[Under Section 45ZL of the Reserve Bank of India Act, 1934] The thirty seventh meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held during August 3 to 5, 2022. 2. The meeting was attended by all the members – Dr. Shashanka Bhide, Honorary Senior Advisor, National Council of Applied Economic Research, Delhi; Dr. Ashima Goyal, Emeritus Professor, Indira Gandhi Institute of Development Research, Mumbai; Prof. Jayanth R. Varma, Professor, Indian Institute of Management, Ahmedabad; Dr. Rajiv Ranjan, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Michael Debabrata Patra, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely: -

the resolution adopted at the meeting of the Monetary Policy Committee; -

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and -

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting. 4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail the staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 5, 2022) decided to: - Increase the policy repo rate under the liquidity adjustment facility (LAF) by 50 basis points to 5.40 per cent with immediate effect.

Consequently, the standing deposit facility (SDF) rate stands adjusted to 5.15 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 5.65 per cent. - The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 6. Since the MPC’s meeting in June 2022, the global economic and financial environment has deteriorated with the combined impact of monetary policy tightening across the world and the persisting war in Europe heightening risks of recession. Gripped by risk aversion, global financial markets have experienced surges of volatility and large sell-offs. The US dollar index soared to a two-decade high in July. Both advanced economies (AEs) and emerging market economies (EMEs) witnessed weakening of their currencies against the US dollar. EMEs are experiencing capital outflows and reserve losses which are exacerbating risks to their growth and financial stability. Domestic Economy 7. Domestic economic activity remains resilient. As on August 4, 2022, the south-west monsoon rainfall was 6 per cent above the long period average (LPA). Kharif sowing is picking up. High frequency indicators of activity in the industrial and services sectors are holding up. Urban demand is strengthening while rural demand is gradually catching up. Merchandise exports recorded a growth of 24.5 per cent during April-June 2022, with some moderation in July. Non-oil non-gold imports were robust, indicating strengthening domestic demand. 8. CPI inflation eased to 7.0 per cent (year-on-year, y-o-y) during May-June 2022 from 7.8 per cent in April, although it persists above the upper tolerance band. Food inflation has registered some moderation, especially with the softening of edible oil prices, and deepening deflation in pulses and eggs. Fuel inflation moved back to double digits in June primarily due to the rise in LPG and kerosene prices. While core inflation (i.e., CPI excluding food and fuel) moderated in May-June due to the full direct impact of the cut in excise duties on petrol and diesel pump prices, effected on May 22, 2022, it remains at elevated levels. 9. Overall system liquidity continues in surplus, with average daily absorption under the LAF at ₹3.8 lakh crore during June-July. Money supply (M3) and bank credit from commercial banks rose (y-o-y) by 7.9 per cent and 14.0 per cent, respectively, as on July 15, 2022. India’s foreign exchange reserves were placed at US$ 573.9 billion as on July 29, 2022. Outlook 10. Spillovers from geopolitical shocks are imparting considerable uncertainty to the inflation trajectory. More recently, food and metal prices have come off their peaks. International crude oil prices have eased in recent weeks but remain elevated and volatile on supply concerns even as the global demand outlook is weakening. The appreciation of the US dollar can feed into imported inflation pressures. Rising kharif sowing augurs well for the domestic food price outlook. The shortfall in paddy sowing, however, needs to be watched closely, although stocks of rice are well above the buffer norms. Firms polled in the Reserve Bank’s enterprise surveys expect input cost pressures to soften across sectors in H2. Cost pressures are, however, expected to get increasingly transmitted to output prices across manufacturing and services sectors. Taking into account these factors and on the assumption of a normal monsoon in 2022 and average crude oil price (Indian basket) of US$ 105 per barrel, the inflation projection is retained at 6.7 per cent in 2022-23, with Q2 at 7.1 per cent; Q3 at 6.4 per cent; and Q4 at 5.8 per cent, and risks evenly balanced. CPI inflation for Q1:2023-24 is projected at 5.0 per cent (Chart 1). 11. On the outlook for growth, rural consumption is expected to benefit from the brightening agricultural prospects. The demand for contact-intensive services and the improvement in business and consumer sentiment should bolster discretionary spending and urban consumption. Investment activity is expected to get support from the government’s capex push, improving bank credit and rising capacity utilisation. Firms polled in the Reserve Bank’s industrial outlook survey expect sequential expansion in production volumes and new orders in Q2:2022-23, which is likely to sustain through Q4. On the other hand, elevated risks emanating from protracted geopolitical tensions, the upsurge in global financial market volatility and tightening global financial conditions continue to weigh heavily on the outlook. Taking all these factors into consideration, the real GDP growth projection for 2022-23 is retained at 7.2 per cent, with Q1 at 16.2 per cent; Q2 at 6.2 per cent; Q3 at 4.1 per cent; and Q4 at 4.0 per cent, and risks broadly balanced. Real GDP growth for Q1:2023-24 is projected at 6.7 per cent (Chart 2).

12. Headline inflation has recently flattened and the supply outlook is improving, helped by some easing of global supply constraints. The MPC, however, noted that inflation is projected to remain above the upper tolerance level of 6 per cent through the first three quarters of 2022-23, entailing the risk of destabilising inflation expectations and triggering second round effects. Given the elevated level of inflation and resilience in domestic economic activity, the MPC took the view that further calibrated monetary policy action is needed to contain inflationary pressures, pull back headline inflation within the tolerance band closer to the target, and keep inflation expectations anchored so as to ensure that growth is sustained. Accordingly, the MPC decided to increase the policy repo rate by 50 basis points to 5.40 per cent. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. 13. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to increase the policy repo rate by 50 basis points to 5.40 per cent. 14. All members - Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma - voted to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Prof. Jayanth R. Varma expressed reservations on this part of the resolution. 15. The minutes of the MPC’s meeting will be published on August 19, 2022. 16. The next meeting of the MPC is scheduled during September 28-30, 2022. Voting on the Resolution to increase the policy repo rate to 5.40 per cent | Member | Vote | | Dr. Shashanka Bhide | Yes | | Dr. Ashima Goyal | Yes | | Prof. Jayanth R. Varma | Yes | | Dr. Rajiv Ranjan | Yes | | Dr. Michael Debabrata Patra | Yes | | Shri Shaktikanta Das | Yes | Statement by Dr. Shashanka Bhide 17. The sharp increase in inflation rate in March 2022, following two successive months of CPI inflation rate of 6 per cent or above, changed the policy perspectives on inflation. The developments in March caused by the Russia-Ukraine war imparted much uncertainty to global supplies of fuel, food and trade in general. The rise in global energy prices had clear impact on the domestic prices. In May policy rate was increased by MPC, which was followed up in June. Although the risks of Covid 19 pandemic remained, there were signs of strengthening economic activities as both supply and demand conditions improved in many of the sectors. Bringing inflation rate closer to the target was important to sustain the economic growth momentum over the medium term. 18. The headline consumer inflation rate for Q1: FY 2022-23 is at 7.3 per cent, although lower than the level projected in the June MPC meeting. At 7.3 per cent, it is also higher than any of the previous four quarters of 2021-22. The moderation seen in the headline inflation rate in May and June, from 7.8 per cent in April to 7.0 per cent was mainly on account of the decline in food inflation and inflation in the category of items excluding food and fuel & light. But in each of the three major components of the headline, the year-on-year (YOY) inflation rate remained at or above 6 per cent in June, highlighting the continued broad-based inflationary pressures. 19. Reduction in the excise duty on petrol and diesel by the central government and some of state governments towards the end of May helped ease price pressures for the transport sector. Withdrawal of Indonesia’s ban on palm oil exports by the end of May 2022 helped ease price pressures on food inflation. 20. The commodity prices in the international markets, including metals and crude oil, softened from the highs that prevailed when the Russia-Ukraine war broke out. The softening of the international crude oil prices appears to be a consequence of expected slowing down of global growth as monetary policies across countries tightened to rein in inflationary pressures. Slowing down of Chinese economy has also been a factor in the emerging global weak demand conditions as Covid 19 continues to cast a shadow on economic activities there. 21. These have been the positive developments as far as inflation scenario is concerned. However, uncertainty on inflation pressures in the global environment remains significant. Prolonged Russia-Ukraine conflict and disruptions in supplies, especially for energy and food commodities are a major source of uncertainty for price trends. The direct impact of supply disruptions, even if targeted to some geographies, is quickly transmitted elsewhere to meet the overall demand supply imbalances. Weakening of many currencies against the US dollar also imparts inflationary pressures on the domestic economies of the other countries. 22. On the domestic front, inflationary pressures exerted by the rising input prices are continuing. The impact of recent changes to GST rates, somewhat uneven distribution of the southwest monsoon rainfall with deficiency in the eastern region of the country, could be source of upward pressure on prices. The Enterprise Surveys conducted by the RBI in May-June 2022 find that majority of the firms in all the major sectors of the economy, manufacturing, services and infrastructure, expect the cost pressures to continue through the current financial year. As a consequence, product prices are also expected to increase. The bimonthly survey of consumers conducted in the first fortnight of July also points to the widely shared perception of the prevailing high rate of inflation one-year ahead, although the percentage of respondents who expect the rate to decline has increased compared to the previous survey in May 2022. The RBI Survey of Inflation Expectations of Households also conducted in the first fortnight of July shows that the 3 months ahead and one year ahead median expected inflation rates have declined from the expectations held in May. However, by a qualitative measure, the percentage of respondents expecting a decline in inflation rate 3 months ahead or one year ahead is far below the percentages who expect the rate to increase or stay similar. These sample survey results show some signs of expectations of decline in future inflation rates but the optimism is guarded. The RBI Survey of Professional Forecasters conducted in the second fortnight of July 2022 projects a CPI inflation rate of 6 per cent or above in the remaining three quarters of FY 2022-23. 23. The present pattern of trends and assessments suggest a gradual decline in inflation rate during FY 2022-23 but still above the upper level of the tolerance band around the target of 4 per cent. Going forward, the food inflation scenario would be affected by the overall rainfall conditions in the remaining period of the present monsoon and the crop prospects, besides the global price conditions. The easing of global prices in the case of energy and other raw materials may soften the prices in the non-food sectors although there may still be pressures from the incomplete pass through of the higher input prices that prevailed. The upside risks to any declining inflation trajectory in the short term are significant. Taking into account these trends, for FY 2022-23, the headline CPI inflation rates have been projected at 7.1 per cent for Q2, 6.4 per cent for Q3 and 5.8 per cent in Q4. The projected inflation rate for FY 2022-23 is at 6.7 per cent, the same as in the June MPC meeting. 24. The global economic conditions have turned unfavourable for growth from the combined shocks of the breakout of the Russia-Ukraine war, continued shadow of Covid 19 across countries and the tightening of monetary policies to rein in inflation in many countries. The revised projections by the International Monetary Fund for 2022, released in July, place world GDP growth at 3.2 per cent, sharp drop from 4.4 per cent projected in January 2022 and 3.6 per cent in April 2022. The world trade volume of goods and services is now projected to grow by 4.1 per cent in 2022 over the previous year, a decline from 6 per cent projected in January and 5 per cent in April 2022. Deceleration in growth, particularly in the major economies of the world would have an adverse impact on their imports. The spill over effects on imports of other countries are also adverse. The monetary policy tightening in the advanced economies has also led to capital outflow from the emerging economies, including India. The elevated levels of crude oil prices and the rising prices of natural gas in the international markets has meant rising import costs raising trade deficit. 25. The worsening global economic conditions have come at a time for us when the domestic economy was beginning to sustain its growth momentum after regaining the output level in 2021-22 from the shocks of the Covid 19 pandemic. Performance of a number of sectors showed sustained growth in Q1: FY 2022-23, particularly in manufacturing. Although IIP for April-May 2022 was only 4.0 per cent above the same period in 2019, it was 12.9 per cent YOY basis. The PMI for manufacturing has remained in the expansion zone for April-June and rose further in July. In the case of services also, PMI rose from April to June but fell in July. Capacity utilisation in manufacturing rose above the long-term average in Q4: 2021-22 and the RBI Industrial Outlook Survey reflects expectations of steady improvement through Q4: 2022-23. Although there are concerns over demand conditions in the case of services and infrastructure sectors in H1, improvement in conditions is expected in H2: FY 2022-23. 26. On the demand side, the RBI Survey of Consumer Confidence conducted in the first fortnight of July reflects continued caution by the consumers on non-essential spending. One year ahead from now, only about 30 per cent of the respondents expect to increase non-essential spending. The import of capital goods during January-June 2022 in terms of value in US$ are above the 2019, although IIP for capital goods is still below 2019 level for the same period. Export performance in both goods and services in 2021-22 was well above the 2019 levels and in Q1: FY 2022-23, exports exceeded the value, YOY basis as well. However, going forward, export performance would be affected by the global demand conditions, with strengthening dollar providing some incentive to exporters despite the higher cost of imported inputs. 27. The recent data on indicators such as GST collections, E-way bills and non-food credit indicate sustained momentum of economic activities. Although demand conditions may be restrained, the growth momentum has been sustained. Based on the overall economic activity conditions, the YOY GDP growth rate of 7.2 per cent for FY 2022-23 projected in the June 2022 MPC meeting has been retained. 28. The CPI inflation rate is in excess of 6 per cent in Q4: FY 2021-22 and Q1: FY 2022-23 and projected to be well above the target of 4 per cent in Q1: FY 2023-24. Both the GDP growth rate and inflation rate for FY 2022-23 have been retained at the same levels as in the June MPC meeting. There are significant uncertainties to both growth and inflation rates emanating from external and domestic factors. Sustaining the growth momentum will also require reduction in inflation rate. The prevailing inflation pressures, therefore, remain a concern and continued monetary policy measures are needed to ensure that the inflation rate is aligned with the target rate. 29. Accordingly, I vote to increase the policy repo rate by 50 basis points to 5.4 per cent. I also vote to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Statement by Dr. Ashima Goyal 30. The last three months show Indian growth sustaining despite continuing global shocks and rate rises. Indeed, India has done better than expected and in comparison to many countries under the pandemic and Ukraine war shocks. Among reasons for this are growing economic diversity that helps to absorb shocks. Large domestic demand can moderate a global slowdown; if industry suffers from lockdown, agriculture does well. Services compensate for less contact-based delivery with digitization, distance work and exports. Even if global growth slows, diversification from China, India’s digital advantage and government efforts to promote exports would support Indian exports. A rise in the current very small Indian share in world exports remains feasible. Another example of the value of diverse participants comes from the financial markets. Household SIPs in stock markets have compensated for FPI outflow. Since the share of stocks in their financial assets is still low (4 per cent compared to 27 per cent for US households) there is room for this to rise further safely and give households higher returns in a better diversified portfolio. Other types of diversity in the financial sector are improving stability. 31. The repo rate rise, which is reversing the large pandemic-induced cut of 115 bps in a more calibrated fashion, has not as yet slowed the recovery. Real rates remain negative and there are lags in pass through. Even so, rising rates may have prevented over-heating. Coordinated fiscal and monetary policy action to reduce inflation while maintaining adequate demand has worked well. 32. Inflation has also moderated. FPI are returning because India has better prospects among emerging markets, and the crash in currency and stock markets that they were waiting for in order to re-enter is proving unlikely. Commodity inflation is finally softening, and is likely to continue with a global slowdown and supply-chain bottlenecks turning into gluts due to excess inventories with firms. In India there is some rise in industry wages, but corporate margins remain high. Large sales and softening of other input costs gives space to absorb moderate wage rise. Although the RBI enterprise survey shows corporates expect prices to rise, if demand falls it may moderate their ability to raise prices. Rural wage growth is flat at 4.8 per cent. Household inflation perceptions and expectations have fallen. 33. Inflation, however, is still above the tolerance band, and shows signs of being so for the first 3 quarters of 2022-23. This can be destabilizing for inflation expectations. That policy responds strongly to ensure its inflation commitments is important for the credibility of an inflation targeting regime. Some rise in GST tax rates, electricity tariffs, energy costs and rupee depreciation, although the rupee is showing signs of mean reversion towards real equilibrium values, are short-term risks for inflation. 34. Attempting a soft landing for the economy is important, however. For this, policy rates should not depart far from equilibrium. Such an outcome also balances between those who gain from a rise in rates and those who lose from it. In my last minutes I had suggested (-)1 per cent as the then lower limit for the one year ahead real repo rate. Shocks affect the steady-state natural interest rate1. Policy has to tighten against negative supply shocks as well as against positive demand shocks that raise the equilibrium rate. My research showed Indian real rates were required to be negative in slumps but low positive in booms2. The healthy recovery suggests we are no longer in a slump. Crude oil prices have fallen, but their persistence above $100, is a negative supply shock, raising the required one-year ahead real rate into positive territory. One year ahead inflation is expected to be around 5 per cent. Therefore, I vote for a 50 bps rise raising the repo rate to 5.4 per cent, and delivering the required low positive real rate. 35. Since the real rate is now near neutral, but uncertainty and global risks to both growth and inflation remain high, policy has to carefully monitor incoming data and respond to current developments. Indeed, if the US Fed does that, tapering its rate rise with signs of a slowdown, it will reduce global risks. 36. One of the first impacts of rising policy repo rates should be on credit demand as pass through raises loan rates. India is just coming out of a deleveraging cycle and recovery requires credit growth to rise. Despite rising repo rates in May and June 2022, yearly credit growth over the respective months in 2021 continues to be high partly due to the base effect. Preliminary sectoral credit data shows sharp rise in bank loans to the service sector but average of MSME, NBFC and personal bank loans over May and June was less than in April, and loans to large industry fell in June. There are pitfalls in monthly comparisons and the picture will be clearer as more data comes in. The rise in loan rates is still limited but has begun. 37. I also vote for ‘withdrawal of accommodation’ to continue since such a stance defined in terms of liquidity also indicates that durable liquidity will continue to be in surplus. This reassurance is important in a period of risk-off and possible outflows as the Fed continues its quantitative tightening. The LAF system has enough instruments to sterilize any effect on domestic liquidity. 38. India’s flexible inflation targeting framework is mandated to respond only to inflation and growth. The repo rate does not respond to the exchange rate. This is market determined with India’s capital flow and reserve management effectively reducing exchange rate volatility, which can be too high in emerging markets under global shocks. Research shows that inflation targeting works better in developing economies if additional instruments are available to address excess exchange rate and capital flow volatility3. India has many such instruments that can be activated if necessary. 39. Moreover, the interest differential with the US has only a minor and possibly perverse effect on capital flows. Debt liabilities in India’s net international investment position include fixed income flows, as well as ECBs and institutional cross border borrowing. Of these $14bn left in 2020, and after that, even as the differential narrowed, have been steady at $100bn. A rise in Indian interest rates will not induce equity investment, which is the one that is currently volatile, to stay. In 2013 and in 2018 following the Fed rate rise aggravated the Indian slowdown. Today policy has more degrees of freedom to use. Similarly, multiple instruments are required and are available to keep the current account deficit at sustainable levels. A competitive equilibrium REER and demand-reducing positive real interest rates will also help. Statement by Prof. Jayanth R. Varma 40. Inflation is at unacceptably high levels, and the projected trajectory is also above target during the entire forecast horizon. Economic growth has on the other hand proved resilient in the face of an adverse global environment. In this situation, there is clearly a need for front loaded hikes in the policy rate. The choice to my mind is between 50, 60 and 75 basis points. 41. The logic of front loading argues in favour of a 75 basis point hike: it would establish the credibility of monetary policy beyond doubt, would help achieve a faster reduction in the inflation rate, and would hopefully reduce the terminal repo rate consistent with bringing inflation close to the target. Weighing against that is the fact that a 75 basis point rate hike is quite unusual (despite a few recent hikes of this magnitude globally in the recent period). In the context of market expectations of a 35-50 basis point hike, such a large hike risks being misinterpreted as a sign of panic, and could be unnecessarily disruptive. Also even with a 50 basis point hike this month, the cumulative tightening in the past few months of 140 basis points would make the real interest rate positive based on projected inflation 3-4 quarters ahead. On balance, therefore, I do not favour a 75 basis point hike at this juncture. 42. The choice between 50 and 60 basis points is less clear cut. The latter has the advantage of bringing the repo rate back to a round multiple of a quarter percent, but shares some of the disadvantage of a 75 basis point hike to a much lesser extent. As I have argued in past statements, 10 basis points is not material and I am happy to go along with the consensus of the rest of the MPC on this issue. Therefore, I vote in favour of increasing the policy repo rate by 50 basis points to 5.40 per cent. 43. I now turn to the second resolution to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. This statement confuses more than it clarifies. Because the rate hike in this meeting takes the policy rate above the pre-pandemic level, “withdrawal of accommodation” cannot refer to the withdrawal of the pandemic era accommodation. It can only mean withdrawal of the pre-pandemic accommodation that began with the rate cut from 6.50% to 6.25% in February 2019. A plain reading of this resolution would then be that the MPC is focused on taking the repo rate back to 6.50%. 44. In my view, such an indication of a terminal repo rate of 6.50% is totally unwarranted in the situation that we are in. The reality is that the Ukraine war and monetary tightening in the advanced economies have led to a very serious risk of recession in the world economy. In the face of this, commodity prices have collapsed from their April peaks. Crude oil remained elevated for longer, but it too is softening even as the MPC meeting is in progress. If this trend continues, we could see significant downward adjustments to the projected inflation trajectory. Moreover, though the Indian economy has been highly resilient to geopolitical and commodity price shocks so far, the weakening of exports in July indicates that India would not be immune to growth shocks emanating from the rest of the world. In short, it is easy to imagine that a few months from now, the economic data could point to a terminal repo rate that is well below 6.50%. To focus on one thing implies paying less attention to other things, and I do not think it would be wise to say that the MPC will remain “focused” on withdrawal of accommodation ignoring other considerations. 45. I have made several different suggestions to the MPC regarding alternatives to this resolution. First, in June, I suggested that individual MPC members could start moving towards providing projections of the future path of the policy rate. Since these would be projections of individual members and not of the MPC as a whole, these projections would not tie the hands of the MPC itself in any way. At the same time, they would provide guidance to the public about the thinking within the MPC. Second, at this meeting, I suggested that this resolution should simply be dropped. It is better not to give any guidance than to give confusing guidance. Unfortunately, none of these proposals found favour with the other members. 46. At the same time, I do not wish to record an outright dissent on this resolution because clearly further withdrawal of accommodation is warranted. The terminal repo rate may or may not be 6.50% but it is almost certainly well above 5.40%. So I am confining myself to expressing my reservations on this resolution. The resolution should in my view be interpreted only as stating that there is a high likelihood of further front-loaded tightening without restricting the freedom of the MPC to respond to the changing environment in a data driven manner. Statement by Dr. Rajiv Ranjan 47. The risks to the global economy which were initially perceived as stagflationary are now increasingly surfacing to be that of an outright recession for most economies. This has fuelled a debate of hard4 versus soft landing for the global economy. Central banks are thus confronted with trade-offs which are governed by both the magnitude as well as the timing of their policy tightening. While the need to rein in inflationary pressures without numbing the growth impulses remains a priority, central banks are treading a very narrow path and they will need a well-curated policy design for a safe and soft landing. 48. Domestic inflation after reaching a peak of 7.8 per cent in April 2022 moderated to 7.0 per cent in May-June 2022. A sequential tapering of the month-on-month prices increases (momentum) along with large favourable base effects in May brought about this softening. Headline CPI price momentum eased to 0.94 per cent in May and further to 0.52 per cent in June from an elevated 1.43 per cent in April. Headline CPI on a seasonally adjusted annualised rate (SAAR) basis also slowed down from 12.8 per cent in April to 2.6 per cent in June. In terms of contributions, while the deceleration in headline price momentum in May was primarily on account of core (CPI excluding food and fuel), food also started to contribute to the slowdown in headline price pressures by June. The deceleration in price momentum was broad-based across items within the food group. On the other hand, the softening in core momentum was primarily influenced by the one-off petrol and diesel price declines (reflecting the full direct impact of excise duty cut). Despite some softening, various trimmed mean measures of CPI inflation5 for June were elevated, in the range of 5.7 per cent to 6.4 per cent. In spite of some softening, diffusion indices6 for core CPI items were also at elevated levels, implying that underlying price pressures remain broad based. 49. Inflation expectations of households in India, being adaptive and backward-looking and influenced mainly by price expectations of food and fuel items (which constitute almost 55 per cent of the CPI basket), moderated in the July 2022 round but remained at elevated levels. Unmooring of inflation expectations, in the context of the spike in inflation following the conflict in Europe, is the biggest risk which the MPC addressed through the off-cycle meet and frontloaded rate actions so as to increase the efficacy of the actions. 50. Going forward, though the fall in international commodity prices and the progress of the monsoon provide room for optimism, there is considerable uncertainty, particularly from the spatial and temporal distribution of monsoon and its implication for kharif paddy production, the depreciation of the INR exchange rate and pending pass-through in services. Importantly, the global geo-political scenario – the source of much of the price shocks – continues to remain unsettled. 51. While WPI inflation rose sharply in line with international commodity price movements, the full pass-through of high inputs costs reflected in WPI to CPI inflation was tempered by weak pricing power due to the prevailing slack in the economy. As the slack wanes and pricing power of firms return, there is a risk that the pass-through of past increases in input costs could continue, partly offsetting the favourable impact of recent fall in global commodity prices. Crude price uncertainty persists, though the pass-through of elevated crude oil prices to retail inflation has been moderate and low in the recent period7 due to the impact of fiscal interventions, such as reduction in excise duties. Moreover, the recent depreciation of the INR exchange rate could also temper the beneficial impact of fall in commodity prices. These could keep core CPI inflation at elevated levels throughout this year. Moreover, if high cost of living conditions persists, the household inflation expectations could edge up feeding into wages in a broad-based manner and pushing up services inflation, which has been muted so far. Thus, monetary policy needs to be watchful of the evolving input cost pass-through and wage dynamics and take pre-emptive action to contain any possibility of the emergence of a wage-price spiral. 52. As mentioned in my minutes of June policy, we need to factor in quicker and improved monetary transmission with the introduction of the external benchmark regime in this tightening cycle while arriving at a terminal rate. In response to the interest rate cycle turning upwards, banks have swiftly increased their external benchmark linked lending rates (EBLRs) (by 90 bps) and the 1-year median marginal cost of funds-based lending rate (MCLR) (by 40 bps) during April-July, 2022. The weighted average lending rate (WALR) on fresh rupee loans has also increased. Though pass-through is relatively lower in case of retail term deposit rates, banks have increased their bulk deposit rates significantly. As credit growth is gathering momentum, banks can be expected to further increase rates on retail deposits to fund their lending. Moreover, with upward revisions in interest rates on small savings schemes (SSSs) in accordance with the formula-based mechanism as and when it happens, pressure will increase on banks to hike interest rates on retail deposits. 53. On balance, the inflation projection for the financial year 2022-23 is retained at 6.7 per cent, with a gradual moderation in headline inflation over H2:2022-23. As per the baseline projections, inflation is likely to remain above 6 per cent till Q3:2022-23. This would require monetary policy to persevere with its exit from accommodation to ensure that frontloaded policy rate hikes dampen inflation expectations, anchor second round effects and firmly establish our commitment to price stability. The frontloading of policy actions is expected to strengthen monetary policy credibility and temper the need for aggressive rate hikes in future. Greater credibility makes disinflation less costly, helps hold down inflation once it is low (Blinder, 20008). The dividends of establishing this credibility are not just in the contemporaneous transmission into the real economy, but also in lowering the necessary terminal policy rate to achieve the inflation target in the medium run. Deft macroeconomic management has insulated the Indian economy from several shocks in the recent past thereby ensuring that recovery remains on a firm footing. Against this background, I vote for a 50 bps hike in the repo rate so as to reinforce the MPC’s commitment to price stability around the target. I also vote to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Statement by Dr. Michael Debabrata Patra 54. The global outlook becomes increasingly uncertain and tilted by downside risks. With inflation remaining elevated worldwide and a pervasive sense of guilt about the consequences of the pandemic stimulus having been underestimated9, central banks have launched into the most aggressive, front loaded and synchronous monetary policy tightening in decades. Consequently, the probability of a recession or hard landing has risen to levels that preceded actual recessions in the past. 55. Each country is on its own - match the Fed or face currency depreciation, imported inflation, wider current account imbalances, capital outflows and reserve losses. Meanwhile, the war in Ukraine appears to be broadening and it is unlikely to cease soon. Friend shoring has begun10. 56. The elephant in the room is the unrelenting strength of the US dollar which has risen by over 8.3 per cent since March 31, 2022 just to set up a numeraire. In India, there is a turn in the wind and financial markets are sensing it. The most recent demonstration of this shift is the strong appreciation of the Indian rupee in the relief rally that followed the fully priced in monetary policy action of the Fed in its July 2022 meeting. During the financial year 2022-23 so far (up to August 3), the Indian rupee has fallen by 3.9 per cent, 4.4 percentage points less than the MSCI advanced economy currency index and by 1.3 percentage points less than the MSCI EME currency index (5.1 per cent) against the US dollar. 57. This wedge reflects the underlying strength of India’s fundamentals. For instance, inflation in India is lower than the weighted average of its major trading partners11. High frequency indicators suggest that there is some moderation in momentum in the first quarter of 2022-23 relative to the previous quarter, but the momentum is still positive in sharp contrast to the rest of the world. India’s real GDP growth is tracking the RBI’s projections, in spite of the downside bias imparted by the highly unsettled global environment. Portfolio investment is making its way back to India – the month of July has recorded net inflows of US $ 458 million, led by equities12. In a span of around one month since June 17, 2022, the BSE Sensex has risen by 13.6 per cent - these gains coincide with the corporate earnings season, with many companies delivering robust first quarter results. The yield on the 10-year G-sec benchmark has softened from its peak of 7.62 per cent on June 16, 2022 and is trading 30-40 basis points below. Surplus liquidity in the banking system has moderated as credit growth has surged. Interest rates in the money markets have aligned with the policy repo rate, reflecting the stance of calibrated withdrawal of accommodation. Other short-term rates have firmed up. Monetary transmission is stronger to lending rates currently, but deposit rates have commenced the catch-up. All in all, the Indian economy is running a positive growth differential vis-à-vis the rest of the world. 58. Monetary policy, unseen and unsung, has played a key role in this swivel. The front-loaded and pre-emptive actions so far are already working into inflation expectations of households. Their perception of current inflation as well as their expectations three months and one year ahead have declined appreciably in the latest round of the RBI’s survey. Furthermore, uncertainty around their perceptions and expectations (measured by their respective coefficients of variation) has reduced, indicative of anchoring. Consumer confidence about price pressures easing across product groups over the year ahead is rising. In a world of global food shortages and price pangs, steady procurement operations and comfortable buffer stocks are positives for the growth outlook and positives for the food inflation trajectory. Undoubtedly, a more even spatial distribution of the south west monsoon could fortify these cushions further. 59. Although inflation seems to have peaked, it is still unconscionably high. Risks to the trajectory of inflation in the form of currency depreciation, seasonal pressures and the monsoon’s uneven progress could upend the moderation in momentum recently recorded. 60. Monetary policy’s response to supply shocks has to be predicated on managing expectations and fortifying credibility. Empirically, it can be demonstrated that when a shock is transitory, inflation returns to equilibrium without the need for any monetary policy action if credibility is high. On the other hand, repeated supply shocks trigger second round effects through cost pushes, expectations, exchange rate and demand channels, warranting pre-emptive monetary policy action. Even with perfect credibility, monetary policy cannot look through the second-round effects of repeated supply shocks. The inflation target may be breached for a prolonged period. This could unsettle expectations and eventually get reflected in higher inflation. Higher credibility can reduce – not substitute for – the monetary policy response to second round effects of repeated supply shocks. By frontloading monetary policy actions, credibility is demonstrated by showing commitment to the inflation target. 61. Another dimension of monetary policy credibility is the timing of its response. With imperfect credibility, a delay in the monetary policy response to repeated unfavourable supply shocks leads to a further loss of credibility, unhinging of inflation expectations and eventually, higher inflation outcomes with a higher sacrifice of growth. Accordingly, it is essential to (a) assess the life of the shock and (b) react to any signs of second round effects to avoid the generalisation of inflation. 62. At the current juncture, shocks are large and recurring. Combined with the rebound in spending liberated from the pandemic, they carry the risk of un-anchoring inflation expectations. Frontloading of monetary policy actions can keep inflation expectations firmly anchored, re-align inflation with the target and reduce the medium-term growth sacrifice as it is timed into the recovery underway. Small steps over a prolonged period could allow inflation to get entrenched and inflation expectations unhinged. 63. I vote for increasing the policy rate by 50 basis points and for the stance of withdrawal of accommodation as articulated in the MPC’s resolution. Statement by Shri Shaktikanta Das 64. Since the last MPC meeting in June 2022, there has been considerable slowdown in the global economy, which is now expected to grow only by 3.2 per cent in 2022 according to the International Monetary Fund (IMF). At the same time, global inflation has hardened further and is projected to remain elevated and persist for longer at around 6.6 per cent for advanced economies (AEs) and 9.5 per cent for emerging market and developing economies (EMDEs) (IMF, July 2022). This has triggered a synchronised and aggressive monetary tightening by central banks across the world, leading to tighter global financial conditions after almost a decade of accommodative policies. 65. On the domestic front, though inflation has moderated and plateaued since its recent peak of April 2022, it remains unacceptably and uncomfortably high. The high level of inflation continues to be broad-based with 13 out of 23 CPI sub-groups/groups, comprising close to 60 per cent of the CPI basket, registering more than 6 per cent inflation in June 2022. Going forward, though there are early indications that inflation might have peaked in April, significant uncertainties remain on account of adverse global spillovers coming from simmering geopolitical tensions, volatile global commodity prices and financial markets. While the let-up in global food and industrial metals prices should lower imported inflation, the appreciation of the US dollar could offset some of the gains. Persistently elevated cost of living conditions can engender wage-price spirals, especially as firms regain pricing power. 66. Domestic growth, on the other hand, remains resilient and gives us the space to act. High-frequency indicators for Q1:2022-23 and thereafter are evolving on the expected trajectory. The southwest monsoon has picked up and is progressing well. This will boost the prospects of agriculture and help revitalisation of rural consumption. Contact-intensive services have rebounded and have been driving consumer demand and growth. Government expenditure, both of Centre and states, is expected to provide support to aggregate demand. 67. Sustained high inflation, unless addressed effectively, could result in unanchoring of inflation expectations and their second order effects. This necessitates appropriate monetary policy response to prevent upward drift in inflation from the target rate. I am of the view that at this juncture a 50 bps increase in the repo rate is necessary and, therefore, vote accordingly. I also vote for remaining focused on withdrawal of accommodation. 68. Our monetary and liquidity actions have been aimed at ensuring continued macroeconomic and financial stability that could set the foundation for a high growth trajectory over the medium term. We will continue with ‘whatever it takes’ approach, given the new set of challenges and very high uncertainties that we are confronted with. 69. Our actions today are tailored towards first bringing the CPI inflation within the target band and then taking it close to the target of 4.0 per cent over the medium term, while supporting growth. The sequence of our policy measures is expected to strengthen monetary policy credibility and anchor inflation expectations. Our actions would continue to be calibrated, measured and nimble depending upon the unfolding dynamics of inflation and economic activity. (Yogesh Dayal)

Chief General Manager Press Release: 2022-2023/737

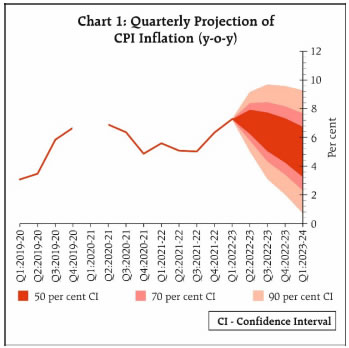

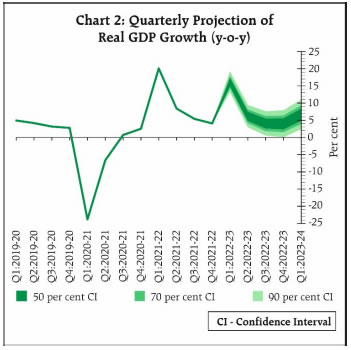

|