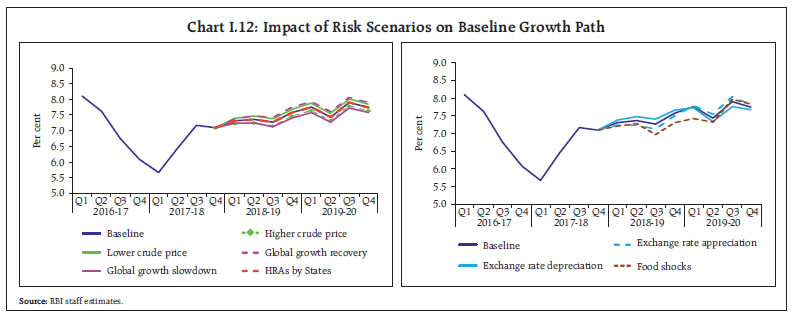

| I. Macroeconomic Outlook Inflation is expected to firm up during the first quarter of 2018-19 before moderating in the remaining part of 2018-19 as the direct impact of the increase in house rent allowances for central government employees fades away, which has to be looked through. Economic activity is expected to accelerate with the strengthening of investment activity, supported by consumption demand and robust credit growth. The Monetary Policy Report (MPR) of October 2017 flagged significant shifts underway in the macroeconomic environment. Some of them have gained traction since then while others are incipiently in motion. Global economic activity has continued to strengthen and is becoming increasingly synchronised across regions. Global trade is outpacing demand after lagging behind for two years. Oil prices have firmed up again on the edge of a delicate demand-supply balance. Generally buoyant global financial markets have been interrupted by bouts of volatility triggered by several event-specific announcement effects, and most recently by reassessments of the pace of monetary policy normalisation in the US. Renewed fears of protectionism, retaliatory actions and trade wars pose a major challenge to the global economy, with implications for emerging market economies (EMEs), including India, that are participating in open international trade and relying on foreign capital flows to realise their developmental aspirations. After languishing for five consecutive quarters, economic activity in India is quickening, as estimates and high frequency as well as survey-based indicators etch out for the second half of 2017-18. Growth is strengthening and several elements are coming together to nurture this nascent acceleration: expectations of a record foodgrains output; strong sales growth by corporations; depleting finished goods inventories; and, restart of investment in fixed assets by corporations pointing to renewal of the capex cycle. Several services sectors, including the information technology sector in terms of its international competitiveness, have shown resilience. These are some of the developments that support brighter prospects for the Indian economy in 2018-19. A significant development has been that this time around, the step-up in growth is propelled by a revival of investment on the demand side and manufacturing on the supply side. This outlook will be lifted by tailwinds from remonetisation and implementation of Goods and Services Tax (GST). The path of inflation will likely be influenced by effects of the increase in house rent allowances (HRAs) for central government employees, which is purely statistical and has to be looked through to gauge true inflation developments. As this effect wanes, inflation could moderate in the remaining part of 2018-19 from an upturn in Q1 under the baseline assumptions. Fiscal slippages for 2017-18 and 2018-19, along with the postponement of the medium-term adjustment path, are a key risk to the growth and inflation outlook. Monetary Policy Committee: October 2017-February 2018 The Monetary Policy Committee (MPC) met in December 2017 and February 2018 in accordance with the pre-announced bi-monthly schedule. The MPC voted to keep the policy rate on hold in these meetings, maintaining its neutral stance of the fourth bi-monthly resolution of October 2017. The MPC’s resolutions as well as individual minutes and voting patterns reflected concerns about the changing inflation trajectory – upside risks to the inflation outlook from food and fuel prices, rising input cost conditions, fiscal slippages, and volatile global financial markets in its December resolution; and increase in HRAs by state governments, crude oil and other commodity prices, revisions to minimum support prices (MSPs) and fiscal slippages in its February resolution. The seasonal moderation in prices of vegetables and fruits, subdued capacity utilisation, and moderate rural real wage growth were seen as mitigating factors. | Table I.1 Monetary Policy Committees and Voting Patterns | | Country | Number of Policy Meetings: October 2017-March 2018 | | Total Meetings | Meetings With Full Consensus | Meetings With Dissents | | Brazil | 4 | 4 | 0 | | Chile | 5 | 5 | 0 | | Colombia | 5 | 1 | 4 | | Czech Republic | 4 | 3 | 1 | | Hungary | 5 | 5 | 0 | | Israel | 4 | 3 | 1 | | Japan | 4 | 0 | 4 | | South Africa | 3 | 1 | 2 | | Sweden | 3 | 2 | 1 | | Thailand | 4 | 3 | 1 | | UK | 4 | 2 | 2 | | US | 4 | 3 | 1 | | Source: Central bank websites. | Against this backdrop, the MPC voted in December by a majority of 5-1 to maintain status quo on the policy rate, while continuing with a neutral stance. As in the October meeting, one member voted for a rate cut to support economic activity. In February, the MPC persevered with status quo on the policy rate with a vote of 5-1 and a neutral stance, while reiterating its commitment to keep headline inflation close to 4 per cent on a durable basis. In view of several drivers of inflation firing at the same time and the upper tolerance band of inflation target under threat, one member voted for a 25 basis points (bps) increase in the policy rate to commence the withdrawal of accommodation. These subtle variations in voting patterns reflecting individual members’ views on the current and evolving macroeconomic outlook as well as policy preferences on the weights they assign to deviations of inflation and output from target/ potential are also observed in recent experiences of the MPCs in other countries (Table I.1). Macroeconomic Outlook Chapters II and III present macroeconomic developments during October 2017–March 2018 and also explain the reasons for deviations of actual outcomes of inflation and growth from staff’s projections in the October 2017 MPR. Turning to the outlook, the recent evolution of domestic and global macroeconomic developments warrant revisions in the baseline assumptions (Table I.2). | Table I.2: Baseline Assumptions for Near-Term Projections | | Indicator | October 2017 MPR | Current (April 2018) MPR | | Crude Oil (Indian Basket) | US$ 55 per barrel during 2017-18: H2 | US$ 68 per barrel during 2018-19 | | Exchange rate | ₹ 65/US$ | Current level | | Monsoon | 5 per cent below LPA in 2017 | Normal for 2018 | | Global growth | 3.5 per cent in 2017

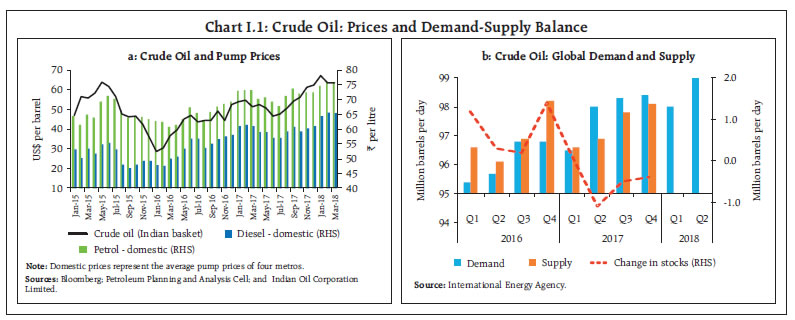

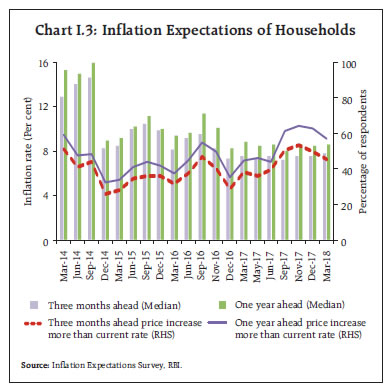

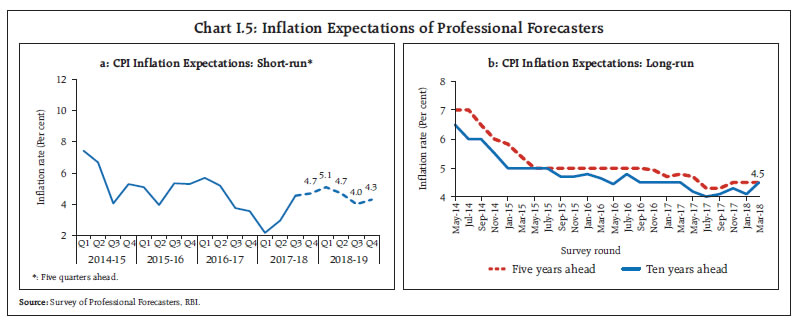

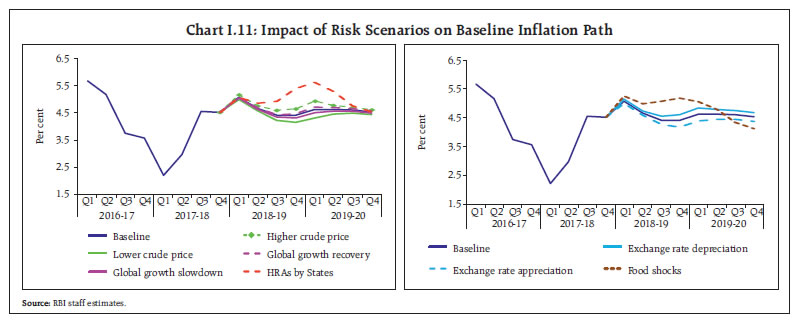

3.6 per cent in 2018 | 3.9 per cent in 2018

3.9 per cent in 2019 | | Fiscal deficit | To remain within BE 2017-18

(3.2 per cent of GDP) | To remain within BE 2018-19

(3.3 per cent of GDP) | | Domestic macroeconomic/ structural policies during the forecast period | No major change | No major change | Notes: 1. The Indian basket of crude oil represents a derived numeraire comprising sour grade (Oman and Dubai average) and sweet grade (Brent) crude oil processed in Indian refineries in the ratio of 72:28.

2. The exchange rate path assumed here is for the purpose of generating staff’s baseline growth and inflation projections and does not indicate any ‘view’ on the level of the exchange rate. The Reserve Bank is guided by the objective of containing excess volatility in the foreign exchange market and not by any specific level of/band around the exchange rate.

3. Global growth projections are from the World Economic Outlook (July 2017 and January 2018 updates), International Monetary Fund (IMF).

4. BE: Budget Estimates.

5. LPA: Long period average (average rainfall during 1951-2000). | First, crude oil prices (Indian basket) firmed up from US$ 56 a barrel in October 2017 to US$ 67 a barrel in January 2018 (Chart I.1). Thereafter, they have fluctuated between US$ 60 and US$ 67. With the Organisation of the Petroleum Exporting Countries (OPEC) extending production cuts through the end of 2018 and the drawdown of inventories to meet increasing demand, being buffeted somewhat by the response of US shale oil production, the baseline scenario assumes crude oil prices (Indian basket) to average around US$ 68 a barrel in 2018-19. Second, the exchange rate (Indian rupee vis-à-vis the US dollar) has exhibited two-way movements since October 2017. It appreciated till the early part of January 2018 on buoyant capital inflows and weakening of the US dollar. Subsequently, it depreciated from early February, following the release of stronger than expected US non-farm payrolls and wages data that fuelled expectations of a faster pace of interest rate increases by the US Federal Reserve and over concerns of the impact of higher crude oil prices on India’s trade deficit. By March, the exchange rate of the rupee was close to its October 2017 level.  Third, the pace of global economic activity in 2017 turned out to be stronger than expected due to robust growth in the advanced economies (AEs) and significantly stronger growth in EMEs. Global growth is expected to accelerate further in 2018, benefitting from the boost to investment demand in the US from corporate tax cuts, robust recovery in the euro area and generally improved growth outlook in EMEs (Chart I.2). The sharp recovery in world trade is expected to sustain in 2018 and enlarge the prospects of another year of strong and resilient global activity. I.1 The Outlook for Inflation Headline CPI inflation reached a peak of 5.2 per cent in December 2017 (4.9 per cent, excluding the estimated impact of HRA for central government employees), reflecting an unseasonal spike in the prices of vegetables and the full impact of the central government implementing the 7th Central Pay Commission’s (CPC’s) HRA award. The delayed setting in of the seasonal food prices moderation took down headline inflation to 4.4 per cent in February (4.1 per cent, excluding the estimated impact of HRA for central government employees). It is likely that this softening will keep the reading for March benign before it reverses in April. The incidence and strength of this reversal will condition monetary policy responses in 2018-19. Turning to the outlook, inflation expectations of urban households remain elevated, according to the March 2018 round of the Reserve Bank’s survey.1 Inflation expectations three months ahead and a year ahead increased by 30 bps and 10 bps, respectively, from the previous round (December) to 7.8 per cent and 8.6 per cent, respectively. The proportion of respondents expecting the general price level to increase by more than the current rate declined for both three months and one year horizons (Chart I.3).  Manufacturing firms polled in the Reserve Bank’s industrial outlook survey (March 2018) expected higher input price pressures in Q1:2018-19 due to rising cost of raw materials (higher negative values for cost of raw materials indicate higher input price pressures) (Chart I.4).2 Selling prices are also expected to increase, but not sufficient to protect profit margins. The Nikkei’s purchasing managers’ survey also indicates both input and output price pressures for manufacturing (March 2018) as well as services (February 2018) sectors. Professional forecasters surveyed by the Reserve Bank in March 2018 expect CPI inflation to firm up to 5.1 per cent in Q1:2018-19 and moderate thereafter to 4.3 per cent in Q4:2018-19 (Chart I.5).3 Their medium-term inflation expectations (5 years ahead) remained unchanged at 4.5 per cent, while longer-term inflation expectations (10 years ahead) increased by 40 bps to 4.5 per cent.  Taking into account the initial conditions, signals from the forward looking surveys and estimates from structural and other models, CPI inflation is projected to pick up from 4.4 per cent in February 2018 to 5.1 per cent in Q1:2018-19 due to unfavourable base effects and then moderate to 4.7 per cent in Q2, and 4.4 per cent in Q3 and Q4, with risks tilted to the upside (Chart I.6). It may be noted that the direct impact of the increase in the HRA announced by the Central Government fades away fully by December 2018. The 50 per cent and the 70 per cent confidence intervals for inflation in Q4:2018-19 are 3.2-5.9 per cent and 2.5-6.7 per cent, respectively. Excluding the estimated impact of HRA for central government employees, CPI inflation would pick up from 4.1 per cent in February 2018 to 4.7 per cent in Q1:2018-19 and then moderate to 4.4 per cent in Q2, Q3 and Q4. For 2019-20, assuming a normal monsoon and no major exogenous/policy shocks, structural model estimates indicate that inflation will move in a range of 4.5-4.6 per cent. The 50 per cent and the 70 per cent confidence intervals for Q4:2019-20 are 3.0-6.1 per cent and 2.2-7.0 per cent, respectively. There are a number of upside risks to the baseline forecasts. Although the direct impact on headline inflation is statistical and should be looked through for policy purposes, second order effects of the expected increases in HRA, including by state governments, can impact inflation expectations. Other major risks to the inflation outlook are crude oil and other commodity prices, the proposed revisions to MSPs for kharif crops, and fiscal slippage at both the central and state levels. I.2 The Outlook for Growth Going forward, economic activity is expected to gather pace in 2018-19, benefitting from a conducive domestic and global environment. First, the teething troubles relating to implementation of the GST are receding. Second, credit off-take has improved in the recent period and is becoming increasingly broad-based, which portends well for the manufacturing sector and new investment activity. Third, large resource mobilisation from the primary market could strengthen investment activity further in the period ahead. Fourth, the process of recapitalisation of public sector banks and resolution of distressed assets under the Insolvency and Bankruptcy Code (IBC) may improve the business and investment environment. Fifth, global trade growth has accelerated, which should encourage exports and reduce the drag from net exports. Sixth, the thrust on rural and infrastructure sectors in the Union Budget could rejuvenate rural demand and also crowd in private investment. Notwithstanding these salubrious developments, consumer confidence dipped in the March 2018 round of the Reserve Bank’s survey, with the respondents expecting a moderation over the year ahead in general economic conditions, employment situation and their income (Chart I.7).4 Overall sentiment in the manufacturing sector a quarter ahead also fell in the March 2018 round of the Reserve Bank’s industrial outlook survey under the weight of weaker prospects for production, order books, capacity utilisation, employment and profit margins (Chart I.8). However, surveys conducted by other agencies indicate an improvement in business confidence (Table I.3). Manufacturing and services sector firms in the Nikkei’s purchasing managers’ surveys (March 2018 and February 2018, respectively) are optimistic about the outlook a year ahead, driven by expansion plans and expected improvement in demand conditions. | Table I.3: Business Expectations Surveys | | Item | NCAER Business Confidence Index

(January 2018) | FICCI Overall Business Confidence Index

(February 2018) | Dun and Bradstreet Composite Business Optimism Index

(January 2018) | CII Business Confidence Index (December 2017) | | Current level of the index | 129.3 | 71.6 | 91.0 | 59.7 | | Index as per previous Survey | 118.5 | 65.6 | 76.7 | 58.3 | | % change (q-o-q) sequential | 9.1 | 9.1 | 18.6 | 2.4 | | % change (y-o-y) | 15.4 | 23.0 | 39.1 | 5.7 | Notes: 1. NCAER: National Council of Applied Economic Research.

2. FICCI: Federation of Indian Chambers of Commerce & Industry.

3. CII: Confederation of Indian Industry. |

In the March 2018 round of the Reserve Bank’s survey, professional forecasters expected real gross domestic product (GDP) growth to pick up marginally from 7.2 per cent in Q3:2017-18 to 7.3 per cent in Q1:2018-19 and remain at 7.2 per cent in Q2-Q4 (Chart I.9 and Table I.4). Taking into account the baseline assumptions, survey indicators and model forecasts, real GDP growth is projected to improve from 6.6 per cent in 2017-18 to 7.4 per cent in 2018-19 – 7.3 per cent in Q1, 7.4 per cent in Q2, 7.3 per cent in Q3 and 7.6 per cent in Q4 – with risks evenly balanced around this baseline path.5 For 2019-20, the structural model estimates indicate real GDP growth at 7.7 per cent, with quarterly growth rates in the range of 7.4-7.9 per cent, assuming a normal monsoon, and no major exogenous/policy shocks (Chart I.10).

| Table I.4: Reserve Bank’s Baseline and Professional Forecasters’ Median Projections | | (Per cent) | | | 2017-18 | 2018-19 | 2019-20 | | Reserve Bank’s Baseline Projections | | | | | Inflation, Q4 (y-o-y) | 4.5 | 4.4 | 4.5 | | Inflation excluding the estimated impact of HRA for central government employees, Q4 (y-o-y) | 4.2 | 4.4 | 4.5 | | Real GDP Growth | 6.6 | 7.4 | 7.7 | | Assessment of Survey of Professional Forecasters@ | | | | | Inflation, Q4 (y-o-y) | 4.7 | 4.3 | | | Real GDP Growth | 6.6 | 7.3 | | | Gross Domestic Saving (per cent of GNDI) | 30.2 | 30.5 | | | Gross Fixed Capital Formation (per cent of GDP) | 28.5 | 29.0 | | | Credit Growth of Scheduled Commercial Banks | 10.0 | 11.3 | | | Combined Gross Fiscal Deficit (per cent of GDP) | 6.5 | 6.3 | | | Central Government Gross Fiscal Deficit (per cent of GDP) | 3.5 | 3.3 | | | Repo Rate (end-period) | 6.00 | 6.00 | | | Yield of 91-days Treasury Bills (end-period) | 6.2 | 6.3 | | | Yield of 10-years Central Government Securities (end-period) | 7.6 | 7.5 | | | Overall Balance of Payments (US$ billion) | 27.1 | 11.3 | | | Merchandise Exports Growth | 9.0 | 9.4 | | | Merchandise Imports Growth | 18.0 | 10.9 | | | Current Account Balance (per cent of GDP) | -1.9 | -2.1 | | @: Median forecasts; GNDI: Gross National Disposable Income.

Source: RBI staff estimates; and Survey of Professional Forecasters (March 2018). | Risks to the baseline growth scenario need to be monitored carefully. First, the uncertainty associated with the pace and timing of normalisation of monetary policy in the US and other major AE central banks has led to recurrent bouts of volatility in international financial markets which may have an adverse impact on capital flows and overall investment sentiment, including for EMEs through the “finance” channel. Second, protectionist measures in the US and the generalised threat of a trade war can exacerbate volatility in global financial markets, with spillovers to domestic financial markets and adverse implications for the growth outlook. Large revisions in past data on national accounts statistics also pose a challenge to forecasts (Box I.1). I.3 Balance of Risks The baseline projections of growth and inflation presented in the preceding sections are based on assumptions set out in Table I.2. However, there are large uncertainties around these baseline assumptions, posing risks to the baseline projections. The projected paths of growth and inflation under plausible alternative scenarios are discussed below. (i) International Crude Oil Prices The dynamics of oil prices over the past six months highlight the volatility associated with the oil market. The baseline scenario assumes crude oil prices (Indian basket) to average around US$ 68 a barrel during 2018-19. Global growth has surprised on the upside in recent quarters. If these conditions persist, global crude oil demand and hence prices could edge higher. Assuming crude oil prices average around US$ 78 in this scenario, inflation could be higher by 30 bps over the baseline and growth weaker by around 10 bps. On the other hand, there could be downward pressures on international crude prices if global economic activity were to turn weaker than expected (for a variety of factors discussed later) or shale gas output is ramped up further in response to elevated crude oil prices or OPEC members produce more than their agreed shares. Should the Indian basket crude price fall to US$ 58 per barrel in this scenario, inflation could ease by around 30 bps below the baseline, with a boost of around 10 bps to real GDP growth (Charts I.11 and I.12). Box I.1: National Accounts Data Revisions in India With the advancement of first advance estimates (FAE) of national accounts data by the Central Statistics Office (CSO) to the first week of January, the issue of large revisions in data has come to the fore. The first advance estimates are based on limited information, which get addressed gradually in successive revisions. An analysis of revisions of annual growth rates of major components of GDP in India between the first release and the latest available release shows a generally upward bias. On the production side, an analysis based on annual data (2003-04 onwards) and quarterly data (2002-03 onwards) reveals that the CSO revised annual real gross value added (GVA) growth estimates relative to advance estimates upwards in ten years (on an average of about 70 basis points), and downwards in the remaining four years (on an average of about 27 basis points) (Table I.1.1). In the case of real GDP, advance estimates were revised up in twelve years (an average of 81 basis points), and revised downwards only in two years (an average of 204 basis points). An analysis of GVA components shows that significant revisions were mainly in three sectors, viz. ‘mining and quarrying’, ‘manufacturing’ and ‘financial, real estate and professional services’. | Table I.1.1: First and Last Estimates of Real GVA Growth: Mean and Median of Differences (in percentage points) | | Variable | Annual Growth Rate (14 years) | Quarterly Growth Rate (60 quarters) | | Mean | Median | Mean | Median | | GVA | 0.43 | 0.37 | 0.55 *** | 0.54 *** | | Agriculture, forestry and fishing | 0.84 | 0.99 | 0.34 | 0.74 * | | Mining and quarrying | 2.34 | 1.18 | 1.97 *** | 0.58 *** | | Manufacturing | 2.06 | 1.75 | 2.09 *** | 1.13 *** | | Electricity, gas, water supply and other utility services | -0.20 | -0.36 | 0.35 | 0.45 * | | Construction | 1.34 | 0.51 | 0.75 | 0.60 | | Trade, hotels, transport, communication and services related to broadcasting | 0.47 | 0.87 | 0.34 | 0.64 | | Financial, real estate and professional services | 0.49 | 0.43 | 1.08 *** | 1.23 *** | | Public administration, defence and other services | -1.31 | -0.81 | -0.46 | -1.10 | Notes: 1. ***, ** and * indicates statistical significance at 1%, 5% and 10%, respectively.

2. Wilcoxon sign rank test has been performed for median.

3. The null hypothesis is that there is no difference in parameters for two or more sets of population. | From the expenditure side, the analysis of annual data from 2007-08 onwards and for quarterly data from 2009-10 onwards shows that private final consumption expenditure (PFCE), and exports and imports of goods and services were revised significantly (Table I.1.2). The analysis also reveals that during periods of rising growth, initial estimates were revised upwards in successive revisions, while during the periods of slackening of growth, revisions were in the downward direction – initial estimates understate in magnitude both upswings and downswings. Advance estimates of GDP/GVA growth may, therefore, need to be supplemented with high frequency indicators to arrive at a realistic assessment of the state of the economy (Prakash et al, 2018). Reference: Prakash, Anupam, A. K. Shukla, A. P. Ekka and K. Priyadarshi (2018), “Examining Gross Domestic Product Data Revisions in India”, Mint Street Memo (forthcoming), Reserve Bank of India. | Table I.1.2: First and Last Estimates of Real GDP Growth-Expenditure Side: Mean and Median of Differences (in percentage points) | | Variable | Annual Growth Rate (10 years) | Quarterly Growth Rate (32 quarters) | | Mean | Median | Mean | Median | | GDP | 0.38 | 0.56 | 0.71** | 0.36** | | Private final consumption expenditure | 1.56 | 1.14 | 1.31** | 1.19** | | Government final consumption expenditure | -0.92 | 0.41 | -0.12 | 2.49 | | Gross fixed capital formation | 1.96 | 1.91 | 2.89* | 0.80 | | Exports of goods and services | 1.97 | 1.29 | 3.59* | 2.04* | | Imports of goods and services | 2.99 | 2.43 | 15.33 | 2.67** | | Notes: Please see notes to Table I.1.1. | |

(ii) Global Growth The baseline scenario assumes global growth to gain upward momentum during 2018, buoyed by the boost to US investment demand from corporate tax cuts, strong activity in the euro area supported by accommodative monetary policy and improvement in growth prospects of EMEs. There are upside risks to the baseline with the synchronised cyclical rebound, revival of global trade and easy financing conditions reinforcing each other. If global growth turns out to be 50 bps over the baseline, it could strengthen domestic growth by 20 bps above the baseline and raise domestic inflation by around 10 bps.  On the other hand, protectionist policies, continuing uncertainty associated with the pace and timing of normalisation of monetary policy in the US and other systemic central banks, and higher crude oil prices pose downside risks to global demand. In such a scenario, if global demand weakens by 50 bps vis-à-vis the baseline, domestic growth and inflation could be 20 bps and around 10 bps, respectively, below the baseline. (iii) House Rent Allowances – Implementation by States The increase in the HRA by the central government for its employees is reflected in the inflation data since July 2017. There remains uncertainty, however, about the magnitude and timing of implementation of the HRA award by the state governments for their employees and these are, therefore, not included in the baseline inflation path. Assuming that all state governments implement increases in pay and allowances of the same order as the central government during the course of 2018-19, CPI inflation could turn out to be around 100 bps above the baseline on account of the direct statistical effect of higher HRAs, with additional indirect effects emanating from higher demand and increase in inflation expectations. As noted earlier, monetary policy should look through the direct statistical effects, while being vigilant about indirect effects working through inflation expectations. (iv) Exchange Rate The exchange rate of the Indian rupee vis-à-vis the US dollar has moved in both directions in recent months. Changing market perceptions about the pace and timing of monetary policy normalisation in the US, along with domestic inflation, fiscal slippage and current account balance developments, have been important factors driving exchange rate movements in the recent period and are likely to remain so in the near-term. With economic activity gathering pace in the euro area, uncertainty surrounding normalisation plans of the European Central Bank is likely to add to financial market volatility. The US macroeconomic policy mix – easy fiscal policy in an environment when monetary accommodation is being withdrawn – can accentuate market volatility. Assuming a depreciation of the Indian rupee by around 5 per cent relative to the baseline, inflation could edge higher by around 20 bps and the boost to net exports could increase growth by around 15 bps. On the other hand, with growth picking up in recent months, sound domestic fundamentals and the various initiatives taken by the Government to boost investment, India may continue to be an attractive destination for foreign investment, which could put upward pressures on the currency. An appreciation of the Indian rupee by 5 per cent in this scenario could soften inflation by around 20 bps and reduce growth by around 15 bps in 2018-19. (v) Risks to Food Inflation The baseline projections of growth and inflation assume a normal south-west monsoon, which is supported by early signals of likely ENSO (El Nino – Southern Oscillation) neutral conditions. The India Meteorological Department (IMD) is yet to release its forecast on the south-west monsoon season for 2018. Given the sensitivity of the agricultural sector to rainfall conditions, the actual growth and inflation dynamics would critically depend on the progress of the monsoon. A deficient monsoon could lower overall GDP growth by around 20-30 bps in 2018-19. Furthermore, the Union Budget has proposed revised guidelines for arriving at the MSPs for kharif crops, although the details are not yet fully available. If the monsoon is deficient and the budget proposals on MSPs lead to higher food prices, headline inflation could rise above the baseline by around 80 bps. (vi) Fiscal Slippage The Central Government’s fiscal deficit for 2017-18 and 2018-19 is likely to be above initial expectations and the medium-term adjustment path has also been postponed. An empirical assessment presented in the MPR of October 2017 suggests that: (a) in India, causality runs from fiscal deficits to inflation; and (b) the impact of fiscal deficits on inflation is non-linear, i.e., higher the initial levels of the fiscal deficit and inflation, higher is the impact of an increase in the fiscal deficit on inflation. Given the present levels of the combined (centre and states) fiscal deficit, an increase in the fiscal deficit to GDP ratio by 100 bps could lead to an increase of about 50 bps in inflation. Apart from its direct impact on inflation, fiscal slippage has broader macro-financial implications, notably on economy-wide costs of borrowing which have already started to rise. These may feed into inflation and elevate it further. I.4 Conclusion To summarise, aggregate demand is expected to improve in 2018-19, supported, inter alia, by the improving GST implementation, the recapitalisation of public sector banks and the resolution of distressed assets under the IBC. Rural and infrastructure sectors are identified as thrust areas in the Union Budget, which could energise aggregate demand. With the acceleration in global trade, the Indian economy could benefit from buoyant external demand. In addition to the usual monsoon related uncertainty, inflation faces upside risks from a variety of other sources, especially due to the oil prices, the fiscal slippage, and (the statistical effect from) the expected increases in HRAs by the state governments, The purely direct statistical impact of the HRA adjustment on CPI will be looked through while formulating monetary policy. Uncertainty over the pace and timing of monetary policy normalisation by the systemic central banks in advanced economies, protectionist tendencies and fears of a trade war pose significant risks to the baseline inflation and growth paths.

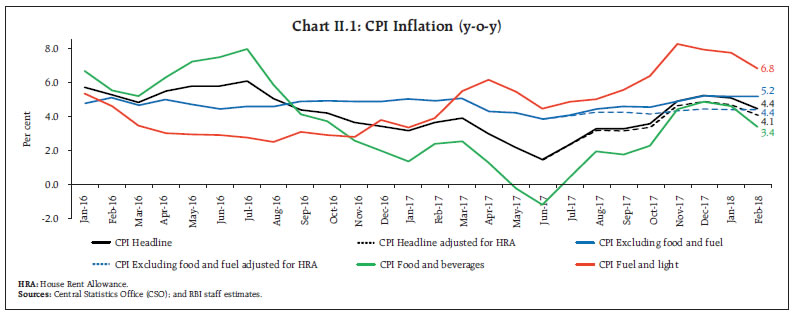

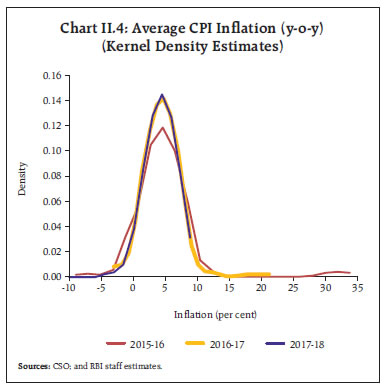

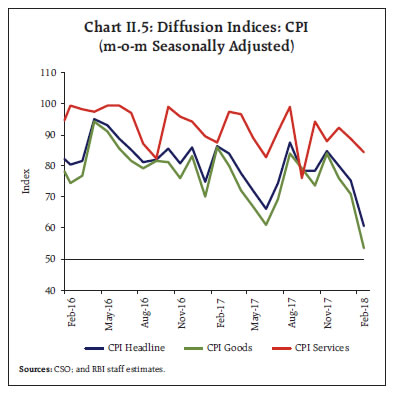

II. Prices and Costs Consumer price inflation rose sharply in Q3:2017-18, driven up by a spike in food prices and by the disbursement of enhanced house rent allowance (HRA) for central government employees, the latter alone contributing an estimated 35 basis points. It moderated somewhat in Q4 on a delayed seasonal easing of prices of vegetables. Industrial input costs increased through H2:2017-18, tracking movements in international commodity prices. Wage pressures have remained moderate in both the organised and rural sectors. The course of consumer price index (CPI) inflation in Q3 was significantly influenced by house rent allowance (HRA) increase for central government employees from July 2017, following the recommendations of the 7th central pay commission (CPC).1 The HRA impact contributed 35 basis points to the rise in headline inflation to its recent peak of 5.2 per cent in December, following the chain base method of compilation of the housing index in the CPI.2 Adjusted for the estimated HRA impact, headline inflation was 4.9 per cent in December. The HRA impact on inflation excluding food and fuel was even larger at around 75 basis points, adjusting for which it would have been lower at 4.4 per cent in December. Food inflation rose sharply in Q3 pushed by the unseasonal pick-up in prices of vegetables; and fuel inflation accelerated due to an uptick in inflation in liquefied petroleum gas (LPG), kerosene, coke and electricity. In Q4, headline inflation eased to 4.4 per cent by February 2018 with the seasonal softening in prices of vegetables. Excluding the HRA impact, headline inflation was 4.1 per cent and inflation excluding food and fuel remained unchanged at 4.4 per cent (Chart II.1). The MPR of October 2017 had projected CPI inflation to increase to 4.2 per cent in Q3 of 2017-18 and further to 4.6 per cent in Q4, based on a prognosis of unfavourable base effects and the play-out of the increase in HRA for central government employees. Actual inflation outcomes in Q3 were in alignment with the direction of the projected trajectory, but in levels, they turned out to be 35 basis points higher than forecast due to a combination of shocks. First, an unseasonal spike in the prices of onions and tomatoes during October-November 2017 caused prices of vegetables to soar, propelling inflation in this category to close to 30 per cent in December. Second, fuel inflation rose sharply during October-November on the back of an escalation in LPG prices. Third, international crude oil prices started firming up further from October. By end-December 2017, they were US$ 10 per barrel above the baseline assumption of US$ 55 per barrel. The pass-through to CPI inflation was, however, muted in Q3 due to excise duty cuts in early October and lagged mark-ups by oil marketing companies (OMCs). In Q4, most of the factors imposing these upward price pressures reversed. The winter downturn in prices of vegetables accentuated in January. Domestic LPG prices also eased in February, tracking international prices. As a result, the deviation between the actual and the projected inflation narrowed in Q4 to 15 bps (Chart II.2).  II.1 Consumer Prices The increase in HRA for central government employees, which became effective from July 2017 and continued to accumulate till December 2017, shaped the path of headline inflation during Q3, with unseasonal hardening of prices of vegetables, accentuating a spike to 4.9 per cent in November. While prices of vegetables did undergo a shallower than usual moderation in December, an unfavourable base effect came into play, pulling up inflation to a peak of 5.2 per cent in December. In Q4, headline inflation moderated with a fall in momentum due to a delayed but steep reversal in prices of vegetables (Chart II.3). The distribution of inflation across CPI groups in 2017-18 had striking similarities as well as divergences with last year’s experience. While median and modal inflation were similar, the continuing deflation in pulses gave the inflation distribution a considerable negative skew this year in contrast to the positive skew generated by high sugar and pulses inflation during 2016-17 (Chart II.4). Diffusion indices3 of price changes in CPI items suggest that on a seasonally adjusted basis, after an uptick in Q3:2017-18, the situation reversed in January-February, with the prices of a number of goods, particularly of food items, registering decline (Chart II.5).

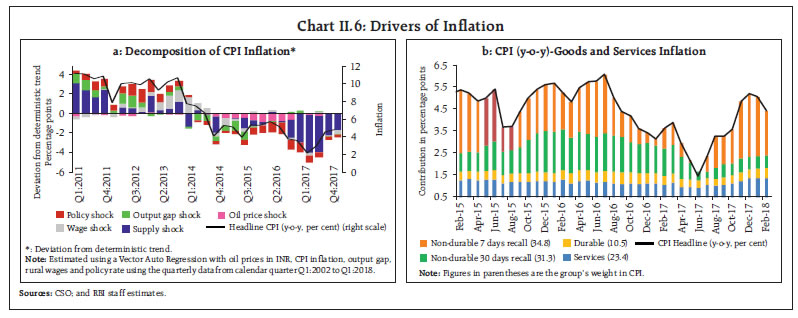

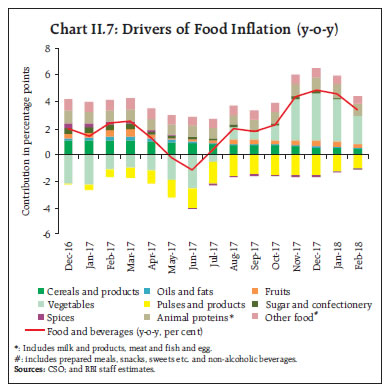

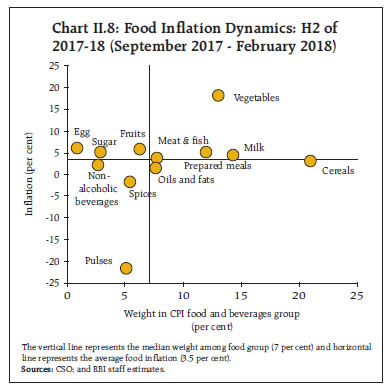

II.2 Drivers of Inflation A historical decomposition4 of inflation shows that the persistent effect of favourable supply shocks, especially on food prices, provided a cushion in the first half of 2017-18. However, the positive supply shocks waned in the second half of the year vis-á-vis the first half. The lagged impact of the still negative output gap and moderation in nominal rural wages also contributed to lower inflation during this period, while the firming up of crude oil prices imparted upward pressure (Chart II.6a).  Decomposing inflation into its goods and services components reveals that the pick-up in inflation from June to December 2017 and its reversal from January 2018 largely emanated from prices of non-durables, particularly perishables; while those of services registered a sustained increase, primarily due to increase in housing inflation from 4.7 per cent in June to 8.2 per cent in December and further to 8.4 per cent in February, reflecting the statistical effect of the HRA (Chart II.6b). Housing alone contributed over 90 per cent of the observed increase in services inflation during this period.  Turning to the drivers of food inflation in the second half of the year, the food and beverages sub-group contributed around 40 per cent to overall inflation, up from just 12 per cent during the first half. Adequate buffer stocks kept inflation in cereals generally under check. With cereals inflation under check, the pick-up in food inflation was largely on account of prices of vegetables – specifically tomato and onion – and intermittent uptick in prices of animal protein-rich food items. Continued decline in prices of pulses exerted a strong downward pull. Inflation in processed food products also moderated due to, inter alia, downward revision in GST rates (Charts II.7 and II.8).

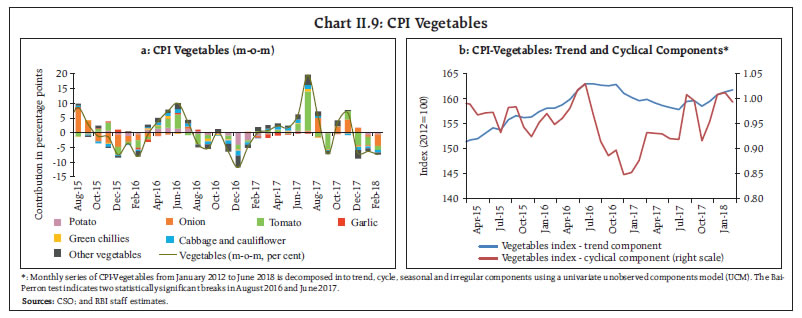

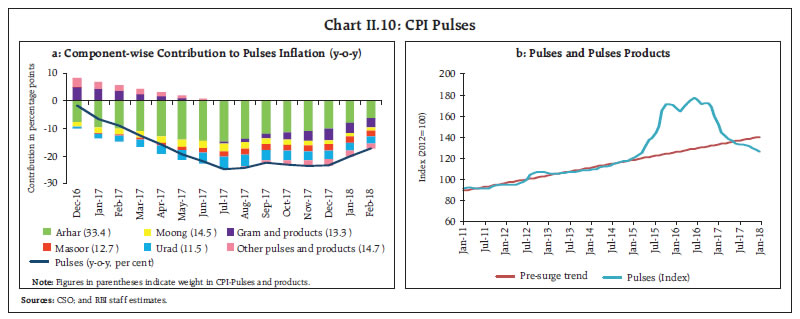

Vegetables, which account for 13 per cent of the food group in CPI, were the principal drivers of food inflation. Price pressures in vegetables started building up from June 2017 following a fall in mandi arrivals, especially in onions and tomatoes (Chart II.9a). In the case of tomatoes, the upsurge in prices was so sharp that inflation in this category went up from (-)41 per cent in June 2017 to 119 per cent in November 2017 due to supply disruptions caused by adverse weather conditions – high temporal and spatial variability and delayed withdrawal of monsoon – and farmers’ agitation in parts of Maharashtra and Madhya Pradesh. While tomato prices recorded some contraction during August-September, the extended South-West monsoon in October in several important tomato-producing centres, especially in states like Karnataka, Andhra Pradesh, Telengana, Madhya Pradesh and Odisha, led to severe crop losses and tomato prices shot up again in November.  Another driver was the inflation in onions, which rose from (-)14 per cent in April 2017 to 159 per cent in December. Again, while unfavourable weather was a factor, large procurement of onions by a few state governments was the principal cause of the price spike. Post-November 2017, onion and tomato prices plunged with the arrival of fresh winter crops. Supply management measures by the government, especially in case of onions, helped in easing prices. The minimum export price (MEP), which is the key supply management measure used by the government to contain onion price surges, was re-implemented during the year in November and set at US$ 850 per tonne. The State-owned canalising agency viz., Metals and Minerals Trading Corporation of India (MMTC), imported 2,000 tonnes of onions, while other agencies such as National Agricultural Cooperative Marketing Federation of India (NAFED) procured around 10,000 tonnes of onions directly from the farmers, and the Small Farmers’ Agri-Business Consortium (SFAC) bought around 2,000 tonnes of onions locally and supplied to the consumers. The central government also advised states to take measures by way of licensing, imposition of stock limits and movement restrictions to balance supplies. In response, onion prices softened and the government brought down the MEP to US$ 700 per tonne in January 2018 before withdrawing it completely in February 2018.  In case of potatoes, delayed sowing in West Bengal – a key growing state – due to extended monsoon showers in October, induced price pressures. However, carry-over stocks from the previous crop reined them in. Analysis based on CPI data suggests that there is no significant difference in the m-o-m changes of prices of vegetables in urban and rural areas – the spike in prices of vegetables uniformly impacted rural and urban India5. Most of the demonetisation-induced fall in prices of vegetables reversed as is evident from the trend and cyclical components of CPI-Vegetables (Chart II.9b). The other food components that recorded uptick in prices, albeit unevenly, were protein-rich items such as egg, meat and fish. Inflation in egg prices jumped from 0.8 per cent in October to 9.3 per cent in December, pushed up by tighter supply conditions on account of reduced egg production by poultry farms at the time of the usual increase in winter demand. Pulses, with a weight of 5 per cent in the food group, contributed significantly to food inflation dynamics during the year. The contribution of pulses to overall inflation shifted from 6.0 per cent during 2016-17 to (-)19.0 per cent in 2017-18. At a granular level, the contribution of arhar in overall pulses inflation declined consistently from July 2017, while the contribution of gram prices, turned increasingly negative month after month till December 2017. With the production for pulses during 2017-18, as per the second advanced estimates, being marginally higher at 23.95 million tonnes (23.13 million tonnes in 2016-17), pulses prices have now fallen significantly below trend levels (Charts II.10a & b).

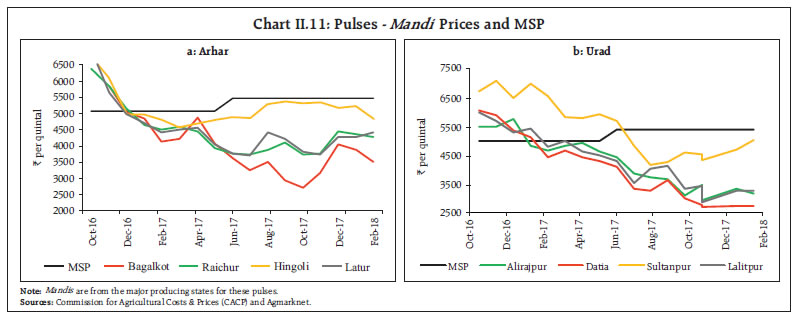

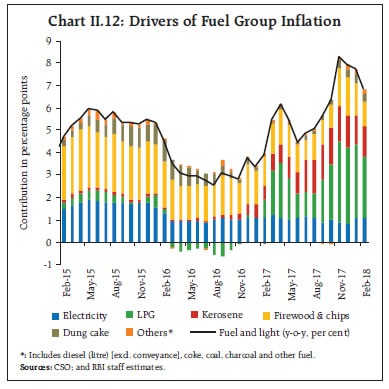

Arhar and urad prices remain below their minimum support prices (MSPs) at the mandi level in the major producing states viz., Maharashtra, Madhya Pradesh, Gujarat, Uttar Pradesh and Karnataka reflecting the large gap in procurement relative to supply (Chart II.11). Corrective measures were initiated by the government during the course of the year such as removal of export ban on all pulses and an imposition of 60 per cent import duty on gram and 30 per cent import duty on masoor in order to support prices and provide some relief to farmers. Sugar and spices are the other items which played an important role in the overall moderation of food inflation. Inflation in sugar and confectionery, which was in double digits all through 2016-17 (averaging about 20 per cent), declined significantly during the year, largely due to measures facilitating imports and on expectations of higher domestic production (the sugarcane production for 2017-18, as per the second advanced estimates, is 353.2 million tonnes as against 306.1 million tonnes in 2016-17). With sugar prices easing rapidly, however, the central government has again raised the import duty on sugar to 100 per cent and re-imposed stockholding limits on sugar sales for February and March 2018. Prices of spices have moved into deflation since June 2017 on account of a fall in prices of dry chillies, turmeric, dhania, and black pepper. Fuel and light inflation, which was at 5.0 per cent in August 2017, touched 8.2 per cent in November 2017, the highest since September 2013 (Chart II.12) largely on account of a sustained increase in domestic prices of LPG – tracking rising international product prices – as well as due to rural fuel consumption items such as dung cake. Since the migration of subsidy payments on LPG to banks under the direct benefit transfer scheme, LPG prices track international prices closely. Administered kerosene also registered sustained price increases as OMCs raised prices in a calibrated manner. Fuel and light inflation since December has eased driven by the downturn in LPG inflation, reflecting international price movements, as well as on account of moderation in firewood and chips and dung cake inflation.

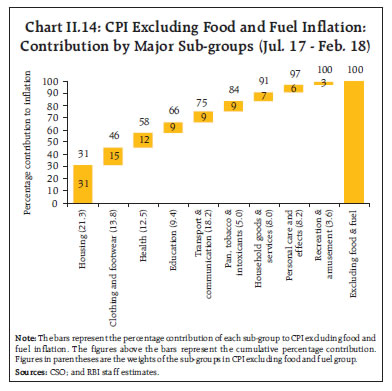

Turning to the underlying inflation dynamics, CPI inflation excluding food and fuel edged up from the June 2017 trough of 3.8 per cent to 5.2 per cent in December and remained at that level during January- February 2018 – an increase of around 130 basis points between June and February (Chart II.13). The substantial increase largely reflected an increase in housing inflation (Chart II.14). Netting out the HRA impact, CPI inflation excluding food and fuel would have been 4.4 per cent – around 75 basis points lower than the observed print – during December 2017 to February 2018. Inflation in CPI excluding food and fuel, as also petrol and diesel, increased from June 2017 by 140 basis points to 5.3 per cent in February 2018. While the HRA impact explained much of this increase, petrol and diesel initially in Q3, had a dampening effect as much of the pass-through of surge in international crude oil price to domestic prices was delayed to the second half of January 2018. Furthermore, the excise duty cuts in early October 2017 by ₹2 per litre each for petrol and diesel also helped cushion the incremental impact of rising international crude prices (Chart II.15). Further, excluding the four volatile items – petrol, diesel, gold and silver – and housing, the inflation in February was 70 basis points lower at 4.4 per cent, and reflected the underlying inflation momentum in the second half of 2017-18.  In H2:2017-18, both goods and services in CPI excluding food and fuel exhibited a rising inflation trajectory, notwithstanding some softening in case of goods in the recent months. For goods, inflation picked up across commodity groups: medicines under the health sub-group; clothing and footwear; pan, tobacco and intoxicants; and gold under the personal care and effects sub-group (Chart II.16a). Services inflation increased by 177 basis points over June (Chart II.16b), driven by housing sub-group due to the release of HRA from July 2017 under the recommendations of the 7th CPC. The contribution of transport services also edged up in recent months, as fuel prices were transmitted to increase in transportation fares. In contrast, communication services inflation has remained muted due to low cellular services inflation.

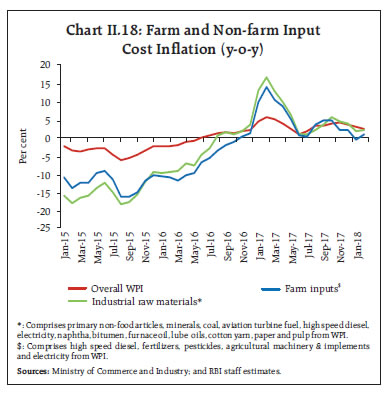

Other Measures of Inflation Measures of inflation other than CPI remained moderate in Q3 and Q4:2017-18. Inflation in wholesale price index (WPI) that does not include services, the CPI for rural labourers (RL) and the agricultural labourers (AL), which do not have housing components, moved in tandem with headline CPI up to October. The gap between inflation in terms of the CPI for industrial workers (CPI-IW) and the headline CPI, which was wide since July 2017 after HRA was implemented, closed in January 2018. CPI-IW adjusts its housing index only twice a year – in January and July. Thus, the HRA impact was reflected only in January 2018. GDP and GVA deflators also remained lower than CPI in Q3 (Chart II.17a). After the June 2017 trough, inflation measured by trimmed means in the CPI hardened for the rest of 2017. Thereafter, all trimmed means, including the weighted median, edged down, reflecting, inter alia, the broad-based softening of food prices (Chart II.17b). II.3 Costs Underlying cost conditions have mostly co-moved with measures of inflation, ticking up in H2:2017-18, notwithstanding some moderation in Q4. Y-o-y growth in farm input costs slipped temporarily into negative territory in January 2018 (Chart II.18). The rise in global crude oil prices and the hardening of metal prices fuelled the rise in input costs from August 2017 onwards and contributed to the turnaround in domestic non-farm input costs as they got passed on to inputs such as high speed diesel, aviation turbine fuel, naptha, bitumen, furnace oil and lube oils. Among other industrial raw materials, domestic coal inflation generally remained high during the year, tracking the surge in international coal prices and domestic supply shortages. However, inflation in other inputs depicted a mixed behaviour. In the case of oilseeds, inflation picked up during H2:2017-18, whereas in the case of fibres and paper and pulp, inflation moderated during the same period. Inflation in electricity, which carries a high weight in both industrial and farm inputs, rose during September-October 2017, but turned negative thereafter. Among other farm sector inputs, diesel prices increased sharply from August 2017, mirroring international prices, while prices of inputs such as tractors and fodder increased sharply in February 2018 after contracting in the preceding months. Fertiliser prices also recorded some upward pressure during December-February.

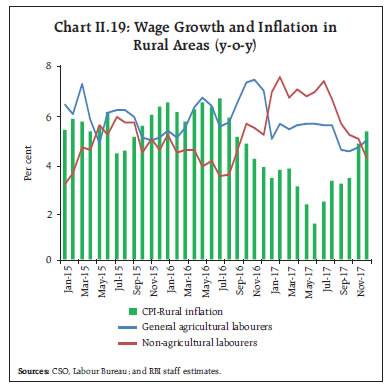

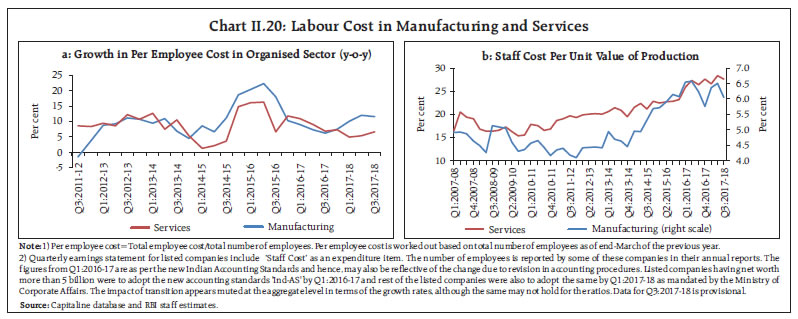

Growth in rural wages largely moderated since August 2017 (Chart II.19). In general, nominal rural wages and inflation tend to move together. However, large supply shocks have caused a divergence between the two in the recent period (Box II.1). Staff costs in the organised manufacturing sector rose between Q3:2016-17 and Q2:2017-18, but moderated during Q3:2017-18. The y-o-y growth in per employee cost for the manufacturing sector moderated to 11.6 per cent during Q3:2017-18. Staff costs in the services sector continued to decelerate from Q4:2015-16 till Q1:2017-18 and rose thereafter to 6.6 per cent in Q3:2017-18 (Chart II.20). Based on responses of manufacturing firms covered in the Reserve Bank’s industrial outlook survey, the cost of raw materials is assessed to increase significantly in Q4:2017-18 in relation to the previous quarter. Firms expect the cost of raw materials to rise further in Q1:2018-19, and pass them on to selling prices due to pressure on their margins. The manufacturing purchasing managers’ index (PMI) suggests that input costs accelerated in the second half of 2017-18, registering their highest level in February in the past 12 months before edging down in March. The co-movement of output prices with input prices suggests that pricing power is returning. In PMI services, there was a sharp acceleration in input prices in Q3, with the input services price index reaching its highest level of 55.0 since October 2013. The prices of services continued to increase in Q3 and Q4, though its momentum moderated with the downward revision in GST rates for many services.

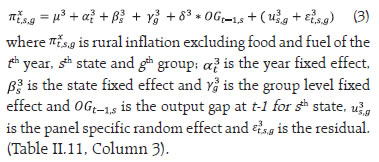

Box II.1: Relationship among Rural Wages, Inflation and Economic Activity: Recent Evidence Rural wages and inflation have moderated since early 2015, but with considerable divergence in their trajectories, particularly since July 2016 (Chart II.19). Historically, nominal wage growth and inflation tended to move together with inflation generally leading nominal wage growth, though with a slow speed of adjustment to disturbances (Kundu, 2018). An important issue that arises in this context is whether evolving economic activity has affected rural wages and inflation differently. Drawing on Knotek et al. (2014), two different Phillips curve specifications were estimated and compared to understand the differential impact of the output gap on rural wage growth and rural inflation. In the first specification, a wage Phillips curve with rural wage inflation as the dependent variable and economic activity measured by output gap (OG)6 as the independent variable was estimated: The second specification consisted of a price Phillips curve with CPI rural price inflation as the dependent variable and economic activity measured by OG as the independent variable: Both specifications were estimated for the period 2015 to 2017 for 15 major states. In the case of the rural wage Phillips curve, nine occupations7 were considered, while the CPI-Rural inflation Phillips curve was estimated with five major groups8. The regression results (Table II.1.1: Columns 1 and 2) show that while the rural wage Phillips curve holds for the recent period, i.e., economic activity is able to explain wage inflation, the price Phillips curve does not hold, i.e. economic activity is not able to explain CPI-Rural inflation9. However, in order to further analyse whether the price Phillips curve holds for a measure of underlying inflation rather than the overall inflation, which is often subject to large supply shocks from food and fuel prices, an alternate specification with CPI-Rural inflation excluding food and fuel as the dependent variable was also estimated:

| Table II.1.1: Empirical Phillips curves | | Independent Variables | Dependent Variable | | Wage Inflation | CPI-Rural Inflation | CPI-Rural Excluding Food and Fuel Inflation | | (1) | (2) | (3) | | OG(-1) | 0.2709 | 0.0860 | 0.2712 | | | (0.052) | (0.436) | (0.007) | | State fixed effects | Yes | Yes | Yes | | Time fixed effects | Yes | Yes | Yes | | Group fixed effects | Yes | Yes | Yes | | No. of observations | 405 | 225 | 135 | Note: p-values in brackets.

Hausman test and Breusch and Pagan Lagrangian multiplier test suggest a random effect model. Regression equations are estimated using generalised least squares regression with AR(1) disturbances to overcome the presence of autocorrelation. Pesaran’s cross-sectional dependence test suggests that residuals are uncorrelated across panels. | In this case, OG is found to be statistically significant and of broadly the same magnitude as in the wage Phillips curve. Taken together, these results suggest that economic activity is a significant determinant of movements in both rural wages and CPI-Rural excluding food fuel inflation but not the overall CPI-Rural inflation (which includes both food and fuel). Rural food inflation since 2015 gyrated in a wide range of (-)0.8 per cent to 7.9 per cent, pointing to the outsized role of supply side shocks in driving recent food inflation trajectory that masks the underlying association between prices and economic activity. In other words, the recent divergence in rural wage growth and inflation could be explained by large supply side shocks affecting rural food inflation (Chart II.6a). References: Behera, H., Wahi, G., & Kapur, M. (2017), ';Phillips Curve Relationship in India: Evidence from State-Level Analysis';, RBI Working Paper Series No. 08/2017. Knotek II, E. S., & Zaman, S. (2014), ';On the Relationships between Wages, Prices, and Economic Activity';, Economic Commentary, Federal Reserve Bank of Cleveland, August. Kundu, S. (2018), ';Rural Wage Dynamics in India: What Role does Inflation Play?';, mimeo. | II.4 Conclusion Going forward, a key risk to the inflation outlook is the risk of fiscal slippages in a scenario of rising aggregate demand. As noted in the MPC resolution of February 2018, apart from the direct impact on inflation, the fiscal risks could also engender a broader weakening of macro-financial conditions. The revised guidelines for arriving at the MSPs for kharif crops proposed in the Union Budget 2018-19, along with proposed increase in customs duty on a number of items, is likely to push-up inflation over the year. In addition, how various state governments implement and disburse HRA increases would have a considerable bearing on CPI housing inflation and consequently on the headline inflation trajectory, albeit statistically, during 2018-19; therefore, the latter should be looked through for monetary policy purposes, other than for their second-round effects. Although the central government's HRA effects on CPI inflation would gradually wane from July 2018, this moderating impact could be more than offset if several state governments simultaneously implement HRA increases in H2:2018-19 (Chapter 1).

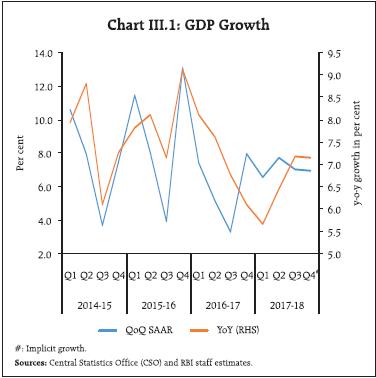

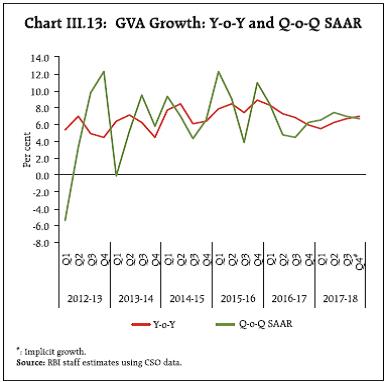

III. Demand and Output Aggregate demand growth accelerated in H2:2017-18, supported mainly by an investment upturn, while consumption remained resilient. Aggregate supply conditions were buoyed by the robust performance of the manufacturing sector and the improvement in activity in the agriculture and services sectors. Domestic economic activity shrugged off the loss of speed that had characterised the period Q1:2016-17 to Q1:2017-18 and a turning point appears to have taken hold in Q2-Q3, with lead indicators pointing to further acceleration in Q4. In terms of aggregate demand, the drivers around this inflexion are shifting, with consumption-led growth of the recent past handing over the baton to investment, which had restrained growth since Q3:2016-17. At the same time, the strong impetus from fiscal spending during Q3:2016-17 to Q1:2017-18 appears to be waning and the rapid pace of import growth is sapping net external demand. On the supply side, the pickup in industrial output from Q2:2017-18 and the strengthening of construction activity in the services sector from Q1 are noteworthy. Meanwhile, agriculture and allied activities have turned out to be resilient to temporary weather disruptions in both kharif and rabi sowing seasons and going by recent estimates of foodgrains production, the outlook appears better than before. III.1 Aggregate Demand Aggregate demand appears to have regained traction in H2:2017-18 after a prolonged slackening that stretched up to a 13-quarter low in Q1:2017-18. Measured by y-o-y changes in real GDP at market prices, it accelerated to 7.2 per cent in H2:2017-18 from 6.1 per cent in the preceding half of the year and 6.4 per cent a year ago. The turnaround in Q2:2017-18 and the steady gathering of speed thereafter are largely benefitting from a favourable base effect – a low base level a year ago – rather than a quickening of momentum, since q-o-q seasonally adjusted annualised growth rate (SAAR) slowed in Q3 and flattened in Q4 (Chart III.1). For the year 2017-18 as a whole, however, the second advance estimates (February 2018) of the Central Statistics Office (CSO) indicate that the pace of expansion of aggregate demand is still slower than in the preceding year.  Turning to the underlying drivers, there are small but noteworthy shifts underway. In terms of weighted contributions, the support to aggregate demand from private consumption is waning, supplanted by the burgeoning strength of capital formation after a prolonged hiatus (Table III.1). This is significant since the historical experience has been that changes in capital accumulation are associated with level and/or slope shifts in India’s growth cycle. A surge in imports led to a higher negative contribution of net exports, which dragged down the overall demand. These developments are discussed in detail in the rest of this chapter. | Table III.1: Real GDP Growth | | (Per cent) | | Item | 2016-17 (FRE) | 2017-18 (SAE) | Weighted Contribution* | 2016-17 (FRE) | 2017-18 (SAE) | | 2016-17 | 2017-18 | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4# | | Private Final Consumption Expenditure | 7.3 | 6.1 | 4.1 | 3.4 | 8.3 | 7.5 | 9.3 | 4.2 | 6.6 | 6.6 | 5.6 | 5.6 | | Government Final Consumption Expenditure | 12.2 | 10.9 | 1.2 | 1.1 | 8.3 | 8.2 | 12.3 | 22.5 | 17.1 | 2.9 | 6.1 | 19.6 | | Gross Fixed Capital Formation | 10.1 | 7.6 | 3.1 | 2.4 | 15.9 | 10.5 | 8.7 | 6.0 | 1.6 | 6.9 | 12.0 | 9.9 | | Net Exports | – | – | 0.1 | -1.2 | – | – | – | – | – | – | – | – | | Exports | 5.0 | 4.4 | 1.0 | 0.9 | 3.6 | 2.4 | 6.7 | 7.0 | 5.9 | 6.5 | 2.5 | 3.0 | | Imports | 4.0 | 9.9 | 0.9 | 2.1 | 0.1 | -0.4 | 10.1 | 6.6 | 16.0 | 5.4 | 8.7 | 10.0 | | GDP at Market Prices | 7.1 | 6.6 | 7.1 | 6.6 | 8.1 | 7.6 | 6.8 | 6.1 | 5.7 | 6.5 | 7.2 | 7.1 | FRE: First Revised Estimates; SAE: Second Advance Estimates; #: Implicit growth.

*: Component-wise contributions to growth do not add up to GDP growth in this table because changes in stocks, valuables and discrepancies are not included.

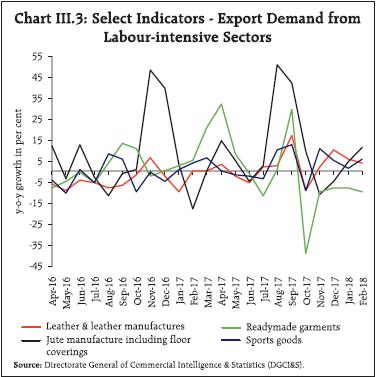

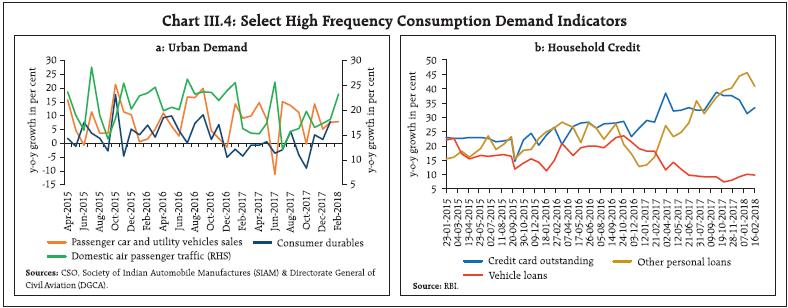

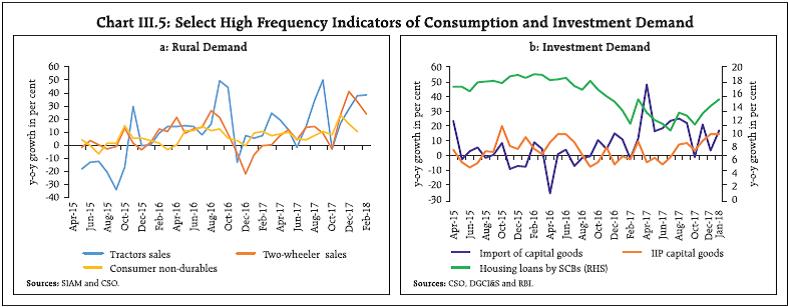

Source: Central Statistics Office (CSO). | III.1.1 Private Final Consumption Expenditure Private final consumption expenditure (PFCE) constituted 56.6 per cent of domestic demand in H2:2017-18, down from 57.5 per cent a year ago (Chart III.2). Short-term adverse effects of demonetisation and the implementation of the GST have taken their toll on output and employment in the unorganised sector, most vividly reflected in significant slowdown in exports of labour-intensive goods such as leather goods, textiles, jute manufactures, readymade garments. and sports goods (Chart III.3). Rise in global crude oil prices also appears to have contributed to the slowdown in private consumption.  High frequency indicators of urban consumption present a mixed picture. While consumer durables production remained subdued during the larger part of 2017-18, domestic air passenger traffic, and passenger cars and utility vehicles sales showed robust growth (Chart III.4a). Going forward, urban consumption is expected to strengthen with the likely implementation of the award on salaries and allowances at the level of states and other public sector entities. A sharp growth in personal loan portfolios of commercial banks and the recent pick-up in vehicle loans also augur well for urban consumption (Chart III.4b). The turnaround in construction activity – an employment-intensive sector in H2:2017-18 (as detailed later in the chapter) should support rural consumption. Indicators of rural demand, viz., growth in sales of two-wheelers and tractors remained strong, particularly from Q2. The production of consumer non-durables has also recovered markedly (Chart III.5a).

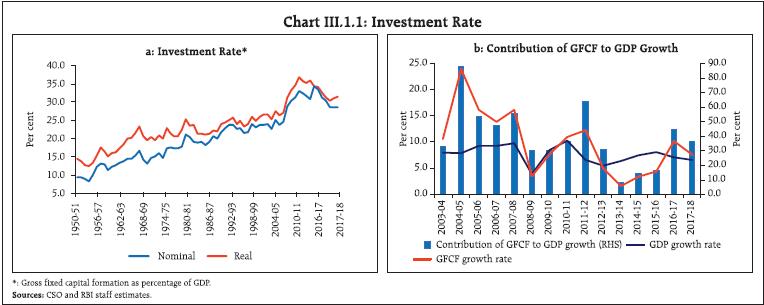

III.1.2 Gross Fixed Capital Formation A stark feature of India’s recent growth experience has been the protracted downturn in investment, however, a turnaround set in during Q2:2017-18. Gross fixed capital formation (GFCF) strengthened further to touch a six-quarter high in Q3. The share of gross fixed capital formation in GDP, which was trapped in a downturn from a high of 34.3 per cent in 2011-12 to 30.3 per cent in 2015-16, broke free and increased to 31.4 per cent in 2017-18. As alluded to earlier, this pick-up in the investment rate could be signalling a turning point in the cyclical component of growth oscillations in India and if sustained by a determined policy push, it could produce a level shift in the trajectory of the Indian economy (Box III.1). Capital goods production – a key element of investment demand – turned around in August 2017 and clocked a 19-month high in terms of growth rates in January 2018 (Chart III.5b). During 2017-18 so far (up to December), the construction of highway projects is on the rise and is expected to have improved further in Q4.

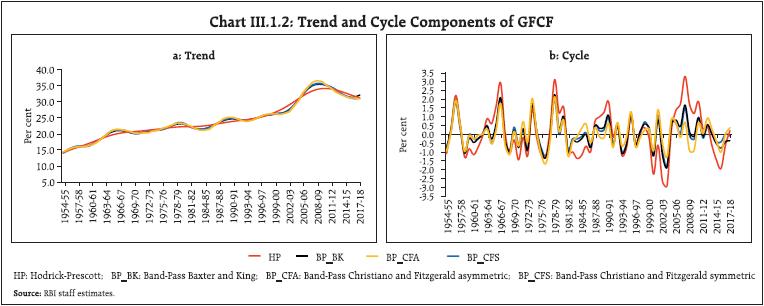

Box III.1: India’s Investment Cycle - Is It Turning? The slowdown in India’s growth over the past two years and the coincident slump in capital formation has generated significant concerns. The investment rate in real terms has slowed down after 2010-11 (Chart III.1.1a). With real GFCF growing at a slower rate, its contribution to real GDP growth declined from 44.4 per cent in 2016-17 to 36.1 per cent in 2017-18 (Chart III.1.1b). As changes in the rate of investment have been historically associated with turning points in the growth path, the trend and cyclical components of the investment rate and its duration of cycle were estimated by applying Hodrick-Prescott (HP) and Band-Pass (BP) filters. While there has been a moderation in the trend component of the investment rate since 2010-11, the cyclical component has shown an upward movement from the year 2016-17, suggesting that the recent improvement in investment activity is largely driven by cyclical factors (Chart III.1.2).

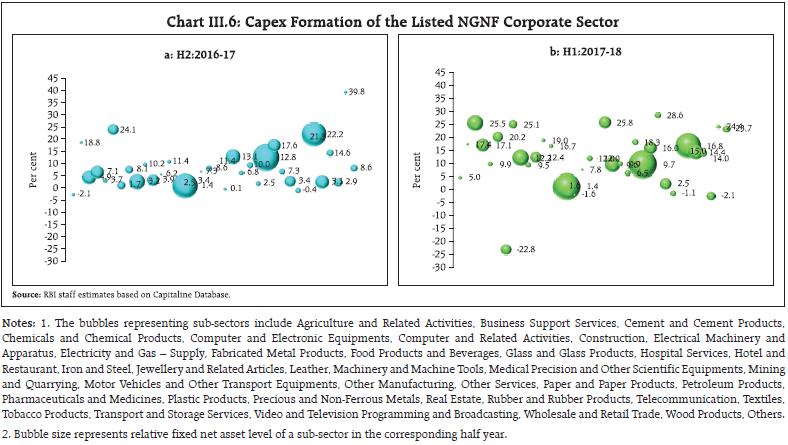

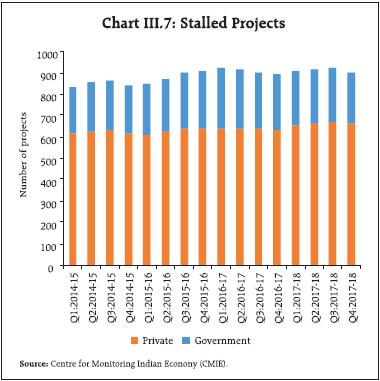

While there are two broad approaches for the measurement of business cycles, viz., the dating procedure and the production function approach, the first one is preferred and widely used in view of inherent problems associated with measurement of technology shocks through a production function framework. In this context, the business cycle and the growth cycle approaches developed by the National Bureau of Economic Research (NBER) are commonly used for the dating procedure. In the first method (Burns and Mitchell, 1946), the business cycle is measured by absolute changes in the general level of production in two steps: (i) identification of cyclical peaks and troughs in the observed economic variables; and (ii) determining whether these changes are common across all the observed series. In the second approach, a growth cycle is defined as the ups and downs in the deviations of the actual growth rate of the economy from the long-run trend growth rate (Zarnowitz, 1992). | Table III.1.1: Duration of Investment Cycle | | Cycle Reference Year | Duration (in Years) | | Peak | Trough | Contraction | Expansion | Cycle | | Peak to Trough | Previous Trough to this Peak | Trough from previous Trough | Peak from previous Peak | | - | 1950-51 | - | - | - | - | | 1951-52 | 1953-54 | 2 | 1 | 3 | - | | 1956-57 | 1958-59 | 2 | 3 | 5 | 5 | | 1959-60 | 1960-61 | 1 | 1 | 2 | 3 | | 1963-64 | 1964-65 | 1 | 3 | 4 | 4 | | 1966-67 | 1968-69 | 2 | 2 | 4 | 3 | | 1969-70 | 1970-71 | 1 | 1 | 2 | 3 | | 1971-72 | 1972-73 | 1 | 1 | 2 | 2 | | 1973-74 | 1976-77 | 1 | 1 | 2 | 2 | | 1978-79 | 1979-80 | 1 | 2 | 3 | 3 | | 1980-81 | 1981-82 | 1 | 1 | 2 | 2 | | 1982-83 | 1983-84 | 1 | 3 | 4 | 4 | | 1985-86 | 1986-87 | 1 | 2 | 3 | 3 | | 1987-88 | 1989-90 | 1 | 1 | 2 | 2 | | 1990-91 | 1991-92 | 1 | 1 | 2 | 2 | | 1992-93 | 1993-94 | 1 | 1 | 2 | 2 | | 1995-96 | 1996-97 | 1 | 2 | 3 | 3 | | 1999-00 | 2000-01 | 1 | 3 | 4 | 4 | | 2001-02 | 2003-04 | 2 | 2 | 4 | 3 | | 2004-05 | 2006-07 | 2 | 1 | 3 | 3 | | 2007-08 | 2009-10 | 2 | 1 | 3 | 3 | | 2010-11 | 2011-12 | 1 | 1 | 2 | 3 | | 2012-13 | 2015-16 | 3 | 1 | 4 | 2 | | 2017-18 | - | - | 2 | 2 | 5 | | Average | 1.4 | 1.6 | 3.0 | 3.0 | | Source: RBI staff estimates. | As the real GFCF rate has declined in levels on many occasions during the post-1950 period, identification of cyclical peaks and troughs in the observed levels of the economic variables based on the business cycle methodology, which is followed by NBER, is more suitable than the growth rate approach. For the purpose of measurement of the duration of investment cycle, the cyclical factor measured by Christiano and Fitzgerald asymmetric Band-Pass filter was used as it assigns variable weights and does not exclude end points. Following the business cycle approach of the NBER, it is observed that investment rate in India has gone through cycles of three-year (Table III.1.1). These results, when extrapolated, suggest that the upturn in the investment rate that commenced in Q3:2016-17 has approximately nine more quarters to fully play out. Policy efforts such as improving ease of doing business, speedy resolution of corporate distress, quickly addressing the remaining issues relating to the implementation of the Goods and Services Tax (GST) and speeding up of the stalled projects, among others, will help ride this phase of the investment cycle to its peak and produce accelerating impulses for the growth trajectory. Timely and measured interventions hold the key to realise the investment-led growth. References: Burns, A.F. and W.C. Mitchell (1946), Measuring Business Cycles, National Bureau of Economic Research, New York. Raj, Janak, Satyananda Sahoo and Shiv Shankar (2018), “India’s Investment Cycle – Is It Turning?”, Mimeo. Zarnowitz, V. (1992), Business Cycles Theory, History, Indicators and Forecasting, University of Chicago Press. | Corporate financial results are also mirroring these underlying shifts. The results of listed nongovernment non-financial (NGNF) companies suggest that manufacturing companies reduced current assets and increased fixed assets in H1:2017-18 vis-à-vis a year ago, possibly pointing to the long-awaited revival in the capex cycle. Nominal capex growth across 38 sub-sectors covering industrial and services sectors underwent a broad-based recovery in H1:2017-18 vis-à-vis H2:2016-17 (Charts III.6a and III.6b). A sharp pick-up in housing loans by scheduled commercial banks also augurs well for investment in dwellings. The implementation of stalled projects showed modest improvement (Chart III.7).

Based on the CSO’s second advance estimates, gross fixed capital formation grew by 7.6 per cent in 2017-18 on top of 10.1 per cent in 2016-17. Seasonally adjusted capacity utilisation [CU(SA)], which remained below average since Q1:2013-14 due to overhang of excess capacity created during 2009-14, exhibited noticeable pick-up in Q3:2017-18 (Chart III.8). Going forward, large resource mobilisation from the primary capital market and accelerating non-food credit growth (Chapter IV) indicate that investment activity could strengthen further if fiscal pre-emptions do not crowd out private investment demand. III.1.3 Government Expenditure Government final consumption expenditure (GFCE) provided sustained support to aggregate demand in H2:2017-18, picking up in Q3:2017-18 on top of the front-loading of expenditure by the central government in Q1:2017-18. GFCE will likely continue to augment aggregate demand going forward into 2018-19, in view of the deviation of 0.3 per cent of GDP from the path of fiscal consolidation announced in the Union Budget (Table III.2). The gross fiscal deficit (GFD) target of 3.0 per cent of GDP has been deferred to 2020-21. In 2017-18 (April-February), there was a deterioration in the fiscal position of the central government on account of a sharp increase in expenditure combined with a decline in non-tax revenue relative to budget estimates. Revenue expenditure has evolved as budgeted, although payments under food and petroleum subsidies have been higher than a year ago. In the revised estimates for 2017-18, the outgo on account of major subsidies was estimated at 1.4 per cent of GDP, up from 1.3 per cent in 2016-17. Various categories of revenue expenditure take the form of committed payments with little room for cutbacks. Meanwhile, capital expenditure rose by 38.3 per cent up to February and constituted 108.6 per cent of the revised estimates (which were revised downwards from the budget estimates for the year). Accordingly, to meet the revised estimates, budgetary adjustments in the remaining part of the year might not involve any capex reduction, which has been stepped up over a wide area comprising civil aviation, defence, heavy industry, petroleum & natural gas, railways, shipping and road transport, including highways. | Table III.2: Key Fiscal Indicators - Central Government Finances | | Indicator | Per cent to GDP | | 2017-18 (BE) | 2017-18 (RE) | 2018-19 (BE) | | 1. Revenue Receipts | 9.0 | 9.0 | 9.2 | | a. Tax Revenue (Net) | 7.3 | 7.6 | 7.9 | | b. Non-Tax Revenue | 1.7 | 1.4 | 1.3 | | 2. Non Debt Capital Receipts | 0.5 | 0.7 | 0.5 | | 3. Revenue Expenditure | 10.9 | 11.6 | 11.4 | | 4. Capital Expenditure | 1.8 | 1.6 | 1.6 | | 5. Total Expenditure | 12.8 | 13.2 | 13.0 | | 6. Gross Fiscal Deficit | 3.2 | 3.5 | 3.3 | | 7. Revenue Deficit | 1.9 | 2.6 | 2.2 | | 8. Primary Deficit | 0.1 | 0.4 | 0.3 | Note: BE: Budget Estimates, RE: Revised Estimates.

Source: Union Budget, 2018-19. | Both gross and net tax collections were marginally higher than their budgeted levels, mainly on account of buoyant direct tax revenues under corporation tax (Chart III.9a). The budgeted buoyancies for all tax categories of direct taxes are higher in 2018-19 than the average of the preceding eight years (2010-11 to 2017-18), suggesting that revenue mobilisation would be a major challenge. Indirect tax collection during Apr-Feb. 2017-18 were higher by 12.9 per cent than their level a year ago (Chart III.9b). As per the Union Budget 2018-19, total revenue under GST for 2017-18 (RE) aggregated ₹ 4,446 billion. Collections under Centre GST (CGST) and integrated GST (IGST) were ₹ 2,214 billion and ₹ 1,619 billion, respectively. Non-tax revenues fell short of the budget target by 18.3 per cent due to lower receipts from dividends and profits as well as deferment of spectrum auctions. Total non-debt capital receipts were higher than the budget estimates (BE) by ₹ 330 billion on account of disinvestment proceeds, which exceeded the target of ₹ 725 billion.  State finances have a significant bearing on the overall fiscal position of the general government. The latest available data for 21 States suggest a slippage in the combined GFD to gross state domestic product (GSDP) ratio to 3.0 per cent in 2017-18 (RE) as against 2.6 per cent budgeted (Table III.3). Revenue expenditures of states have shown significant divergences from budget estimates of 2017-18 so far, resulting from several factors such as implementation of the recommendations of states’ pay commissions, farm loan waiver in some states and rising interest burden (Chart III.10). This poses a challenge for overall fiscal consolidation. Though the budgeted fiscal deficit for 2018-19 for 21 states is placed lower at 2.5 per cent of GSDP, it is likely to come under pressure due to several factors such as upcoming state elections, likely farm debt waiver, and implementation of pay commission awards by some states. The borrowing programme of the Centre for 2017-18 was conducted at levels higher (1.4 per cent) than in the overall budgeted strategy, while States, at the aggregate level, borrowed less (13.4 per cent) than budgeted (Table III.4). A strategy of debt consolidation was undertaken through buybacks and switches to the extent of ₹ 416 billion and ₹ 581 billion, respectively. Gross market borrowings of the central government through dated securities for 2018-19 have been budgeted at ₹ 6,055 billion and net market borrowings at ₹ 4,621 billion. | Table III.3: Major Deficit Indicators – State Governments | | (Per cent to GSDP) | | Item | 2016-17 | 2017-18 BE | 2017-18 RE | 2018-19 BE | | Revenue Deficit | 0.4 | 0.0 | 0.4 | -0.1 | | Gross Fiscal Deficit | 3.4 | 2.6 | 3.0 | 2.5 | | Primary Deficit | 1.7 | 0.9 | 1.3 | 0.9 | Notes: 1. Negative (-) sign indicates surplus.

2. Data pertain to 21 out of 29 States.

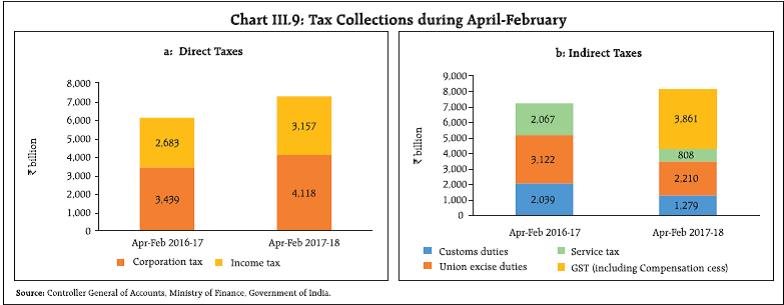

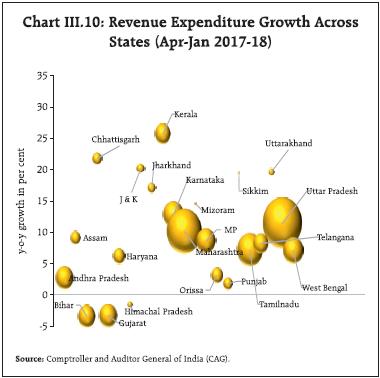

Source: Budget Documents of State Governments. | The Centre’s gross fiscal deficit target of 3.2 of GDP for 2017-18 was exceeded by 0.3 percentage points of GDP. A slippage of the same magnitude has also been observed for states. Slippages in key deficit indicators have raised questions about the credibility of fiscal consolidation. In addition, higher fiscal deficits crowd out productive private sector investment. It is also worrying that revenue expenditure of the Centre for 2018-19 is budgeted to grow at a higher rate (10.2 per cent) than capital expenditure (9.9 per cent). In this context, even as the increase in outlays on agriculture and infrastructure proposed in the Union Budget for 2018-19 is welcome, concerted efforts need to be made to improve revenues. While disinvestment proceeds helped contain the fiscal deficit in 2017-18, they are contingent upon market conditions. It is important that tax revenues are maximised by expanding coverage and compliance, rationalising exemptions and building innate buoyancy so that the fiscal deficit budgeted for 2018-19 is adhered to without compromising the quality of the fiscal adjustment process.

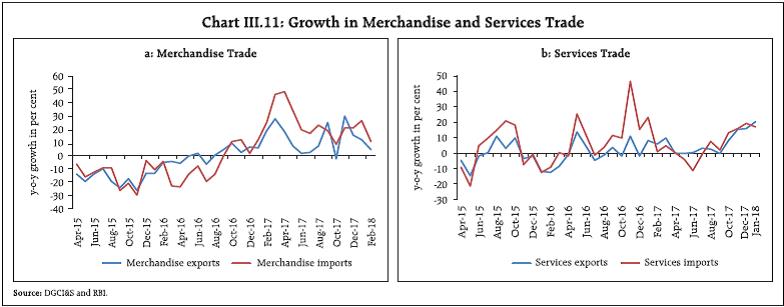

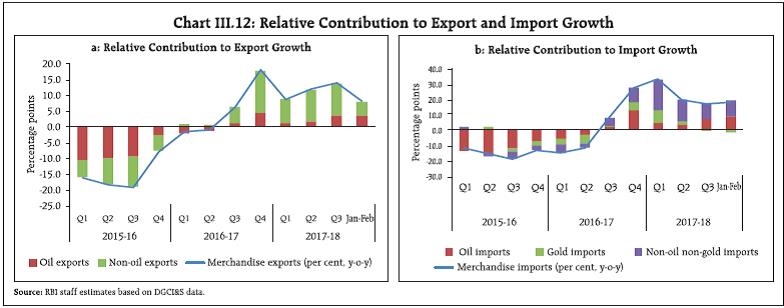

| Table III.4: Government Market Borrowings | | (₹ billion) | | Item | 2015-16 | 2016-17 | 2017-18 | | Centre | States | Total | Centre | States | Total | Centre | States | Total | | Net Borrowings | 4,406 | 2,594 | 7,000 | 4,082 | 3,426 | 7,508 | 4,484 | 3,403 | 7,887 | | Gross Borrowings | 5,850 | 2,946 | 8,796 | 5,820 | 3,820 | 9,640 | 5,880 | 4,191 | 10,071 | | Source: RBI. | III.1.4 External Demand Net exports continued to act as a drag on aggregate demand in H2:2017-18 with rapid import expansion outpacing exports (Charts III.11a and 11b). Although export growth slowed down to less than 3 per cent in H2:2017-18 from 6.2 per cent in H1:2017-18, there was a bounce-back in November and December with the easing of implementation hurdles associated with the GST. In Q4, however, there has been a sequential loss of pace, pointing to underlying weaknesses in the domestic supply response to rising external demand, especially in labour-intensive categories such as readymade garments, and gems and jewellery. Non-oil exports constitute a significant part of India’s exports, with engineering goods, and chemicals being consistent contributors through 2017-18 (up to January) (Chart III.12a). In line with trends in global trade, advanced economies (AEs) accounted for a larger share of the increase in India’s exports than emerging market economies (EMEs). Turning to imports, a large part of the strong growth was accounted for by non-oil non-gold imports during 2017-18 so far, attesting to the growing strength of domestic demand (Chart III.12b). Pearls and precious stones, electronic goods and coal1 were major contributors. Restocking by power plants and the growing requirements of the Indian steel sector led to an increase in coal imports in Q3:2017-18 to US$ 6.1 billion (56.8 million tonnes) from US$ 4.2 billion (44.8 million tonnes) in Q3:2016-17. Firming international crude oil prices on account of the Organization of the Petroleum Exporting Countries (OPEC) persisting with production cuts caused POL import bill to rise. Gold imports increased – both in value and volume terms – in December after declining in the preceding three months, but declined again in January 2018 due to the postponement of purchases in anticipation of reduction in customs duty on imports. Overall, merchandise import growth, which had largely declined sequentially up to October, started increasing strongly from November 2017, pushing the April-February trade deficit to a five-year high of US$ 143 billion.