14 reveals that their tax revenue increased by 7.2 per cent during 2020-21 (revised estimates) over 2019-20 levels (Table III.1). The growth in tax revenue was mainly driven by property taxes whereas collections under water tax, sewerage/drainage tax and octroi and toll tax witnessed sharp declines. Collections under all components of tax revenue during 2020-21 (revised estimates) were significantly lower than the respective budget estimates. Assigned revenues, compensation from State governments and rental income from municipal properties recorded modest growth in 2020-21 (revised estimates) over 2019-20 but remained much lower than the budget estimates. Revenue grants, contributions and subsidies from the Central and the State governments is the only component which overshot the budget estimates, indicative of higher transfers from the upper tiers of the governments to support municipal finances during the first wave of the pandemic. The MCs have budgeted robust growth in almost all components of revenue in 2021-22. 4.2 Impact on Expenditure 3.23 Revenue expenditure accounts for about two thirds of total disbursements of MCs (Chart III.14). Fixed overheads in the form of establishment expenditure (largely towards salaries, wages and bonus, and pensions) account for more than 50 per cent of revenue expenditure. The other large revenue expenditure categories are operational and maintenance expenses and administrative expenses. Capital expenditure accounts for around 30 per cent of total disbursements, and is largely spent on creation of fixed assets. Disbursement towards repayment of borrowings has a relatively low share of around 3 per cent (Chart III.14). | Table III.1: Receipts of Municipal Corporations | | (Growth in Per cent) | | Revenue Receipts | 2020-21 | 2021-22 | | 2020-21 Budget Estimates over 2019-20 Actuals | 2020-21 Revised Estimates over 2019-20 Actuals | 2020-21 Revised Estimates over 2020-21 Budget Estimates | 2021-22 Budget Estimates over 2020-21 Revised Estimates | | 1 | 2 | 3 | 4 | 5 | | 1. Tax Revenue | 28.0 | 7.2 | -16.3 | 17.2 | | Of which | | | | | | Property Tax | 31.1 | 20.3 | -8.2 | 11.6 | | Water Tax | 15.2 | -10.0 | -21.9 | 29.1 | | Sewerage/Drainage Tax | -2.7 | -26.2 | -24.2 | 37.8 | | Electricity Tax | 13.8 | 6.2 | -6.7 | 7.9 | | Professional Tax | 31.0 | 8.6 | -17.2 | 14.0 | | Octroi and Toll | 68.5 | -62.0 | -77.4 | 100.8 | | 2. Assigned Revenues and Compensations | 31.3 | 1.4 | -22.8 | 10.2 | | 3. Rental Income from Municipal Properties | 38.0 | 6.9 | -22.6 | 20.1 | | 4. Fees and User Charges | 97.3 | 47.7 | -25.2 | 5.1 | | 5. Revenue Grants, Contributions and Subsidies | 25.1 | 29.2 | 3.3 | 3.2 | | 6. Income from Investment | -2.9 | -32.4 | -30.4 | 6.5 | | 7. Interest Earned | -0.3 | 5.4 | 5.7 | -25.5 | | Source: Budgetary data of 20 large MCs. |

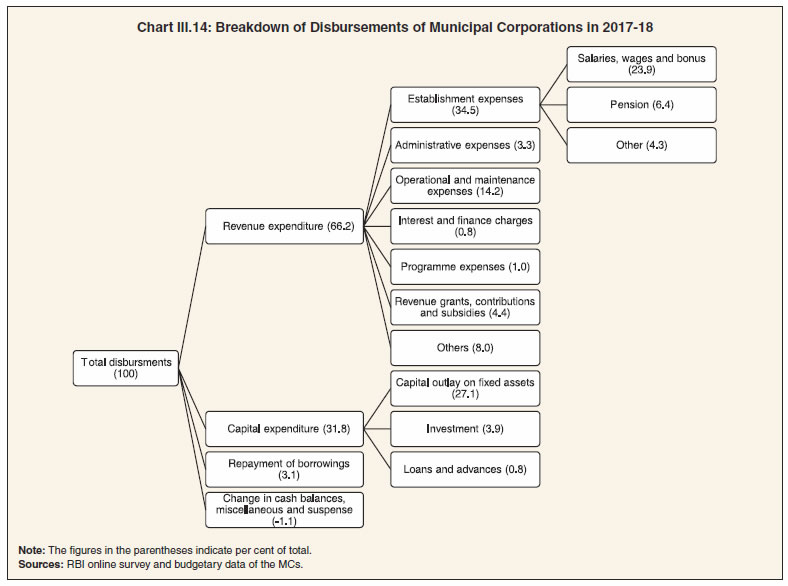

3.24 All the major components of revenue expenditure, viz., establishment expenses, administrative expenses, operation and maintenance expenses and interest and finance charges – most of which are committed in nature – witnessed an increase in 2020-21 (revised estimates) over 2019-20 (Table III.2). Establishment expenses of the MCs (salaries, wages, bonus and pension), however, were lower than the budget estimates, reflecting efforts by MCs to cutback on expenses in view of the revenue shortfall. Capital expenditure of the MCs recorded robust growth in 2020-21 (revised estimates) albeit remaining lower than the budgeted amount. The MCs have budgeted modest growth in all components of revenue expenditure in 2021-22, and robust growth in capital expenditure. 3.25 The MCs’ expenditure on public services, viz., health, sanitation, roads and education witnessed robust growth in 2020-21 but fell short of budget estimates (Table III.3). The MCs have budgeted strong growth in expenditure under all major categories of public services in 2021-22, anticipating the need for continuance of COVID-19 related expenses. The MCs’ inability to meet the budgetary target of expenditure on public services in 2020-21 even at the time of pandemic reflects their fiscal constraints arising out of revenue shortfalls and limited opportunities for market borrowings, as statutorily they cannot run a deficit (Box III.1). Increasing fiscal stress of the MCs may act as a hindrance to effective mitigation of future pandemic-type crises (Box III.2). | Table III.2: Revenue and Capital Expenditure of the Municipal Corporations | | (Growth in Per cent) | | Disbursements | 2020-21 | 2021-22 | | 2020-21 Budget Estimates over 2019-20 Actuals | 2020-21 Revised Estimates over 2019-20 Actuals | 2020-21 Revised Estimates over 2020-21 Budget Estimates | 2021-22 Budget Estimates over 2020-21 Revised Estimates | | 1 | 2 | 3 | 4 | 5 | | I. Revenue Expenditure | 30.9 | 22.2 | -6.6 | 3.9 | | 1. Establishment Expenses | 30.2 | 13.2 | -13.1 | 5.7 | | Of which: | | | | | | a. Salary, Wages and Bonus | 27.2 | 6.7 | -16.1 | 12.4 | | b. Pension | 13.7 | 8.8 | -4.3 | 6.0 | | 2. Administrative Expenses | 28.6 | 21.8 | -5.3 | 9.8 | | 3. Operation and Maintenance Expenses | 34.6 | 37.4 | 2.0 | 1.4 | | 4. Interest and Finance Charges | 24.8 | 36.4 | 9.3 | -14.0 | | II. Capital Expenditure | 155.7 | 59.4 | -37.7 | 58.9 | | Source: Budgetary data of 20 large municipal corporations. |

| Table III.3: Expenditure on Select Public Services by the Municipal Corporations | | (Growth in Per cent) | | Public Services | 2019-20 | 2020-21 | 2021-22 | | 2019-20 Actuals over 2018-19 Actuals | 2020-21 Budget Estimates over 2019-20 Actuals | 2020-21 Revised Estimates over 2019-20 Actuals | 2021-22 Budget Estimates over 2020-21 Revised Estimates | | 1 | 2 | 3 | 4 | 5 | | Health & Sanitation | 0.9 | 47.5 | 32.3 | 5.9 | | Water Supply | 6.7 | 71.6 | 17.6 | 45.4 | | Roads | -7.7 | 93.6 | 41.6 | 5.2 | | Education | -16.8 | 71.9 | 42.9 | 17.8 | | Sewerage | 15.0 | 71.4 | 15.6 | 39.7 | | Solid waste management | 14.4 | 40.7 | 13.3 | 14.8 | | Energy/lighting | -0.5 | 32.8 | 16.6 | 21.8 | | Source: Budgetary data of 20 large MCs. |

Box III.1:

Fiscal Stress on Indian Municipal Corporations Fiscal stress is a situation in which a government institution faces a growing imbalance between its receipts and expenditures (Premchand, 1993). Existing fiscal stress testing frameworks generally measure the impact of different factors which directly or indirectly affect the projected receipts and expenditures of the government. However, measuring fiscal stress of MCs in India using these traditional stress testing methods may not be efficient and may make model selection difficult, as the municipal finance data in India is characterised by a lack of uniform accounting practices with differences in accounting classifications and presence of incomplete/missing data. The modern approach of maximum likelihood estimation (MLE) has weaker assumptions and provides improved statistical properties. The primary benefit of using MLE techniques for missing data is to produce estimates which are consistent, efficient, and asymptotically normal. Accordingly, a gradient boosting model based on the MLE technique has been used to assess fiscal stress of the MCs.  In India, statutorily, the MCs cannot run a deficit and their revenue receipts must exceed revenue expenditure while presenting budgets. The MCs can resort to borrowings only after explicit approval from their respective State governments (ICRIER, 2019). Thus, the fiscal balance alone may not be a sufficient indicator of fiscal stress on MCs. In view of this, apart from fiscal balance, two more indicators of fiscal stress have been used for the analysis. On the revenue side, the MCs’ own revenue as a ratio of total revenue receipts has been used as an indicator of fiscal stress. A higher share of own revenue in total revenue receipts indicates greater autonomy or conversely lower dependence of the MCs on transfers from upper tiers of the government to meet their expenditure needs thus reducing their fiscal stress. On the expenditure side, the share of committed expenditure15 in total expenditure has been considered as a stress factor as a considerable amount of municipal expenditure is committed in nature and cannot be altered in the short run. The budgetary data of 221 MCs collected for the period 2017-18 to 2019-20 has been used for the analysis. In the gradient boosting model, a higher probability score implies higher stress16. Probability scores presented as percentile plots in Chart I show that around 30 to 35 per cent of the MCs out of 221 are severely fiscally stressed17 on account of either of the three parameters. A composite index of fiscal stress has been estimated by taking the average of three separate probability scores for fiscal balance, fiscal autonomy and committed expenditure. The overall fiscal stress index exhibits a bell-shaped distribution with almost half of the MCs having a moderate fiscal stress, with index values lying between 0.3 to 0.6. The composite fiscal stress index has identified 15 per cent of the MCs as severely stressed with index value above 0.8 in a scale of 0 to 1. For these MCs, the relatively higher share of committed expenditure (as per cent of total expenditure) is the primary contributor to fiscal stress (Chart II). References: Hastie, T.; Tibshirani, R.; Friedman, J. H. (2009). “Boosting and Additive Trees”. The Elements of Statistical Learning (2nd ed.). New York: Springer. pp. 337-384. ISBN 978-0- 387-84857-0. ICRIER (2019). “State of Municipal Finances in India: A Study Prepared for the Fifteenth Finance Commission”. Hellwig, Klaus-Peter (2021). “Predicting Fiscal Crises: A Machine Learning Approach,” IMF Working Papers 2021/150, International Monetary Fund. Premchand, A. (1993). “Managing Fiscal Stress”. Public Expenditure Management. USA: International Monetary Fund. Retrieved Nov 14, 2021, from https://www.elibrary.imf.org/view/books/071/05487-9781557753236-en/ch03.xml. |

Box III.2:

Does Fiscal Health Impact Vaccination Drive? Empirical Study of Select Municipal Corporations Municipal corporations (MCs) have been at the forefront of the vaccination drive in India. They have been running vaccination centres; dispersing information about vaccine availability and distribution through their websites and social media platforms; and undertaking awareness campaigns and public outreach programmes to sensitise people about the need for vaccination. Keeping in view the role of MCs in the vaccination programme, it is worthwhile to empirically examine if the fiscal health of the MCs influences progress in vaccination. The empirical investigation is carried out through cross-sectional regression of district vaccination rates on municipal fiscal health for the period February-October 2021.18 The fiscal health of a MC is proxied by its per capita total receipts19. Since vaccination rates20 are likely to be influenced by the disease burden, district-wise infections (as per cent of district population) are included as a control variable. | Table I: Regression Estimates (Dependent Variable: Vaccination Rates) | | | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | | Infection cases | -1.160

(3.876) | 0.189

(0.852) | 4.800***

(1.459) | 1.636***

(0.341) | 2.396**

(1.036) | 5.091***

(1.278) | 5.223***

(0.742) | -0.0761

(0.746) | -4.551***

(0.979) | | Receipt | 0.0773

(0.048) | 0.186***

(0.039) | 0.171

(0.114) | 0.256***

(0.019) | 0.773***

(0.058) | 0.661***

(0.063) | 0.757***

(0.061) | 1.006***

(0.090) | 0.635***

(0.106) | | Cons | 0.008***

(0.001) | 0.035***

(0.002) | 0.053***

(0.007) | 0.035***

(0.003) | 0.081***

(0.004) | 0.096***

(0.004) | 0.136***

(0.005) | 0.177***

(0.005) | 0.132***

(0.006) | | adj. R2 | 0.320 | 0.265 | 0.592 | 0.460 | 0.537 | 0.543 | 0.435 | 0.479 | 0.230 | | N | 147 | 147 | 147 | 147 | 147 | 147 | 147 | 147 | 147 | Note: Standard errors in parentheses; * p < 0.10, ** p < 0.05, *** p < 0.01.

Source: RBI staff estimates. | The outcomes of the empirical estimation show that MCs with better fiscal health were able to achieve higher vaccination rates (Table I). Vaccination rates also depend on cases – higher infection rates are generally associated with higher vaccinations, barring the first few months when the vaccination strategy was focussed on vulnerable groups (healthcare and frontline workers) and during September-October when all-India cases had come down substantially. As MCs with higher per capita receipts could achieve a higher vaccination rate, strengthening local government finances is key to augment India’s capacity to tackle future health crises successfully. | 5. Steps taken by the Municipal Corporations to fill Resource Gaps 3.26 Before the onset of the pandemic, the consolidated revenue balance21 of the MCs was in surplus. Budgetary data relating to 20 large MCs indicate that their combined revenue surplus22 declined in 2020-21, with many of them recording either a fall in the revenue surplus or an increase in the revenue deficit (Chart III.15a). Segregating MCs into revenue surplus (group A) and revenue deficit (group B) categories, it is observed that the reduction in the surpluses of group A MCs was sharper than the increase in the revenue deficit of group B MCs (Chart III.15b). 3.27 MCs adopted a combination of measures to bridge COVID-19-induced resource gaps. The survey responses reveal that apart from reduction of non-essential expenditure, the MCs also mobilised additional funding from multiple sources such as borrowing, grants from the States and the Centre, reserves, municipal funds, deposits in State Disaster Response Funds (SDRF), issuances of COVID bonds, donations and contribution (Chart III.16), which are discussed below. Additional Funding Support from the Central and State Governments 3.28 The international experience reveals that Central governments across the world announced fiscal measures to help sub-national governments cope with the fiscal shocks23 imparted by the pandemic. For instance, two-thirds of the OECD countries have adopted funding measures in support of sub-national governments (OECD, 2020). In India, MCs receive grants from the States and the Centre to bridge their financial gaps. Revenue grants are given to run current expenses, while capital grants are disbursed to run project-specific expenses (which are long-term in nature). The FC XV recommended provision of grants amounting to ₹70,051 crore to strengthen and plug critical gaps in the healthcare system. Around 43 per cent of the respondents to the survey reported use of grants from the State governments to meet pandemic-related needs of funding. Use of Reserve Funds 3.29 Reserves held by the MCs proved to be the second important source of financing - 19 per cent of the survey respondents reported drawing from reserve funds to meet the resource gap. These reserves are linked to either the infrastructure sector or committed liabilities such as provident and pension funds. Ideally, the infrastructure-linked funds should be channelised towards capital expenditure with long-term growth prospects so as to form a source of future income. The fiscal stress caused by the pandemic forced MCs to withdraw from these reserves. 26 per cent of surveyed MCs indicated that they created special reserve funds to cope with higher spending. Borrowings 3.30 During the pandemic, MCs largely depended on transfer from upper tiers of the government and their accumulated reserves. Borrowing by MCs came into prominence, albeit in a supplemental role. About 6 per cent of surveyed MCs borrowed from State governments and another 2 per cent borrowed from banks to meet the additional need for funds during the pandemic. Another source of funds was Issuance of bonds. In the pre-COVID period, some MCs had issued municipal bonds at different points of time to finance their infrastructure. For instance, Ahmedabad Municipal Corporation issued a ‘muni bond’ worth ₹200 crore in 2019 (maturity of 5-years and 8.7 per cent coupon), to fund urban infrastructure development. Centre-driven schemes like AMRUT24 were used to incentivise bond issuances by ULBs, resulting in fresh issuances of around ₹1,800 crore worth of municipal bonds by nine MCs25. During the COVID-19 period, Ghaziabad Municipal Corporation issued its first green bond26 in India on April 08, 2021 to raise ₹150 crore with a coupon rate of 8.10 per cent for a tertiary water treatment plant to benefit industries in Ghaziabad. Five MCs responding to the survey issued bonds to finance COVID-related expenditure. Other Sources 3.31 Private participation (including NGOs) in pandemic management also helped ease the MCs’ financial burden. 22 per cent of surveyed MCs availed help from these institutions in different forms such as quarantining, treatment, ambulances, sanitisation, oxygen concentrators, food and shelter. Other sources of funding were District Mineral Funds (DMFs)27, SDRF, contributions from the public, municipal staff and other donations, and additional revenue generated through better tax compliance by providing incentives to taxpayers. Reduction/Freezing of Non-essential/Discretionary Spending 3.32 Among the surveyed MCs, 18 per cent reported expenditure cuts relating to non-essential areas. Guidelines were issued to head of departments to restrict expenditure to a certain proportion of budgeted allocations till a specific month or to incur only essential spending like establishment expenses, spending for COVID prevention, electric charges, payment of property tax, water tax, and urgent repair and maintenance works. Discretionary spending like expenditure on renovation and decoration of office premises, purchase and hiring of additional vehicles except for health/sanitation work/carrying emergency staff, and withdrawal from the general provident fund (GPF) except for urgent treatment, education, and marriage-related expenditure were restricted. 6. Lessons and Conclusions 3.33 The impact of the pandemic has been heterogeneous across time and space, warranting the adoption of localised approaches for crisis management rather than a centralised response. During the second wave, the third-tier echelons of government became frontline pandemic warriors. Their involvement in the COVID-19 response became the catalyst for forging vistas of cooperation with civil society, NGOs and the private sector in mitigating the pandemic’s impact. It is in this context that a key lesson can be derived from the pandemic experience – the importance of strengthening local government finances. 3.34 Before the pandemic, local governments across the world suffered from insufficient budgets, over reliance on funds from upper tiers of government, lack of access to new sources of revenue, limited autonomy to change/introduce taxes, and low levels of taxpayer compliance. COVID-19 amplified these structural constraints on local government finances and brought to the fore new challenges such as revenue volatility and demand for public services and investments in areas which were not required earlier. In other words, COVID-19 has increased the responsibilities of local governments towards delivery of public services manifold. 3.35 In India, the role of MCs in cities that were the hotspots became pivotal. As a consequence, their budgets came under severe strain, forcing them to cut down discretionary spending, use reserves and other contingency funds, including resources from funds linked to the infrastructure sector or committed liabilities. This diversion of funds may have serious consequences for the financial sustainability of cities in the short to medium term. On the positive side, many of the MCs in India have now created special reserve funds to cope with future pandemics. This imparts a degree of resilience to their finances. 3.36 Going forward, increasing the financial autonomy of civic bodies, strengthening their governance structures and financially empowering them via higher resource availability, including through own resource generation are critical for their effective intervention at the grassroot level. 3.37 Financial autonomy notwithstanding, the importance of transfers from upper tiers of the government during a crisis cannot be overemphasised. During the pandemic, inter-governmental transfers were among the least affected sources of revenue. Thus, strengthening and streamlining transfers from upper tiers of government through institutionally sound mechanisms can help fortify the financial stability of MCs. 3.38 There are several facets of municipal finances that merit reforms. Greater fiscal transparency, revitalising the municipal bond market, boosting developmental/infrastructure finance and green finance, exploiting land-based financing opportunities and developing partnerships with impact finance in the private space would all strengthen the third tier, and make it viable and effective, especially in managing and mitigating future crises.

Annex III.1:

Initiatives by Municipal Corporations in Combating the COVID-19 Pandemic | | Initiatives/ Corporation | Shimla Municipal Corporation | Surat Municipal Corporation | Bhopal Municipal Corporation | Madurai Municipal Corporation | | Tracking and Monitoring | • Closing of public places and Suvidha Kendras

• Deployment of Nodal Officers for monitoring and surveillance of quarantined households | • Launching of COVID-19 quarantine reporting app

• Establishment of COVID-19 war room

• Surveillance in Slums

• Tracking acute respiratory cases | • Aerial surveillance using drones

• Contact tracing through mobile app and portal

• Developing a dashboard for all COVID-19 data analysis | • Establishment of 24*7 control room

• Barricading of containment zones | | Diagnostics and Sanitisation | • Appointment of Zone Nodal Officers and involvement of Local Area Committees in COVID management

• Sanitisation of public places

• Hill Challenge Cleaning Campaign

• Waste collection from quarantined homes and isolation centres | • Augmentation of health care facilities

• Regular sanitisation and disinfection by the corporation

• Setting up hands free hand washing facilities in slums

• Solid waste management | • 24*7 Tele-Counselling and Video Counselling facilities

• Use of Drones for disinfection across the city | • Setting up mobile clinics for screening influenza like symptoms

• Daily testing of citizens in containment zone for respiratory infections

• Disinfection through spraying machinery | | Awareness and Capacity Building | • Sensitising corporation sanitation staff about COVID-19

• Communication via Hoardings

• Ensuring Sanitation and awareness in slums | • Capacity building of frontline staff

• Raising awareness in slums | • Influencer for Good: An initiative to tackle the spread of fake news and ensure that citizens receive verified and accurate information

• Verified information dissemination through Visual Media Displays, digital billboards and the city’s public addressing system | • Pasting of hand washing awareness stickers with the telephone number of the control room as well as contact details of medical teams at public places

• Posting of flex banners, posters and notices in key areas

• Fitting of public addressal systems in 100 Madurai Corporation vehicles for raising awareness continuously both in the morning and the evening | | Citizen Centric Support | • Establishment of control room and WhatsApp number for citizen grievances

• Safety and security of sanitation staff

• Honouring CORONA warriors

• Waiving off penalties and interest on delayed payments of various services

• Reaching out to labourers | • Setting up toll-free COVID Helpline number

• Ensuring food and shelter for the needy

• Distribution of essentials items | • Usage of non-contact ‘SNA Dispenser’ for citizens

• Use of technology-based app to track food distribution and deployment of relief vehicles across Bhopal | • Supply of essential commodities through engaging a fleet of light commercial vehicles

• Establishment of community kitchen to provide food free of cost

• Proper barricading and strict maintenance of social distancing in city vegetable markets

• Counselling of COVID-19 patients’ family members by trained counsellors and doctors to counter the stigma around COVID-19 | | Sources: Various municipal corporations’ websites. |

Annex III.2:

Initiatives taken by Panchayati Raj Institutions in Rural Areas | | State | Initiatives | | Andhra Pradesh | • Formulation of Corona Monitoring Committee at village level

• Resolution of ‘No Mask No Entry’ at the Gram Panchayat (GP) level

• Sanitisation and door to door surveillance | | Assam | • Formulation of Village Defence Party

• Creation of Migrant Database

• Funds from FC XV untied grants earmarked for sanitisation | | Bihar | • Mask distribution among all families in the village

• Utilisation of FC XV grants for sanitisation | | Gujarat | • Self-proclaimed lockdowns imposed by the Panchayati Raj Institutions

• Door to Door surveillance through pulse oximeter, temperature guns and antigen test kits

• Formulation of Gram Yodhhasamiti for supporting families of patients | | Haryana | • Periodic awareness programs

• Formulation of Village Monitoring Committees

• Arrangement of sanitisation, ration and isolation centers for migrant labourers | | Himachal Pradesh | • Door to Door Surveillance

• Distribution of Ration and Medical Kits for Corona infected families

• Distribution of ration to migrant labour and marginalized section | | Jharkhand | • Conversion of Panchayat Bhawans, Government Schools and Community Halls into Quarantine Centers

• Implementation of complete lockdown at GP level

• Prohibition of entrance of the external people at village level

• Formation of Corona volunteers

• Production and distribution of face mask

• Awareness generation camp through mobile van and wall painting

• Development of community kitchen in the Hazaribagh district to provide cooked meals to stranded migrant labourers, people at quarantine centers, senior citizens, and students, as well as poor and vulnerable households

• Development of contactless, low-cost, telephone booth-style sample collection center in West Singhbhum district | | Karnataka | • Task Forces have been revived at the village level with participation from primary health centre doctor, auxiliary nurse midwives and accredited social health activists

• Decisions on COVID-19 related management such as implementing the lockdown, disinfection, providing food to those who need it and ensuring the supply of other essential services were implemented by these village-level task forces | | Kerala | • Formation of Panchayat War Room

• Formation of Kudumbashree Community Network

• Formation of Ward Sanitation Committees

• Preparation and management of COVID Care and quarantine centres | | Madhya Pradesh | • Establishment of containment zones in villages with high infection

• Formation of Red, Orange and Green zones in villages

• Establishment of control rooms at Block, District and State level | | Maharashtra | • Formation of Corona Prevention Committee

• Door to Door surveillance for checking vitals and any medical emergency

• My Family My Responsibility awareness campaign

• Distribution of food grains by sarpanches to the villagers’ doorstep

• Free distribution of anti-biotic, soap and sanitizers to the villagers | | Odisha | • Initiatives by Gram Sabhas in various districts to provide food grains to poor families and cooked meals to poor individuals who had no families

• Distribute soaps and liquid handwash to all households in the villages

• Generate awareness and enabling access to food and income security schemes | | Punjab | • Formation of Village Monitoring Committee in each village

• Strict mobility restrictions from other states | | Sikkim | • Distribution of sanitizer and protective mask by all GPs to villagers

• Identification of poor families and migrant workers eligible for free rations from the State Government

• Awareness measures for social distancing and lockdown | | Uttar Pradesh | • Formation of Village Nirgani Samiti at all gram panchayats to promote cleanliness

• Dedicated Safai Karmacharis in every village for regular cleaning, fogging and mopping

• Financial assistance for cremation of COVID related deaths | | Uttarakhand | • Formation of Village Monitoring Committee in every GP

• Establishment of 24*7 Help Desk System

• Formation of Block Response Team at Block level to monitor deliverables | | West Bengal | • Awareness generation drives by the GPs

• Enabling safe operation of local markets/ haats

• Distribution of food ration to daily wage-earning households | | Sources: GoI (2020; 2021); Raghunandan (2020); and Sen and Palit (2020). |

|