By Dr. Raghuram G. Rajan, Governor Monetary and Liquidity Measures On the basis of an assessment of the current and evolving macroeconomic situation, it has been decided to: -

keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.75 per cent; -

keep the cash reserve ratio (CRR) of scheduled banks unchanged at 4.0 per cent of net demand and time liability (NDTL); -

continue to provide liquidity under overnight repos at 0.25 per cent of bank-wise NDTL at the LAF repo rate and liquidity under 14-day term repos as well as longer term repos of up to 0.75 per cent of NDTL of the banking system through auctions; and -

continue with daily variable rate repos and reverse repos to smooth liquidity. Consequently, the reverse repo rate under the LAF will remain unchanged at 5.75 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 7.75 per cent. Assessment 2. Since the fourth bi-monthly statement of September 2015, global growth continues to be weak. Global trade has slowed further with waning demand and oversupply in several primary commodities and industrial materials. In the United States, inventory accumulation is likely to hold down growth in Q4 of 2015. Industrial production slumped in October on cutbacks in oil drilling, while exports were undermined by the strengthening US dollar. Consumer confidence was, however, supported by the diminishing slack in the labour market. In the Euro area, high frequency indicators such as retail sales, purchasing managers’ indices and unemployment point to an uptick in a still anaemic recovery, with monetary policy expected to be increasingly supportive as risks of undershooting the inflation target persist. In China, slowing nominal GDP growth and high debt continue to raise concerns, especially given the overcapacity in certain sectors. Other emerging market economies (EMEs) continue to face headwinds from domestic structural constraints, shrinking trade volumes and depressed commodity prices. 3. Global financial markets began Q4 on a calmer note after the Federal Open Market Committee stayed on hold in September. Stock markets recorded modest gains in October; major currencies recouped some ground against the US dollar and crude oil traded briefly above US $ 50 per barrel for the first time since July. Markets were also boosted by the easing of monetary policy in China and indications of further stimulus in the Euro area and Japan. Following the early November release of robust US jobs data which increased the likelihood of US monetary policy starting to normalise in December, the US dollar has appreciated significantly, and US yields have hardened. Bond markets in EMEs have generally been tracking the hardening of US yields. Currency markets in EMEs have experienced selling pressures as portfolio investors continue to exit them as an asset class. Unease in investor sentiment is likely to increase ahead of the imminent divergence in advanced economy monetary policy stances. 4. On the domestic front, provisional estimates of gross value added (GVA) at basic prices for Q2 of 2015-16 rose on the back of acceleration in industrial activity. Other indicators suggest the economy is in the early stages of a recovery, though with some areas of continued weakness. 5. Value added in agriculture and allied activities picked up on the modest increase in kharif output and timely policy interventions to stem the effects of the deficient south-west monsoon. Turning to Q3, the north-east monsoon commenced on a listless note, but the subsequent cyclonic weather has improved precipitation and raised the probability of a normal monsoon as predicted by the Indian Meteorological Department. Nevertheless, the exceptionally dry start to the season affected sowing in all major rabi crops, while the excessive rains that followed may have reduced the prospects of coffee and paddy. Overall, the current outlook for agricultural growth in 2015-16 appears moderate at best at this juncture. 6. The Index of Industrial Production picked up in the second quarter. Early results of the Reserve Bank’s order books, inventories and capacity utilisation survey indicate that there was robust growth in new manufacturing orders in the second quarter, and finished goods inventories declined while raw materials inventories increased. Not all indicators, however, are positive. While urban consumption is showing signs of a pick-up in some areas such as passenger vehicles sales, rural demand has been weakened by two consecutive deficient monsoons and slowing construction activity. Nevertheless, new project announcements as measured by the Centre for Monitoring Indian Economy grew more strongly in the second quarter. It remains to be seen whether growing public investment can crowd in private investment on a sustained basis, despite the still-low capacity utilisation. 7. Lead indicators of services sector are mixed. The services purchasing managers’ index increased in October 2015 on account of improvement in new business orders. Commercial vehicle sales (reflecting transportation demand) and domestic civil aviation passenger traffic accelerated year-on-year. On the other hand, tourist arrivals, cargo handled at major ports, railway freight traffic, domestic and international air cargo traffic, and measures of construction such as steel consumption slowed. Recent policy initiatives relating to rail, port and road projects are likely to improve construction activity, as will the Reserve Bank’s countercyclical reduction of capital charges on low income housing loans, albeit with gestation lags. 8. As anticipated in our previous policy, retail inflation measured by the consumer price index (CPI) increased for the third successive month in October 2015, pushed up by a surge in the monthly momentum. Food inflation rose sharply in October, driven especially by pulses. 9. CPI inflation excluding food, fuel, petrol and diesel also rose for three consecutive months on account of price increases in respect of housing, recreation and amusement, and personal care and effects. Within this broad category, education and health services contributed most to headline inflation. Households’ inflation expectations remain elevated although they have edged lower recently, perhaps in response to lower prices of petrol and diesel. Rural wage growth, as also corporate staff costs, remain subdued. 10. Underlying liquidity conditions tightened in October-November with the festival season draining currency from the system and some slowdown in government expenditure. In response, the Reserve Bank conducted variable rate repo and reverse repo auctions of various tenors in addition to regular 14-day variable rate repo. As a result, average net daily liquidity absorptions of ₹ 119 billion in Q2 gave way to average daily net injection of ₹ 372 billion in October, which scaled up to ₹ 856 billion in November. Money market rates remained around the policy repo rate – only rising slightly in the second week of November at the height of festival currency demand. Bank credit in the form of personal loans grew strongly as did non-bank financing flows particularly through commercial paper, public equity issues and housing finance. 11. In the external sector, exports contracted for the eleventh month in a row to October, indicative of the persisting weakness in global trade. Excluding petroleum products (PoL), however, the decline in exports was more moderate and early signs of a turnaround are visible in respect of readymade garments, drugs and pharmaceuticals and electronics. With global commodity prices, especially those of crude, softening further, both PoL and non-PoL exports continued to contract, with the latter shrinking for the fourth consecutive month. The decline in bullion imports despite the festival season helped narrow the trade deficit in October as well as over the financial year so far, moderating the current account deficit further. Net foreign direct investment (FDI), external commercial borrowings and accretions to non-resident deposits have risen in relation to last year; however, portfolio outflows from both debt and equity segments rose in November. During 2015-16 (up to November 20), there has been an accretion of US$ 10.8 billion to the foreign exchange reserves. Policy Stance and Rationale 12. In the bi-monthly monetary policy statement of September, the Reserve Bank assessed that the inflation target for January 2016 at 6 per cent was within reach. Accordingly, it front-loaded its policy action in response to weak domestic and global demand that were holding back investment, while noting that structural reforms and productivity improvements would continue to provide the main impetus for sustainable growth. 13. Since then, inflation has turned up as anticipated, and is expected to rise further until December before plateauing. Although the seasonal moderation in prices of vegetables and fruits is expected to provide some respite, the El Nino induced shortening of winter may limit this effect. The early indications of rabi sowing together with low reservoir levels suggest that astute supply management by the central government, including close coordination with State governments, is necessary to minimize any shortfall in the rabi crop. While oil prices, barring geopolitical shocks, are expected to remain benign for a few quarters more, the uptick of CPI inflation excluding food and fuel for two months in succession warrants vigilance. Taking all this into consideration, inflation is expected to broadly follow the path set out in the September review with risks slightly to the downside (Chart 1).  14. The outlook for agriculture is subdued, in view of both rabi and kharif prospects being hit by monsoon vagaries. While there are areas of robust growth in manufacturing such as capital goods and passenger cars, weak rural and external demand holds back stronger overall growth. Similarly, while prospects for a revival in service sector activity have been boosted by optimism on new business, pockets of lacklustre activity such as construction weigh on the overall outlook. The step-up in public capital spending and the easing stance of monetary policy provide the enabling environment for a revival in private investment demand, supported by easing input prices and improving conditions for doing business. The growth projection for 2015-16 has accordingly been kept unchanged at 7.4 per cent with a mild downside bias (Chart 2).  15. The Reserve Bank will follow developments on commodity prices, especially food and oil, even while tracking inflationary expectations and external developments. The implementation of the Pay Commission proposals, and its effect on wages and rents, will also be a factor in the Reserve Bank’s future deliberations, though its direct effect on aggregate demand is likely to be offset by appropriate budgetary tightening as the Government stays on the fiscal consolidation path. In the meantime, since the rate reduction cycle that commenced in January, less than half of the cumulative policy repo rate reduction of 125 bps has been transmitted by banks. The median base lending rate has declined only by 60 bps. The Reserve Bank will shortly finalise the methodology for determining the base rate based on the marginal cost of funds, which all banks will move to. The Government is examining linking small savings interest rates to market interest rates. These moves should further help transmission of policy rates into lending rates. In addition, the on-going clean-up of bank balance sheets will help create room for fresh lending. The Reserve Bank will use the space for further accommodation, when available, while keeping the economy anchored to the projected disinflation path that should take inflation down to 5 per cent by March 2017. 16. The sixth bi-monthly monetary policy statement will be announced on Tuesday, February 2, 2016. Alpana Killawala

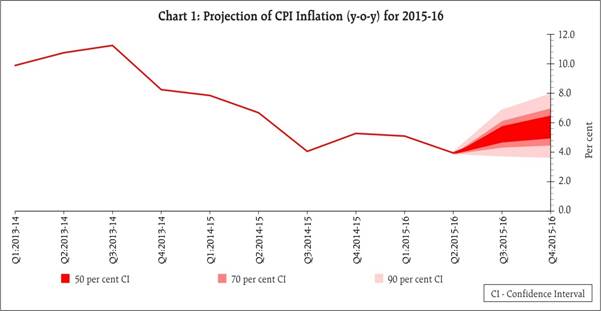

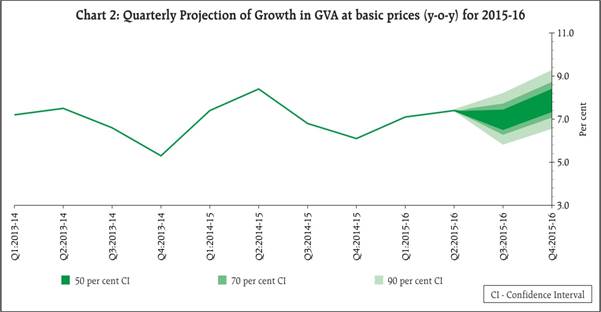

Principal Chief General Manager Press Release : 2015-2016/1278 |