An approach paper to accelerate financial inclusion to promote economic wellbeing, prosperity and sustainable development The National Strategy for Financial Inclusion 2019-2024 sets forth the vision and key objectives of the financial inclusion policies in India to help expand and sustain the financial inclusion process at the national level through a broad convergence of action involving all the stakeholders in the financial sector. The strategy aims to provide access to formal financial services in an affordable manner, broadening & deepening financial inclusion and promoting financial literacy & consumer protection.

I Introduction I.1 Financial inclusion is increasingly being recognized as a key driver of economic growth and poverty alleviation the world over. Access to formal finance can boost job creation, reduce vulnerability to economic shocks and increase investments in human capital. Without adequate access to formal financial services, individuals and firms need to rely on their own limited resources or rely on costly informal sources of finance to meet their financial needs and pursue growth opportunities. At a macro level, greater financial inclusion can support sustainable and inclusive socio-economic growth for all. I.2 There has been a growing evidence on how financial inclusion has a multiplier effect in boosting overall economic output, reducing poverty and income inequality at the national level. Financial inclusion of women is particularly important for gender equality and women’s economic empowerment. With greater control over their financial lives, women can help themselves and their families to come out of poverty; reduce their risk of falling into poverty; eliminate their exploitation from the informal sector; and increase their ability to fully engage in measurable and productive economic activities. An inclusive financial system supports stability, integrity and equitable growth. Therefore, financial exclusion because of several barriers like physical, socio-cultural and psychological, warrants attention from the policy makers. Some of the key reasons resulting in involuntary exclusion are: Financial Inclusion and United Nations Sustainable Development Goals I.3 It is also noteworthy to state that, seven1 of the seventeen United Nations Sustainable Development Goals (SDG) of 2030 view financial inclusion as a key enabler for achieving sustainable development worldwide by improving the quality of lives of poor and marginalized sections of the society. (Home- Sustainable Development Goals, 2018) Defining Financial Inclusion in the Indian Context I.4 Financial inclusion has been defined as “the process of ensuring access to financial services, timely and adequate credit for vulnerable groups such as weaker sections and low-income groups at an affordable cost”. (Committee on Financial Inclusion - Chairman: Dr C Rangarajan, RBI, 2008). The Committee on Medium-Term Path to Financial Inclusion (Chairman: Shri Deepak Mohanty, RBI, 2015) has set the vision for financial inclusion as, “convenient access to a basket of basic formal financial products and services that should include savings, remittance, credit, government-supported insurance and pension products to small and marginal farmers and low-income households at reasonable cost with adequate protection progressively supplemented by social cash transfers, besides increasing the access of small and marginal enterprises to formal finance with a greater reliance on technology to cut costs and improve service delivery, ….” Financial Inclusion Strategy - Rationale I.5 While a lot of efforts have been undertaken to increase financial inclusion in the country (See Chapter III- Status of Financial Inclusion in India) a lot of steps are further needed to ensure adequate access to financial services and usage of these services by various segments of under-served and un-served population in India, so far. Anchored in the country’s development priorities, the NSFI 2019-2024 seeks to address the inherent barriers of access to a gamut of financial products and services. An inclusive financial system (ably supported through sound financial inclusion policies, focus on financial education and customer protection) is not only pro-growth but also pro-poor with the potential to reduce income inequality and poverty, promote social cohesion and shared economic development. Financial exclusion, on the other hand, leaves the disadvantaged and low- income segments of society with no choice other than informal options, making them vulnerable to financial distress, debt, and poverty.  I.6 The National Strategy for Financial Inclusion for India 2019-2024 has been prepared by RBI under the aegis of the Financial Inclusion Advisory Committee and is based on the inputs and suggestions from Government of India, other Financial Sector Regulators viz., Securities Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI) and Pension Fund Regulatory and Development Authority of India (PFRDA). This document also reflects various outcomes from wide-ranging consultation held with a range of stakeholders and market players, including National Bank for Agriculture and Rural Development (NABARD), National Payments Corporation of India (NPCI), Commercial Banks and Corporate Business Correspondents etc. It includes an analysis of the status and constraints in financial inclusion in India, specific financial inclusion goals, strategy to reach the goals and the mechanism to measure progress. II Cross Country Analysis and Lessons II.1 With increased recognition globally and United Nations Sustainable Development Goals (SDGs) emphasising financial inclusion as a key enabler for achieving sustainable development worldwide, countries across the globe are developing suitable strategies and policies to increase access and usage of formal financial services. Achieving Universal Financial Access by 2020 (UFA 2020) has been one of the key developmental agenda of the World Bank which aims to provide adults who currently aren’t part of the formal financial system, with access to a transaction account to store money, send and receive payments to manage their financial lives. (Universal Financial Access 2020, 2018) To achieve this ambitious goal, the World Bank Group has committed to enable one billion people to gain access to a transaction account through targeted interventions. It also works with countries to strengthen the following key building blocks: public and private sector commitment, enabling legal and regulatory framework, and bolstering financial and ICT infrastructure, and globally, through engagement with standard-setting bodies to come up with recommendations and guidelines that will advance access to transaction accounts. II.2 Each country’s strategy and progress towards financial inclusion is unique because of significant variations in the Government’s priorities, institutional capacity to implement reforms, evolution of financial markets, payments infrastructure, financial capability of people, and cultural beliefs that drive financial behaviour. Therefore, a mere review of various countries’ financial inclusion policies without understanding their socio-economic background, political system, and culture and beliefs, will not be sufficient to draw insights for designing and developing our own Financial Inclusion strategy. It would nevertheless still be meaningful to look into and draw inferences based on the experiences and feedback of the financial inclusion policies of other countries. Similar to National Identity System put in place by various countries, India has also introduced Aadhaar in 2009. Recognizing the importance of financial education, the current Strategy considers Financial Education as one of the important pillars of the NSFI as visualized by other countries. II.3 Globally, the adoption of a formal National Financial Inclusion Strategy (NFIS) has accelerated significantly in the past decade. By mid-2018, more than 35 countries, including Brazil, China, Indonesia, Peru and Nigeria have launched a NFIS and another 25 countries are in the process of developing a strategy. Further, several countries have also updated their original NFIS (World Bank Group, 2018). Some of the important commonalities observed in the strategies of a few countries have been reviewed and are summarised below. Leadership II.4 A strong leadership (visionary or charismatic) is important to achieve financial inclusion goals. Financial inclusion policies require time to realize their full potential. Therefore, having a long-term vision and a well-coordinated approach is essential. Target Based Approach II.5 Financial inclusion policies are generally targeted towards specific sectors like MSME, Agriculture or specific regions like Aspirational Districts. It is important to develop sector specific action plans and monitor targets and review the progress. Regulatory Framework II.6 There should be a strong regulatory and legal framework aimed at protecting the interests of the customers, promoting fair practices and curbing market manipulations. Further, the regulations should have adequate space to allow flexibility and openness for innovations. This calls for incorporating a Test and Learn Approach in the form of Regulatory Sandboxes along with encouraging Pilot projects to reach long term viability and mitigate losses. Market Development II.7 Market development and deepening thereof, through various regulatory initiatives for catering to the needs of the target groups is vital. While a Universal Banking system can continue to provide services to existing clientele, there may also be a case for permitting differentiated entities that leverage technology to provide low cost, high volume services. The process of market development can be in the form of expansion of rural networks and access points; allowing preferential prudential rules to encourage lending to rural areas and setting up special sub-branches in rural areas; digitising large-scale payment streams like pension, insurance, and subsidies for rural households etc. as also proliferation of new institutions, products and services. Strengthening Infrastructure II.8 Development of an ecosystem with requisite infrastructure, including credit infrastructure, receipt and payment infrastructure etc., are essential. Providing a national level identification, setting up a credit registry database, creation of open and inclusive payment systems are some of the key steps in this direction. Putting in place a suitable framework for using national level identification number for cashless and paperless financial transactions, based on customer consent can simplify customer on-boarding and also ease in operations. Further, this facilitates a large volume of Government to Person (G2P) transactions and vice-versa (P2G), directly through bank accounts. Development of robust payments infrastructure coupled with regulations can foster competition and orderly growth which result in more customer centric products, increased choices and convenience. Developing a robust credit database also helps lenders to take an informed decision on the credit proposals. Last Mile Delivery II.9 Focus on Last Mile Delivery has been one of the major thrust areas in various countries. Since the typical rural customer would not be willing to forego his/ her day’s wage to visit a financial service provider, it is important that distance and resulting time taken to visit the service provider does not act as a deterrent. To achieve this, various countries have come up with policies to extend the receipt infrastructure including permitting formal financial institutions to engage services of agents and Business Correspondents (BCs). While the Business Correspondents have been able to reach out to the last mile customer, the issue of customer protection, providing suitable products, increasing financial awareness, having a proactive oversight over the activities of the agents and sustainability of the agent/BC network are some of the areas which now require policy interventions. Innovation and Technology II.10 Innovation and Technology in the overall landscape have resulted in rise of fin-tech entities which leverage technology to offer financial services. While these new entities have the potential to increase competition and provide the customer with greater choice through suitable products and easier processes, they may also exclude those customers who do not have the basic infrastructure like internet connectivity and access to smart phones. It is therefore imperative to have a balance between technology and agents to provide customers with adequate handholding. Since technology evolves very rapidly, oversight on the technology led institutions is of utmost importance and their regulation needs constant upgradation. Financial Literacy and Awareness II.11 Financial literacy continues to gather global attention as it is increasingly being realised that only an informed customer will be able to take proper financial decisions. Financial literacy enables a customer to have necessary awareness about the available products, ability to choose the right product and available mechanism for grievance redressal. Emphasis is now on to increase the financial awareness among various vulnerable groups in the society viz., women, youth, children, elderly, small entrepreneurs, etc. who require handholding. Focus has been on the development of various scientific tools and design approaches combining concept literacy with process literacy. With more and more usage of digital mode of transactions, financial literacy in the realm of digital financial services has assumed importance. Consumer Protection II.12 Considering that the new entrants to the financial system are likely to be more vulnerable, customer protection and grievance redressal has become an important pillar for furthering sustainable financial inclusion. This is further accentuated by the fact that there has been a steep increase in access to digital financial services which calls for a robust customer protection framework. Some of the measures undertaken include increased market monitoring, creation of a strong enforcement machinery to redress customer grievances and improved coordination between the financial sector supervisors, particularly relating to cross-product and cross-market issues. Monitoring and Evaluation II.13 Periodic monitoring and evaluation of the progress made in financial inclusion sphere can help in identifying the bottlenecks and also initiate corrective measures. Countries and various institutions are recognizing the need for reliable financial inclusion data, to get an overview on parameters relating to access, usage, and quality of financial services rendered. II.14 Financial inclusion is a much-cherished policy objective for India and its economic policy has always been driven by an underlying intent of a sustainable and inclusive growth. The next chapter summarises the initiatives undertaken in India in the financial inclusion domain and our achievements especially in the light of the foregoing learnings. The chapter also highlights some of the critical challenges that act as barriers for financial inclusion. III Status of Financial Inclusion in India III.1 The policy makers in India have been aware of the implications of poverty for financial stability and have continually endeavoured to ensure that poverty is tackled in all its manifestations and that the benefits of economic growth reaches the poor and excluded sections of the society. III.2 India began its financial inclusion journey as early as in 1956 with the nationalisation of Life Insurance companies. This was followed by nationalisation of banks in 1969 and 1980. The general insurance companies were nationalised in 1972. A review of the status of financial inclusion in India indicates that a host of initiatives have been undertaken over the years in the financial inclusion domain. III.3 India has also been actively engaged with other countries and multilateral fora viz. Global Partnership for Financial Inclusion (GPFI) and Organization for Economic Co-operation and Development (OECD). India is one of the co-chairs along with Indonesia and United Kingdom in the GPFI Subgroup on Regulation and Standard Setting Bodies. India has been actively involved in preparation of relevant research and policy guides in Digitalisation, Regulation and Financial Inclusion that are published by GPFI from time to time. Further, the Reserve Bank of India is currently a member of four working groups viz. Standards, Implementation and Evaluation, Digital Financial Literacy, Financial Education for MSMEs and Core Competencies for Financial Literacy under the International Network for Financial Education (INFE), set up under OECD. Keeping in view the various developments in the global front, India has also initiated the process of preparing its National Strategy for Financial Inclusion (NSFI) in June 2017 under the aegis of Financial Inclusion Advisory Committee (FIAC). The document has been formulated, based on the feedback received from various stakeholders viz., Department of Financial Services (DFS), and Department of Economic Affairs (DEA), Ministry of Finance (MoF), Govt of India, RBI, SEBI, IRDAI, PFRDA, NABARD and NPCI. Leadership III.4 A strong leadership (either a visionary or charismatic) is a prerequisite to drive financial inclusion in a mission mode. Indian policy making has shown unswerving resolve for inclusive growth which culminated in the National Mission for Financial Inclusion, namely the Pradhan Mantri Jan Dhan Yojana (PMJDY). Launched in August 2014, it was a watershed in the financial inclusion movement in the country. The programme leverages on the existing large banking network and technological innovations to provide every household with access to basic financial services, thereby bridging the gap in the coverage of banking facilities. III.5 Under PMJDY, 34.01 crore2 accounts have been opened with deposits amounting to ₹89257 crore upto January 30, 2019 within a short span of five years. The achievement of opening the largest number of accounts (1,80,96,130 nos.) under PMJDY, in one week has found a place in the Guinness Book of World Records. A bouquet of products viz., overdraft of ₹10,000, accidental death cum disability insurance cover, term-life cover and old age pension have been made available under PMJDY to the account holders. The focus has also shifted from opening account for “every household to every adult”. III.6 Under Pradhan Mantri Suraksha Bima Yojana (PMSBY) a renewable one- year accidental death cum disability cover of ₹2 lakhs is offered to all subscribing bank account holders in the age group of 18 to 70 years for a premium as low as ₹12/- per annum per subscriber. Another insurance product with one-year term life cover of ₹2 lakhs under Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) is made available to all subscribing bank account holders in the age group of 18 to 50 years, for a premium of ₹330/- per annum per subscriber. III.7 To take care of the financial needs in old age, a pension product named Atal Pension Yojana (APY) guaranteed by the Government of India has also been made available to the newly included bank account holders. Under APY, a subscriber (in the age group of 18 to 40 years) will receive fixed monthly pension in the range of ₹1,000 to ₹5,000 after completing 60 years of age, depending on the contributions made by the subscriber. Target based approach for specific sectors / regions A. Micro, Small and Medium Enterprises (MSMEs) III.8 MSMEs are considered the engines of growth of the Indian economy. They contribute nearly 31% to India’s GDP, 45% to exports and provide employment opportunities to more than 11.1 crore skilled and semi-skilled people. There are approximately 6.33 crore MSMEs in the country. A number of initiatives have been undertaken for facilitating credit off take in this sector. In order to bring about an attitudinal change in the mindset of the bankers while dealing with entrepreneurs from MSME sector, a special capacity building programme named ‘National Mission for Capacity Building of Bankers for financing MSME Sector’ (NAMCABS) was put in place to familiarise bankers with the entire gamut of credit related issues of the MSME sector. III.9 A Certified Credit Counsellors (CCC) scheme was launched for creating a structured mechanism to assist the entrepreneurs in preparing financial plans and project reports in a professional manner, thus facilitating the banks to make informed credit decisions. Web portals like the ‘Udyami Mitra’ and ‘psbloanin59minutes’ have also been launched to provide easy access to credit. Trade Receivables Discounting System (TReDS) platforms have been set up to address the problem of delayed payments to MSMEs. Pradhan Mantri Mudra Yojana (PMMY)3, a scheme to finance small business enterprises has been launched in April 2015 whereby lending institutions would finance to micro entrepreneurs up to ₹10 lakh. Interest subvention scheme has been launched for MSMEs to reduce cost of borrowings. B. Agriculture III.10 India’s agrarian economy is the source of around 15 percent of GDP, 11 per cent of exports and provides livelihood to about half of India’s population. The importance of the sector from a macroeconomic perspective is also reflected in a significant flow of bank credit to finance agricultural and allied activities relative to other sectors of the economy. III.11 To give a thrust to agriculture financing from the formal sector, banks have been mandated specific targets under priority sector scheme. Currently the target for agriculture lending under priority sector for all domestic scheduled commercial banks and foreign banks having more than 20 branches is 18 per cent of Adjusted Net Bank Credit (ANBC) or Credit Equivalent Amount of Off-Balance Sheet Exposure (CEAOBE), whichever is higher. Within the 18 per cent target for agriculture, a sub-target of 8 percent of ANBC or Credit Equivalent Amount of Off-Balance Sheet Exposure, whichever is higher is prescribed for Small and Marginal Farmers. The banks have been advised to extend collateral free loans to small and marginal farmers upto ₹1.6 lakh. To provide adequate and timely credit support from the banking system under a single window to the farmers for their cultivation & other needs an innovative product viz., Kisan Credit Card Scheme (KCC) was introduced in August 1998 as a revolving cash credit for ease of access and delivery. The scheme covers tenant farmers, oral lessees and share croppers and has now been extended to cover animal husbandry and fisheries. The scheme provides for sanction of the limit for 5 years with simplified renewal every year. C. Aspirational Districts III.12 In order to address regional disparity in inter-state and inter-district variations in development, ‘Transformation of Aspirational Districts’ programme was launched in January 2018. This initiative focuses on the strengths of each aspirational district which has been identified by a team of Senior Government officials through analysis of the district’s performance on a composite index of key data sets that included deprivation enumerated under the Socio-Economic Caste Census, key health and education sector performance and state of basic infrastructure. Under this programme, a set of attainable outcomes for immediate improvement have been identified while measuring progress and ranking the selected districts on the basis of their performance. This programme focuses on expeditiously transforming 117 identified districts across 28 states and driven primarily by the State governments. This initiative focuses closely on improving people’s ability to participate fully in the rapidly growing economy. The baseline ranking for the Aspirational Districts is based on 49 indicators across five sectors that include health and nutrition (30% weightage) through 13 indicators, education (30%) through 8 indicators, agriculture and water resources (20%) through 10 indicators, financial inclusion and skill development (10%) through 10 indicators, and basic infrastructure (10%) through 7 indicators. Regulatory Framework (i) Banking III.13 To protect the interest of the customers, promote fair business processes and prevent unhealthy practices by the market players, supporting regulatory and legal framework has been put in place. III.14 RBI has adopted a bank-led model to deepen financial inclusion. The banks were mandated to open branches nationwide especially in underbanked pockets which led to a considerable increase in bank branches and later Automated Teller Machines (ATMs) in the 1990s to early 2000. The banks were advised to draw up a roadmap for having banking outlets in villages with population more than 2000 (in 2009) and less than 2000 (in 2012). Subsequently the banks were advised to open brick and mortar branches in villages with population more than 5000. The banks were also advised to prepare Financial Inclusion Plans for a period of three years comprising key parameters viz., modes of delivery of financial services, access to Basic Savings Bank Deposit Accounts (BSBDAs) and transactions through the BC Channel. III.15 To strengthen financial inclusion, RBI has relaxed the branch authorisation guidelines in 2017 wherein fixed-point Business Correspondent outlets serving for more than 4 hours a day and five days a week are treated on par with physical brick and mortar branches. An exclusive fund viz., Financial Inclusion Fund (FIF) has been created to support adoption of technology and capacity building with an initial corpus of ₹2000 crore. III.16 To widen financial inclusion, RBI has issued differentiated banking license viz., Small Finance Banks (SFBs) and Payments Banks in 2015. The objective of setting up of SFBs was to further financial inclusion by provision of a savings vehicle and supply of credit to small business units, small and marginal farmers, micro and small industries and other unorganized sector entities, through high technology-low cost operations. Payments Banks have been set up to provide small savings accounts and payments/remittance services to migrant labour workforce, low income households, small businesses and other unorganised sector entities / other users. III.17 In order to strengthen the BC model of delivery and help prospective users to identify BC having good service track record, the BC Registry has been launched under the aegis of Indian Banks’ Association (IBA). For capacity building and to ensure certain minimum standards of service rendered by the BCs, a BC Certification course through Indian Institute of Banking and Finance (IIBF) has also been introduced. (ii) Insurance III.18 In addition to the initiatives / insurance products mentioned above, some of the other keyinitiatives undertaken in insurance sector4 include increasing awareness among citizens on the benefits and appropriateness of insurance and enabling greater availability of insurance products (including micro-insurance) through increasing the number of delivery channels including corporate agents and Common Service Centers. III.19 Further, leveraging on technology, Web Aggregators and Insurance Repositories have been set up, which facilitate access and storage of insurance policy details and enable issuance of insurance policies in an electronic form. III.20 For the protection of interests of policy holders and also in building their confidence in the system, the institution of Insurance Ombudsman has been created. This will ensure quick disposal of the grievances of the insured customers and also mitigate their problems involved in redressal of their grievances. To safeguard the interests of policyholders and customers catered to by the insurance companies / intermediaries under Health insurance segment, separate guidelines have been issued. (iii) Pension III.21 To regulate the National Pension System (NPS) and any other pension scheme not regulated by any other enactment, the Pension Fund Regulatory and Development Authority (PFRDA)5 was set up under the PFRDA Act, 2013. Besides the initiatives / pension products mentioned above, some of the other key initiatives undertaken in the pension sector include expansion of NPS through increasing the channels of distribution, developing capacity of the officials of its intermediaries and increasing awareness on old age income security and retirement planning. It has also leveraged on technology to drive efficiencies & improve ease of access to NPS for the subscribers and service providers. Market Development III.22 While the current model of Universal banking may continue to provide financial services to the existing clientele there has been a need for differentiated banking to cater to various niche segments. Accordingly, RBI has issued differentiated banking license for Small Finance Banks (SFBs) and Payments Banks in 2015. To increase access points and rural network, RBI has rationalised the branch authorisation guidelines in 2017. To ensure accurate targeting of the beneficiaries, de-duplication and reduction of fraud and leakage, Direct Benefit Transfer (DBT)6 has started on 1st January 2013. The first phase of DBT had been introduced in 43 districts and subsequently extended to 78 more districts under 27 schemes pertaining to scholarships, women, child and labour welfare. DBT has been further extended across the country since December 2014. 7 new scholarship schemes and Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) has been brought under DBT in 300 identified districts with higher Aadhaar enrolment. III.23 Jan Dhan Accounts, Aadhaar biometric ID and Mobile (JAM) are enablers which provide a unique opportunity to implement DBT in all welfare schemes across the country including States & UTs. The DBT has enabled efficiency, effectiveness, transparency and accountability in all Government to Persons (G2P) transfers. Strengthening Infrastructure III.24 To operate and introduce any payment system related entity / product, authorisation from RBI under The Payment and Settlement Systems Act, 2007 is essential. While RBI operates the large-value payment system (RTGS) and retail payment systems (NEFT), other retail payment system products (CTS, AEPS, NACH, UPI, IMPS etc.) are operated by National Payments Council of India (NPCI). With the popularisation of these retail payment system products, digital transactions have increased manifold. III.25 The Unique Identification Authority of India (UIDAI)7 has been created with the objective to issue Unique Identification numbers (UID), named as “Aadhaar”, linked to biometric identification, to all residents of India to eliminate duplicate and fake identities. The UIDAI has so far issued more than 120 crore Aadhaar numbers to the residents of India and has enabled use of technology to implement large-scale real-time Direct Benefit Transfers (DBTs) to bank accounts in order to improve economic lives of India’s poor beneficiaries. III.26 A Public Credit Registry (PCR) would enable better and faster underwriting standards for credit assessment and pricing by banks; risk-based, dynamic and counter-cyclical provisioning at banks; supervision and early intervention by regulators; and help in restructuring stressed assets effectively. III.27 To solve the problem of delayed payment to MSMEs, RBI had laid down guidelines foroperationalisation of Trade Receivables Discounting System (TReDS)8. TReDS was put in place to facilitate Electronic Bill Factoring Exchanges, which could electronically accept and auction MSME bills so that MSMEs could realize their of receivables without delay. Government of India has mandated that all companies with a turnover of more than ₹50 crore have to compulsorily register under TReDS. Last Mile Delivery III.28 To bridge the gap in the last mile connectivity, RBI permitted banks to engage Business Correspondents / Business Facilitators (2006). This has resulted in cost effective delivery of services through ICT based solutions. Another step to deepen financial inclusion in the countryhas been the launching of India Post Payments Bank (IPPB)9 in September 2018. IPPB is also leveraging the vast network of Department of Posts with 1.55 lakh Post Offices, more than 3 lakh postmen and Grameen Dak Sewaks to further scale up financial inclusion initiatives in the country. Financial Literacy and Awareness III.29 In order to spread financial education among the populace in the country, RBI has issued guidelines for financial literacy through Financial Literacy Centres (FLCs) and rural branches of banks. It has also advised banks to observe a “Financial Literacy Week” across the country simultaneously every year. Centres for Financial Literacy (CFLs) have been set up at block level, involving community participation in association with banks to spread financial literacy. Work is under progress to incorporate financial education in school curriculum in association with State Governments and also National Council for Educational Research and Training (NCERT). Further, National Centre for Financial Education (NCFE) has been set up by the financial sector regulators viz., RBI, SEBI, IRDAI and PFRDA as a Section (8) Company under Companies Act, 2013 to undertake co-ordinated efforts in disseminating basic financial literacy. Consumer Protection III.30 To strengthen the grievance redressal system, among other measures, suitable mechanisms in the form of Ombudsman Scheme by RBI, IRDAI and PFRDA have been put in place. Further, SEBI has also instituted a SEBI Complaints Redressal System (SCORES). Challenges III.31 Despite the various measures that have been undertaken by various stakeholders in strengthening financial inclusion in the country, there are still critical gaps existing in the usage of financial services that require attention of policy makers through necessary co-ordination and effective monitoring. 1. Inadequate Infrastructure: Limited physical infrastructure, limited transport facility, inadequately trained staff etc., in parts of rural hinterland and far flung areas of the Himalayan and North East regions create a barrier to the customer while accessing financial services. 2. Poor Connectivity: With technology becoming an important enabler to access financial services, certain regions in the country that have poor connectivity tend to be left behind in ensuring access to financial services thereby creating a digital divide. Technology could be the best bridge between the financial service provider and the last mile customer. Fintech companies can be one of the best solutions to address this issue. The key challenge that needs to be resolved would be improving tele and internet connectivity in the rural hinterland and achieving connectivity across the country. 3. Convenience and Relevance: The protracted and complicated procedures act as a deterrent while on-boarding customers. This difficulty is further increased when the products are not easy to understand, complex and do not meet the requirements of the customers such as those receiving erratic and uncertain cash flows from their occupation. 4. Socio-Cultural Barriers: Prevalence of certain value system and beliefs in some sections of the population results in lack of favourable attitude towards formal financial services. There are still certain pockets wherein women do not have the freedom and choice to access financial services because of cultural barriers. 5. Product Usage: While the mission-based approach to financial inclusion has resulted in increasing access to basic financial services including micro insurance and pension, there is a need to increase the usage of these accounts to help customers achieve benefits of relevant financial services and help the service providers to achieve the necessary scale and sustainability. This can be undertaken through increasing economic activities like skill development and livelihood creation, digitising Government transfers by strengthening the digital transactions’ eco-system, enhancing acceptance infrastructure, enhancing financial literacy and having in place a robust customer protection framework. 6. Payment Infrastructure: Currently, majority of the retail payment products viz., CTS, AEPS, NACH, UPI, IMPS etc. are operated by National Payments Council of India (NPCI), a Section (8) Company promoted by a group of public, private and foreign banks. There is a need to have more market players to promote innovation & competition and to minimize concentration risk in the retail payment system from a financial stability perspective. IV Strategic Objectives To achieve the vision of ensuring access to an array of basic formal financial services, a set of guiding objectives have been formulated with special relevance in the Indian context. This chapter elaborates on each of the objectives, lays down action plans and milestones and suggests broad recommendations to achieve the same. IV.1 Universal Access to Financial Services Every village to have access to a formal financial service provider within a reasonable distanceof 5 KM radius. The customers may be on boarded through an easy and hassle-free digitalprocess and processes should be geared towards a less-paper ecosystem. | Providing Universal Access to Financial Services by expanding the outreach is the key foundation for a successful financial inclusion strategy. Over the last five years, especially with the launch of the PMJDY in 2014, the total number of access points have increased in the country. However, there are a few parts in the country including difficult to reach terrain in the North Eastern Region, Left Wing Extremists affected districts and the aspirational districts in the country wherein the number of access points need to be increased to improve coverage. Recommendation In order to achieve the objective of providing universal access to financial services, it is important to provide a robust and efficient digital network infrastructure to all the financial service outlets / touch points for seamless delivery of the financial services. It is also recommended to extend the digital financial infrastructure to co-operative banks and other specialised banks (Payments Banks, Small Finance Banks) as well as other non-bank entities such as fertilizer shops, Office of the Local Government bodies / Panchayats, fair price shops, common service centres, educational institutions etc. to promote efficiency and transparency in the services offered to customers. Banks may endeavour to sort out issues relating to remuneration, need for furnishing cash-based collaterals and cash retention limits, etc. to strengthen the BC network. Action Plan and Milestones -

Increasing outreach of banking outlets of Scheduled Commercial Banks /Payments Banks/ Small Finance Banks, to provide banking access to every village within a 5 KM radius/ hamlet of 500 households in hilly areas by March 2020. -

Strengthen eco-system for various modes of digital financial services in all the Tier-II to Tier VI centres to create the necessary infrastructure to move towards a less cash society by March 2022. -

Leverage on the developments in fin-tech space to encourage financial service providers to adopt innovative approaches for strengthening outreach through virtual modes including mobile apps so that every adult has access to a financial service provider through a mobile device by March 2024. -

Move towards an increasingly digital and consent-based architecture for customer on-boarding by March 2024. IV.2 Providing Basic Bouquet of Financial Services Every adult who is willing and eligible needs to be provided with a basic bouquet of financialservices that include a Basic Savings Bank Deposit Account, credit, a micro life and non-lifeinsurance product, a pension product and a suitable investment product. | The National Mission for Financial Inclusion, namely the PMJDY has created the requisite infrastructure for providing every adult with access to a basic bouquet of financial services. However, it is found that efforts are still needed to provide access to insurance, pension and credit to the PMJDY account holders. Recommendation The objective of providing a basic bouquet of financial services can be achieved through designing and developing customized financial products by banks and ensuring efficient delivery of the same through leveraging of Fin-tech and BC networks. It is recommended that banks should strive for capacity building of their BCs so that they can be utilised for delivery of a wider range of financial products such as life/ non-life insurance products, pension products, mutual funds etc. Action Plan and Milestones: -

Every willing and eligible adult who has been enrolled under the PMJDY (including the young adults who have recently taken up employment) to be enrolled under an insurance scheme (PMJJBY, PMSBY, etc.), Pension scheme (NPS, APY, etc.) by March 2020. -

Capacity building of all BCs either directly by the parent entity or through accredited institutions by March 2020. -

Make the Public Credit Registry (PCR) fully operational by March 2022 so that authorised financial entities can leverage on the same for assessing credit proposals from all citizens. IV.3 Access to Livelihood and Skill Development The new entrant to the financial system, if eligible and willing to undergo any livelihood/ skilldevelopment programme, may be given the relevant information about the ongoing Governmentlivelihood programmes thus helping them to augment their skills and engage in meaningfuleconomic activity and improve income generation. | Globally, it is found that sustainable livelihood generation can bring people out from the clutches of poverty. Through adequate coordinated and collaborative effort between the banks, Government and Skill Development Agencies, new entrants to financial sector may be provided requisite information on the ongoing skill development programmes and livelihood missions of the Government. Recommendation While ensuring access to livelihood and skill development requires multi-dimensional efforts, it is recommended to attain convergence of objectives of various employment generation and skill development programmes like National Rural Livelihoods Mission (NRLM), National Urban Livelihoods Mission (NULM), Pradhan Mantri Kaushal Vikas Yojana (PMKVY) and other state level programmes through an integrated approach. New entrants to the formal financial system should be informed about such programmes and provided assistance through information dissemination and coordination. Action Plan and Milestones: -

All the relevant details pertaining to the ongoing skill development and livelihood generation programmes through RSETIs, NRLM, NULM, PMKVY shall be made available to the new entrants at the time of account opening. The details of the account holders including unemployed youth, and women who are willing to undergo skill development and be a part of the livelihood programme may be shared to the concerned skill development centres/ livelihood mission and vice versa by March 2020. -

Keeping in view the importance of handholding for the newly financially included SHGs/ Micro entrepreneurs, a framework for a focused approach ensuring convergence of efforts from civil society/ banks/ NGOs to increase their awareness on financial literacy, managerial skills, credit and market linkages needs to be developed by National Skill Development Mission by March 2022. IV.4 Financial Literacy and Education Easy to understand financial literacy modules with specific target audience orientation (e.g.children, young adults, women, new workers/ entrepreneurs, family person, about to retire,retired etc. in the forms of Audio-Video/ booklets shall be made available for understanding theproduct and processes involved. It is also expected that these modules would help the newentrants. | On account of the financial inclusion efforts made by Government of India, RBI and other stakeholders, there has been considerable progress in increasing the number of banking outlets and bank accounts. Financial Literacy is an important component to enable customers to use their accounts to their advantage and thereby enhance their financial well-being. Initially from a bank led model for propagating financial literacy in the country, over the years several steps have been taken to make financial literacy a multi-stakeholder community led approach to reach out to various groups of population who require financial literacy. Recommendation Since financial literacy and education are bedrocks of a vibrant financial system, it is important to make sustained efforts in this direction. It is recommended that the existing mechanism of SLBC/ DCC/ DLRC be leveraged and coordinated efforts are made by RBI, NABARD, NRLM resource persons, NGOs, PACS, Panchayats, SHGs, Farmers’ Clubs etc. to promote financial literacy at grassroots levels. Action Plan and Milestones: -

Develop financial literacy modules through National Centre for Financial Education (NCFE) that cover financial services in the form of Audio-Video content/ booklets etc. These modules should be with specific target audience orientation (e.g. children, young adults, women, new workers/ entrepreneurs, senior citizens etc.) by March 2021. -

Focus on process literacy along with concept literacy which empowers the customers to understand not only what the product is about, but also helps them how to use the product by using technology led Digital Kiosks, Mobile apps etc. through the strategy period (2019-2024). -

Expand the reach of Centers for Financial Literacy (CFL) at every block in the country by March 2024. IV.5 Customer Protection and Grievance Redressal Customers shall be made aware of the recourses available for resolution of their grievances. About storing and sharing of customer’s biometric and demographic data, adequate safeguards need to be ensured to protect the customer’s Right to Privacy. | With a large number of new customers included in the ambit of formal financial services, and with the emerging risks from digital financial services due to the incidents of cloning, hacking, phishing, vishing, SMiShing, pharming, malware etc. a strong customer protection architecture is vital. Data Protection and Information/Cyber Security are also the new frontiers that needs to be addressed under the customer protection framework. Recommendation Since financial system acts as a conduit in channelizing capital from the savers to the entrepreneurs who need it, and in turn meets the transactional and financial needs of the individuals, the importance of trust in the system remains paramount. Therefore, it is imperative to have a robust customer grievance redressal mechanism at different levels. It is recommended that internal audits should also assess the qualitative efficacy of the customer grievance redressal mechanism already in place in the banking system viz., Internal Ombudsman Scheme. Action plans and Milestones: -

Strengthening the Internal Grievances Redressal Mechanism of financial service providers for effectiveness and timely response by March 2020. -

Develop a robust customer grievance portal/ mobile app which acts as a common interface for lodging, tracking and redressal status of the grievances pertaining to financial sector collectively by all the stakeholders by March 2021. -

Operationalize a Common Toll-Free Helpline which offers response to the queries pertaining to customer grievances across banking, securities, insurance, and pension sectors by March 2022. -

Develop a portal to facilitate inter-regulatory co-ordination for redressal of customer grievance by March 2022. IV.6 Effective Co-ordination There needs to be a focused and continuous coordination between the key stakeholders viz. Government, the Regulators, financial service providers, Telecom Service Regulators, Skills Training institutes etc. to make sure that the customers are able to use the services in a sustained manner. The focus shall be to consolidate gains from previous efforts through focus on improvement of quality of service of last mile delivery viz., capacity building of Business Correspondents, creating payments system ecosystems at village levels to deepen the culture of digital finance leading to ease of use and delivery. | India has come a long way in the advancement of financial inclusion and the role of effective co-ordination cannot be over emphasised. Over the years, financial inclusion has moved from a bank led model to a multi-stakeholder led approach with the role of Telecom Service Providers and Fin-Tech companies emerging as important stakeholders in the pursuit of inclusive growth. Recommendation The sheer size and diversity of India makes it imperative for policymakers to follow a coordinated approach in meeting various objectives of financial inclusion. While fora like SLBC/ DCC/ BLBC are in place for coordination among various stakeholders, it is recommended that members of the same leverage such platforms to the maximum through assigning specific responsibilities to all. Further, promoting co-ordination through technology and adopting a decentralized approach to planning and development by creating separate smaller forums will help accelerate local level financial inclusion. Action Plans and Milestones: -

Clearly articulate the responsibilities/ expectations of each of the stakeholders at the grass-root level to ensure convergence of action between the Government/ Regulators/ financial service providers/ Civil Society etc. With the Lead Bank Scheme completing 50 years in 2019, SLBCs may review and implement the vision, action plans and the milestones to be achieved during the NSFI period (2019-24). -

With advancements in Geo-Spatial Information Technology, a robust monitoring framework leveraging on the said technology can be developed for monitoring progress under financial inclusion with special emphasis given to Aspirational Districts, North Eastern Region and Left -Wing Extremist affected Districts. A monitoring framework and a GIS dashboard to be developed by March 2022. V Recommendations This chapter is a broad summary of the previous chapter and lists down the key recommendations that are to be achieved under each of the strategic pillars for which the action plans have been outlined in the previous chapter. V.1 Universal Access to Financial Services -

The digital infrastructure in the country needs to be expanded through better networking of bank branches, BC outlets, Micro ATM, PoS terminals and stable connectivity etc. coupled with electricity. Efforts are needed to be undertaken through co-ordination with various stakeholders to ensure creation of the requisite infrastructure for moving towards completely digital on-boarding of customers. -

Encourage adoption and acceptance for digital payments and bringing people into the fold of formal financial system. In addition to the traditional banking outlets, efforts may also be taken to involve co-operative banks, Payments Banks, Small Finance Banks and other non-bank entities such as fertilizer shops, fair price shops, Office of the Local Government Bodies, Panchayat, Common Service Centres, educational institutions, etc., to promote efficiency and transparency through digital transactions. -

Some of the issues such as remuneration to the BCs, need for furnishing cash-based collaterals, cash management issues and lack of insurance for cash in transit which act as deterrents in smooth functioning of the BC network, need to be redressed by banks in a timely manner. V.2 Providing Basic Bouquet of Financial Services -

The banks may undertake periodic review of their existing products and adopt a customer centric approach while designing and developing financial products. -

Ensure efficient delivery by leveraging on Fin-tech and BC network. -

Initiate measures for capacity building of the BCs by encouraging and incentivizing them to acquire requisite certifications and enabling them to deliver a wide range of financial products. V.3 Access to Livelihood and Skill Development -

There should be convergence of objectives of the National Rural Livelihood and Urban Livelihood Missions to deepen Financial inclusion through an integrated approach. -

Inter-linkages may be developed between banks and other financial service providers with ongoing skill development, and livelihood generation programmes through RSETIs, NRLM, SRLM, Pradhan Mantri Kaushal Vikas Yojana etc. V.4 Financial Literacy and Education -

Customers need to be explained in simple language the nature of the product, its suitability to their requirements and the cost vis-à-vis return. -

Concerted efforts are needed to ensure coordination among the ground level functionaries viz. Lead District Manager (LDM), District Development Manager (DDM) of NABARD, Lead District Officer (LDO) of RBI, District and Local administration, Block level officials, NGOs, SHGs, BCs, Farmers’ Clubs, Panchayats, PACS, village level functionaries etc. while conducting financial literacy programmes. V.5 Customer Protection and Grievance Redressal -

A robust customer grievance redressal mechanism at different levels helps banks in timely redressal of grievances. -

Develop a portal to facilitate inter-regulatory co-ordination for redressal of customer grievance. V.6 Effective Co-ordination -

Strengthen the various fora under Lead Bank Scheme viz., SLBC / DCC / BLBC to ensure the achievement of the vision of the strategy at the ground level. -

Leverage on the emerging developments in technology to promote effective stakeholder co-ordination by having in place a digital dashboard/ MIS monitoring. -

Encourage decentralized approach to planning and development by creating a forum to actively involve Gram Panchayats/ Civil Society/ NGOs to accelerate financial inclusion using various tools like social audit. A review on the action taken on the recommendations may be conducted in March 2021 and accordingly, course corrections may be introduced. VI Measurement of Progress of Financial Inclusion VI.1 Periodic evaluation of financial inclusion policies through monitoring of financial inclusion parameters provides policy makers and stakeholders with necessary insights to understand the achievements made in the country and to address issues and challenges through a coordinated approach. The Financial Stability and Development Council (FSDC) is the Apex forum which also looks after Financial Inclusion and Literacy through the Technical Group on Financial Inclusion and Financial Literacy (TGFIFL) under the aegis of FSDC Sub-Committee (FSDC-SC). Financial Inclusion Advisory Committee (FIAC) undertakes review of the policies on financial inclusion amongst its other objectives. Further at the state level, the SLBC is the apex monitoring and coordinating forum to discuss issues pertaining to Financial Inclusion and Development. VI.2 As regards the design of the Financial Inclusion Indicators, there has been substantial research on various methodologies and tools to quantitatively monitor financial inclusion progress. The G20 Financial Inclusion Indicators serve as a useful guide and starting point for the design of country specific indicators and targets. Some of the key global data sources measuring financial inclusion across countries include Financial Access Survey of IMF, Global Findex Database by World bank and Enterprise Surveys. VI.3 In India, RBI collects data from banks on Financial Inclusion Plans, credit flow under priority sector, credit flow to minorities, and progress made under major Government Schemes. In addition to the above data collected by RBI, NABARD collects data from Rural Cooperatives and Regional Rural Banks. Other Financial Sector Regulators also capture necessary data pertaining to their regulated entities. Ministry of Finance, Government of India is also preparing an Index of Financial inclusion. VI.4 To make the whole data collection process meaningful and provide inputs for future policy interventions, the following approach may be considered for adoption: -

Data should be captured electronically, and directly from the systems that store these data sets through an Automated Data Extraction method. Such a collection of data would result in seamless processes, minimal human intervention and enhanced data integrity. -

The integration of data among all the financial sector regulators should be presented in the form of a Digital MIS Dashboard that can be analyzed granularly so as to understand the issues hampering financial inclusion progress at the grassroots level. These issues can be suitably taken up in the relevant forum for being addressed and progress may be monitored thereof. -

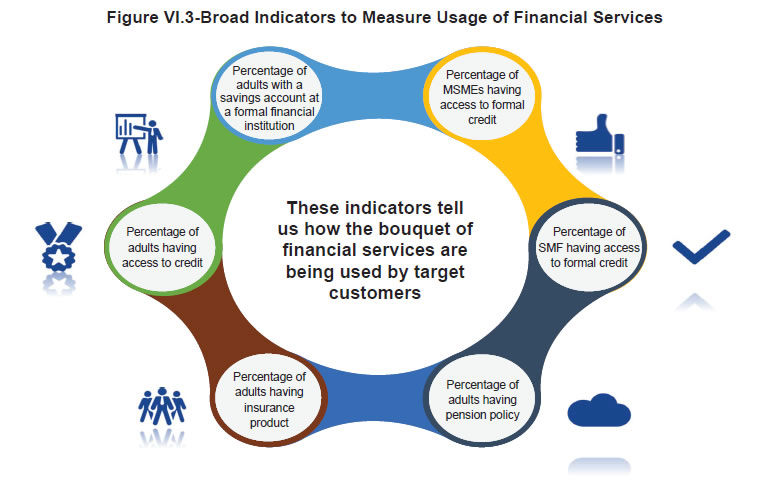

Going forward, the availability of consistent, reliable and internationally comparable gender disaggregated data is vital to focus attention on policies that could help close the gender gap on women’s access to formal financial services. Further, an understanding of the existence of regional variation and imbalances on women’s access to financial services across the country would also help in coming up with suitable policy interventions that can eventually help women achieve economic wellbeing through managing their household finances optimally. VI.5 Quantifying financial inclusion progress is usually undertaken across the three dimensions of access, usage and quality. VI.6 Access Indicators show the details pertaining to access points in the form of Banking Outlets (Bank Branches, Business Correspondent outlets), Automated Teller Machines (ATMs) and Point of Sale (PoS) terminals. The access parameters can be represented both in terms of geography (e.g number of banking outlets per 1000 sq km) as well as demography (e.g number of banking outlets per 100000 adult population). Typically, data for access indicator is obtained from the data available with the Government/ Regulators. VI.7 Usage Indicators show how the products are being used by the target customers. Data for usage can be collected through primary and secondary sources. While data on number of accounts, products, etc. can be collected from financial service providers, insights into the usage of different financial products and services may be obtained through surveys/ feedback from customers.  VI.8 The Quality indicators describe the supporting pillars that ensure that the customers can use the financial services to their satisfaction. For example, financial literacy and capability is an important enabler to help customers make right choices. However, lack of proper service by the provider may result in dissatisfaction to the customer which may result in financial exclusion. Since quality also involves the dimension of subjectivity, it is essential to have a well-defined metric that allows for certain flexibility while capturing data. Measuring quality under financial inclusion can include financial literacy and capability, clarity and transparency in the communication of the service provider, customer satisfaction, availability of grievance redressal process and timely redressal mechanisms. VI.9 An illustration of Financial Inclusion Indicators is presented below: | Sl No | Category | Indicator | Formula | | Access | | 1 | Physical points of service | No. of banking outlets per 100,000 adults | Total No. of banking outlets

–––––––––––––––––––––––– X 100000

Total adult population | | 2 | No. of ATMs per 100,000 adults | Total No. of ATMs

–––––––––––––––––––– X 100000

Total adult population | | 3 | No. of Depository Participant Service Centres Across the Country per 100,000 adults | Total No. of Depository Participant Service Centres

––––––––––––––––––––––––––––––––––––––––––––– X 100000

Total adult population | | 4 | No. of Mutual Fund Distributors’ per 100,000 adults | Total No. of Mutual Fund Distributors

––––––––––––––––––––––––––––––––– X 100000

Total adult population | | Usage | | 5 | Formally banked adults | Percentage of adults with a savings bank account | Total No. of adults with savings bank account

––––––––––––––––––––––––––––––––––––––– X 100

Total adult population | | 6 | Formally banked women | Percentage of women having a savings bank account | Total No. of Women with a saving bank account

–––––––––––––––––––––––––––––––––––––––––– X 100

Total Women population | | 7 | Formally banked MSMEs | Percentage of MSMEs having access to bank credit | MSMEs with access to bank credit

–––––––––––––––––––––––––––––––– X 100

Total Number of MSMEs | | 8 | Formally banked Agricultural Sector | Percentage of SMF having access to bank credit | Total Number of SMF with access to bank credit

––––––––––––––––––––––––––––––––––––––––– X 100

Total Number of SMFs | | 9 | Adults with pension | Percentage of adults having pension policy (includes NPS and APY) | Total No. of adults with pension accounts

–––––––––––––––––––––––––––––––––––– X 100

Total adult population | | 10 | Adults with life insurance | Percentage of adults having life insurance product | Total No. of adults with life insurance

––––––––––––––––––––––––––––––––– X 100

Total adult population | | 11 | Adults with non- life insurance | Percentage of adults having non- life insurance product | Total No. of adults with non- life insurance

–––––––––––––––––––––––––––––––––––– X 100

Total adult population | | 12 | Adults with Credit Product | Percentage of Adults having credit product from banks | No. of adults with credit product from banks

–––––––––––––––––––––––––––––––––––– X 100

Total adult population | | 13 | Adults with Mutual Fund Products (Folios) | Percentage of Adults having Mutual Fund Products (Folios) | No. of adults with Mutual fund Products (Folios)

––––––––––––––––––––––––––––––––––––––––– X 100

Total adult population | | 14 | Adults with Demat Accounts | Percentage of Adults with Demat Accounts | No. of adults with Demat Accounts

–––––––––––––––––––––––––––––– X 100

Total adult population | | 15 | Women with pension | Percentage of Women having pension product (includes APY/ NPS) | Total No. of women with pension accounts

––––––––––––––––––––––––––––––––––––– X 100

Total women population | | 16 | Women with life insurance | Percentage of women having life insurance product | Total No. of women with life insurance product

–––––––––––––––––––––––––––––––––––––––– X 100

Total women population | | 17 | Women with non- life insurance | Percentage of women having non-life insurance product | Total No. of women with non-life insurance product

–––––––––––––––––––––––––––––––––––––––––––––– X 100

Total women population | | 18 | Women with credit Product | Percentage of women with a formal credit product | Total No. of women with formal credit product

––––––––––––––––––––––––––––––––––––––––––– X 100

Total women population | | 19 | Women with Mutual Fund Products (Folios) | Percentage of women having Mutual Fund Products (Folios) | No. of women with Mutual fund Products (Folios)

–––––––––––––––––––––––––––––––––––––––– X 100

Total women population | | 20 | Women with Demat Accounts | Percentage of women with Demat Accounts | No. of women with Demat Accounts

––––––––––––––––––––––––––––––– X 100

Total women population | | Quality | | 21 | Financial Literacy & Capability | Financial Knowledge Score Arithmetic score which sums up correct responses to questions about basic financial concepts such as: (a) inflation; (b) Interest Rate; (c) Compound Interest; (d) Money illusion; (e) Risk Diversification; (f) Main Purpose of insurance. | Through conduct of Periodic Dipstick Surveys | | 22 | Grievance Redressal | Existence of formal internal and external dispute resolution mechanism, measured through:

i) No. of complaints received

ii) No. of complaints resolved

iii) Category of Complaints

iv) Average Time taken to resolve Complaints | Through data from Banking Ombudsman scheme and banks | Conduct of Studies/ Surveys VI.10 In addition to data collected from financial service providers, there is also a need to seek views and insights from the end users of the products themselves, namely the customers. There are a lot of demand side surveys including the Global Findex Demand Side Data and Enterprise Survey of the World Bank, the Fin-Scope, the Inclusix of CRISIL etc. While these may serve as broad indicators and tool kits for understanding the macro level progress under financial inclusion, it is also essential to design surveys based on region specific issues to critically understand the issues and problems pertaining to regional disparity, demand peculiarities resulting in inequality and exclusion. VI.11 To begin with, a base line survey can be undertaken to assess the issues that hamper progress under financial inclusion efforts of the stakeholders. The issues that are recommended to be covered may inter alia include the following aspects: -

Challenges faced in accessing financial services while opening an account, seeking credit, or opening of other financial inclusion products like Micro Insurance, Pension, Investments and Remittances -

Issues faced while using digital financial services -

Attitude of financial service provider -

Complete knowledge of the product features including terms and conditions -

Knowledge of Customer Rights -

Grievance Redressal Mechanisms -

Satisfaction in using the products VII Conclusion VII.1 The document highlights the major issues that act as impediments to financial inclusion and comes up with a set of recommendations and action plans to support sustainable financial inclusion over the next 5 years. VII.2 Substantial efforts are needed not only from banks and other financial institutions, but also from an array of other stakeholders including civil society. As a result, the document views universal access to financial services and providing bouquet of basic financial services as the starting point of the strategy. Over the next few years, it is envisaged that ubiquitous physical and digital connectivity coupled with full financial inclusion is possible owing to the focused efforts being undertaken by the respective stakeholders. The issues like customer centric approach for product design and delivery, focus on financial literacy and strengthening the customer protection framework as described in the relevant chapters need adequate focus to ensure that the momentum generated by the Government’s PMJDY needs to be taken forward to ensure better delivery and choices available to the end customers with active involvement from the service providers including private sector players. VII.3 A discussion on financial inclusion policies would be incomplete if digital financial inclusion and the role of fin-tech is not meaningfully integrated in the policy discourse. While, India has largely benefited from the Jan Dhan-Aadhaar- Mobile trinity over the last few years, adequate measures are needed to strengthen the digital financial services’ eco-system including increased awareness on usage of digital modes of transactions, increased access points/ acceptance infrastructure and a safe environment incorporating the principles of consent and privacy. It is expected that over the next few years, fin-tech may evolve from its present structure, calling for adequate understanding among regulators, financial service providers and most importantly the customers availing financial services through the digital mode. It is, therefore, important to first address the newly digitally included customers through adequate awareness and literacy. VII.4 The need for an objective and a scientific assessment of the progress made in financial inclusion cannot be overlooked. While a lot of data collection efforts are underway, there is a need to go beyond data collected from financial service providers alone. Surveys and feedback from the customers, leveraging on Big Data sets and importantly collecting and analyzing granular data to gather a holistic perspective on the coverage and also the usage of financial services is essential. Insights on the quality of financial services delivered to various target groups would be very useful to see the impact of financial inclusion policies on overall financial wellbeing.

Bibliography 1. About PFRDA. (2018, October 09). Retrieved from Pension Fund Regulatory and Development Authority Website: http://www.pfrda.org.in/ 2. DFS, M. o. (2018, October 09). Continuation of PMJDY beyond 14 August 2018. Retrieved from PMJDY: https://www.pmjdy.gov.in/files/E-Documents/Continuation_of_PMJDY.pdf 3. DFS, Ministry of Finance. (2018, October 09). PMJJBY. Retrieved from Department of Financial SErvices, Ministry of Finance, GoI: https://financialservices.gov.in/insurance-divisions/Government-Sponsored-Socially-Oriented-Insurance-Schemes/Pradhan-Mantri-Jeevan-Jyoti-Bima-Yojana(PMJJBY) 4. DFS, Ministry of Finance. (2018, October 09). PMSBY. Retrieved from Department of Financial Services, Ministry of Finance, Government of India: https://financialservices.gov.in/insurance-divisions/Government-Sponsored-Socially-Oriented-Insurance-Schemes/Pradhan-Mantri-Suraksha-Bima-Yojana(PMSBY) 5. DFS, Ministry of Finance, GoI. (2014, August). Mission Document- PMJDY. Retrieved from PMJDY: https://www.pmjdy.gov.in/files/E-Documents/PMJDY_BROCHURE_ENG.pdf 6. Giridhar, G., James, K., Kumar, S., Sivaraju, S., Alam, M., Gangadharan, K.,... Gupta, N. (2017). Caring for Our Elders: india Ageing Report 2017. New Delhi, India: United Nations Population Fund. Retrieved October 09, 2018, from https://india.unfpa.org/sites/default/files/pub-pdf/India%20Ageing%20Report%20-%202017%20%28Final%20Version%29.pdf 7. Home-Sustainable Development Goals. (2018, August 09). Retrieved from UNDP: http://www.undp.org/content/undp/en/home/sustainable-development-goals.html 8. RBI. (2015, December 28). Report of the Committee on Medium Term Path on Financial Inclusion. Retrieved from https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/FFIRA27F4530706A41A0BC394D01CB4892CC.PDF 9. RBI. (2018, October 09). Chapter IV-Credit Delivery and Financial Inclusion; Annual Report of RBI 2017-18. Retrieved from RBI: https://www.rbi.org.in/scripts/AnnualReportPublications.aspx?Id=1231 10. SIDBI. (2018, October 09). Certified Credit Counsellors. Retrieved from SIDBI Udyami Mitra: https://udyamimitra.in/Home/CCC 11. Social Protection Advisory Service, World Bank. (2018, October 09). world Bank Pension Reform Primer- The World Bank Pension Conceptual Framework. Retrieved from worldbank. org: http://siteresources.worldbank.org/INTPENSIONS/Resources/395443-1121194657824/PRPNoteConcept_Sept2008.pdf 12. Universal Financial Access 2020. (2018, October 09). Retrieved from World Bank Website: http://www.worldbank.org/en/topic/financialinclusion/brief/achieving-universal-financial-access-by-2020 13. Welfare, M. o. (2018, October 09). Institutional credit to small farmers- Press Information Bureau. Retrieved from Press Information Bureau: http://pib.nic.in/newsite/PrintRelease.aspx?relid=175181 14. World Bank Group. (2018). Developing and Operationalizing a National Financial Inclusion Strategy. Washington DC: World Bank Group.

List of Select Abbreviations | APBS | Aadhaar Payment Bridge System | | AEPS | Aadhaar Enabled Payment System | | AFI | Alliance for Financial Inclusion | | ANBC | Adjusted Net Bank Credit | | ATM | Automated Teller Machine | | APY | Atal Pension Yojana | | BC | Business Correspondent | | BLBC | Block Level Bankers Committee | | BSBDA | Basic Savings Bank Deposit Account | | CBSE | Central Board of Secondary Education | | CBK | Central Bank of Kenya | | CCC | Certified Credit Counsellors | | CDD | Customer Due Diligence | | CFL | Centre for Financial Literacy | | CGAP | Consultative Group to Assist the Poor | | CKYC Registry | Central Know Your Customer Registry | | CMPFI | Committee on Medium Term Path on Financial Inclusion | | CONAIF | National Council for Financial Inclusion | | CSC | Common Service Centre | | CTS | Cheque Truncation System | | DAY | Deendayal Antyodaya Yojana | | DAY-NULM | Deendayal Antyodaya Yojana- National Urban Livelihood Mission | | DBT | Direct Benefit Transfer | | DCC | District Consultative Committee | | DCCB | District Central Co-operative Bank | | DDU-GKY | Pt. Deen Dayal Upadhyaya Grameen Kaushalya Yojana | | DFS | Department of Financial Services | | DLRC | District Level Review Committee | | FAME | Financial Awareness Message | | FLC | Financial Literacy Centre | | FIAC | Financial Inclusion Advisory Committee | | FIF | Financial Inclusion Fund | | FIP | Financial Inclusion Plan | | FSDC | Financial Stability and Development Council | | GCC | General Credit Card | | GPFI | Global Partnership for Financial Inclusion | | G2P | Government to Person | | IBA | Indian Banks’ Association | | IFI | Index of Financial Inclusion | | IIBF | Indian Institute of Banking and Finance | | IMF | International Monetary Fund / Insurance Marketing Firms | | IMPS | Immediate Payment Service | | INFE | International Network for Financial Education | | IPPB | India Post Payments Bank | | ISP | Insurance Service Provider | | IR | Insurance Repository | | IGNOAPS | Indira Gandhi National Old Age Pension Scheme | | ICT | Information and Communication Technology | | IRDAI | Insurance Regulatory and Development Authority of India | | JAM | Jan Dhan- Aadhaar-Mobile | | KYC | Know Your Customer | | LDO | Lead District Officer | | LWE | Left Wing Extremists | | MIS | Management Information System | | MGNREGA | Mahatma Gandhi National Rural Employment Guarantee Act | | MoF | Ministry of Finance | | MSME | Micro, Small and Medium Enterprises | | NACH | National Automated Clearing House | | NAMCABS | National Mission for Capacity Building of Bankers for Financing MSME Sector | | NABARD | National Bank for Agriculture and Rural Development | | NEFT | National Electronic Fund Transfer | | NER | North Eastern Region | | NCFE | National Centre for Financial Education | | NFIS | National Financial Inclusion Strategy | | NPCI | National Payments Corporation of India | | NGO | Non-Government Organisation | | NPS | National Pension System | | NRLM | National Rural Livelihoods Mission | | NSFI | National Strategy for Financial Inclusion | | NULM | National Urban Livelihoods Mission | | NWR | Negotiable Warehouse Receipts | | OECD | Organisation for Economic Co-operation and Development | | PACS | Primary Agricultural Co-operative Society | | P2B | Person to Business | | P2P | Person to Person/ Peer to Peer | | P2G | Person to Government | | PCR | Public Credit Registry | | PMEGP | Pradhan Mantri Employment Guarantee Programme | | PMKVY | Pradhan Mantri Kaushal Vikas Yojana | | PMJDY | Pradhan Mantri Jan Dhan Yojana | | PPF | Public Provident Fund | | PB | Payments Bank | | PMJJBY | Pradhan Mantri Jeevan Jyoti Bima Yojana | | PMMY | Pradhan Mantri Mudra Yojana | | PMSBY | Pradhan Mantri Suraksha Bima Yojana | | PFRDA | Pension Fund Regulatory and Development Authority | | PSGIC | Public Sector General Insurance Companies | | RoC | Registrar of Companies | | RTGS | Real Time Gross Settlement | | RXIL | Receivables Exchange of India | | RBI | Reserve Bank of India | | SC | Scheduled Caste | | ST | Scheduled Tribe | | SEBI | Securities and Exchange Board of India | | SFB | Small Finance Banks | | SIDBI | Small Industries Development Bank of India | | SLBC | State Level Bankers’ Committee | | SME | Small and Medium Enterprises | | SPV | Special Purpose Vehicle | | SRLM | State Rural Livelihoods Mission | | TGFIFL | Technical Group on Financial Inclusion and Financial Literacy | | TReDS | Trade Receivables Discounting System | | UFA | Universal Financial Access | | UIDAI | Unique Identification Authority of India | | UNSDG | United Nations Sustainable Development Goals | | UPI | Unified Payments Interface | | USSD | Unstructured Supplementary Service Data | | WDRA | Warehousing Development and Regulatory Authority |

|