[Under Section 45ZL of the Reserve Bank of India Act, 1934]

The thirty second meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held from December 6 to 8, 2021.

2. The meeting was attended by all the members – Dr. Shashanka Bhide, Senior Advisor, National Council of Applied Economic Research, Delhi; Dr. Ashima Goyal, Emeritus Professor, Indira Gandhi Institute of Development Research, Mumbai; Prof. Jayanth R. Varma, Professor, Indian Institute of Management, Ahmedabad; Dr. Mridul K. Saggar, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Michael Debabrata Patra, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor.

3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely:

-

the resolution adopted at the meeting of the Monetary Policy Committee;

-

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and

-

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting.

4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below.

Resolution

5. On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (December 8, 2021) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

The reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

- The MPC also decided to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

6. Since the MPC’s meeting during October 6-8, 2021, surges of infections across geographies, emergence of the Omicron variant, the persistence of supply chain disruptions and elevated energy and commodity prices continue to weigh on global economic activity. Global merchandise trade is slowing after a sharp rebound from the pandemic due to the disruptions in port services and turnaround time, elevated freight rates and the global shortage of semiconductor chips, which could dampen future manufacturing output and trade. The composite global purchasing managers’ index (PMI), however, improved to a four-month high in November, with services continuing to perform better than manufacturing for eight consecutive months.

7. Commodity prices remain elevated across the board, though there has been some softening since late October and further drop towards end-November following uncertainties from the new COVID-19 variant, among others. Headline inflation in several advanced economies (AEs) and emerging market economies (EMEs) has soared, prompting a number of central banks to continue tightening and others to bring forward policy normalisation. With the US Federal Reserve commencing tapering of its monthly asset purchases and the possibility of faster taper, renewed bouts of volatility and heightened uncertainties have unsettled global financial markets. Bond yields which had risen in most countries, responding to inflation and monetary policy actions, eased from the last week of November. The US dollar has been trading higher in recent weeks against both AE and EME currencies.

Domestic Economy

8. On the domestic front, data released by the National Statistical Office (NSO) on November 30, 2021 showed that real gross domestic product (GDP) expanded by 8.4 per cent year-on-year (y-o-y) in Q2:2021-22, following a growth of 20.1 per cent during Q1:2021-22. With the recovery gaining momentum, all constituents of aggregate demand entered the expansion zone, with exports and imports markedly exceeding their pre-COVID-19 levels. On the supply side, real gross value added (GVA) increased by 8.5 per cent y-o-y during Q2:2021-22.

9. Available data for Q3:2021-22 indicate that the momentum of economic activity is gaining further traction, aided by expanding vaccination coverage, the rapid subsiding of new infections and release of pent-up demand. Rural demand exhibited resilience – tractor sales improved in October over the same month of 2019 (pre-pandemic level), while motorcycle sales are slowly inching towards their pre-pandemic levels. Continued direct transfers under PM Kisan scheme are supporting rural demand. The demand for work under the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) moderated in November from a year ago, suggesting a pickup in farm labour demand. Supported by favourable soil moisture content and good reservoir storage levels, rabi sowing was 6.1 per cent higher than a year ago as on December 3, 2021.

10. Urban demand and contact-intensive services activities are rebounding on improving consumer optimism, supported by festival demand. High-frequency indicators such as electricity demand, railway freight traffic, port cargo, toll collections, and petroleum consumption registered robust growth in October/November over the corresponding months of 2019. Automobile sales, steel consumption and air passenger traffic still remained below 2019 levels even though they gained momentum in October as supply side shortages eased. Investment activity is exhibiting modest signs of improvement – production of capital goods remained above pre-pandemic levels for the third month in a row during September, while import of capital goods in October rose at double-digit pace over its level two years ago. Prints of manufacturing and services PMIs for November 2021 suggested continued improvement in economic activity. Exports grew in November for the ninth month in a row, along with a surge in non-oil non-gold imports on the back of reviving domestic demand.

11. Headline CPI inflation, which has been on a downward trajectory since June 2021, edged up to 4.5 per cent in October from 4.3 per cent in September on account of a spike in vegetable prices – due to crop damage from heavy rainfalls in October in several states, and fuel inflation – driven up by international prices of liquefied petroleum gas and kerosene. In fact, fuel inflation at 14.3 per cent in October surged to an all-time high. Core inflation or CPI inflation excluding food and fuel remained elevated at 5.9 per cent during September-October with continuing upside pressures stemming from clothing and footwear, health, and transportation and communication sub-groups.

12. Liquidity conditions remained in large surplus, with daily absorptions through the fixed rate reverse repo and the variable rate reverse repo (VRRR) operations under the liquidity adjustment facility (LAF) averaging ₹8.6 lakh crore in October-November. Reserve money (adjusted for the first-round impact of the change in the cash reserve ratio) expanded by 7.9 per cent (y-o-y) on December 3, 2021. Money supply (M3) and bank credit by commercial banks grew y-o-y by 9.5 per cent and 7.0 per cent respectively, as on November 19, 2021. India’s foreign exchange reserves increased by US$ 58.9 billion in 2021-22 (up to December 3, 2021) to US$ 635.9 billion.

Outlook

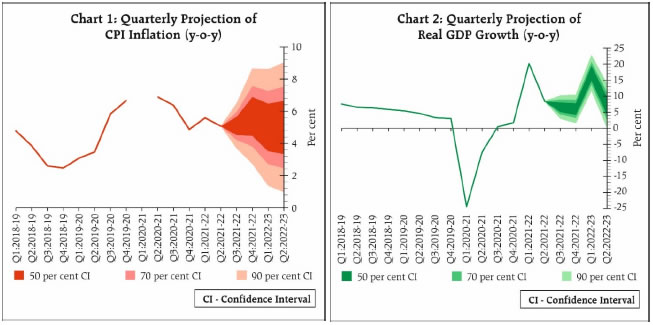

13. The inflation trajectory, going forward, will be conditioned by a number of factors. The flare-up in vegetables prices due to heavy rains in October and November is likely to reverse with the winter arrivals. Rabi sowing is progressing well and is set to exceed last year’s acreage. Recent pro-active supply side interventions by the Government continue to restrain the pass-through of elevated international edible oil prices to domestic retail inflation. Crude prices have seen a significant correction in recent period. Cost-push pressures from high industrial raw material prices, transportation costs, and global logistics and supply chain bottlenecks continue to impinge on core inflation. The slack in the economy is muting the pass-through of rising input costs to output prices. Taking into consideration all these factors, CPI inflation is projected at 5.3 per cent for 2021-22; 5.1 per cent in Q3; 5.7 per cent in Q4:2021-22, with risks broadly balanced. CPI inflation for Q1:2022-23 is projected at 5.0 per cent and for Q2 at 5.0 per cent (Chart 1).

14. The recovery in domestic economic activity is turning increasingly broad-based, with the expanding vaccination coverage, slump in fresh COVID-19 cases and rapid normalisation of mobility. Rural demand is expected to remain resilient. The spurt in contact-intensive activities and pent-up demand will continue to bolster urban demand. The government’s infrastructure push, the widening of the performance-linked incentive scheme, structural reforms, recovering capacity utilisation and benign liquidity and financial conditions provide conducive conditions for private investment demand. The Reserve Bank’s surveys point to improving business outlook and consumer confidence. On the other hand, volatile commodity prices, persisting global supply disruptions, new mutations of the virus and financial market volatility pose downside risks to the outlook. Taking all these factors into consideration and assuming no resurgence in COVID-19 infections in India, the projection for real GDP growth is retained at 9.5 per cent in 2021-22 consisting of 6.6 per cent in Q3; and 6.0 per cent in Q4:2021-22. Real GDP growth is projected at 17.2 per cent for Q1:2022-23 and at 7.8 per cent for Q2 (Chart 2).

15. The impact of the recent spike in vegetables prices on food inflation prints is expected to dissipate as the usual softening of prices in the winter sets in. The partial roll back of Central excise and State Value Added Taxes (VAT) on petrol and diesel in November have eased retail selling prices and will have second round effects over a period of time. Crude oil has seen some correction but remains volatile. Core inflation will need to be closely monitored and held in check. For a sustained lowering of core inflation, continuing the normalisation of excise duties and VATs alongside measures to address other input cost pressures assume critical importance, more so as demand improves. The domestic recovery is gaining traction, but activity is just about catching up with pre-pandemic levels and will have to be assiduously nurtured by conducive policy settings till it takes root and becomes self-sustaining. In particular, private investment has to lead the revival of the economy, along with the strong impetus being provided by exports. Private consumption, despite strong recovery in Q2:2021-22, remains below its pre-pandemic level and demand for contact-intensive services could potentially face headwinds if authorities take pre-emptive steps to contain the fallout of Omicron. Downside risks remain significant rendering the outlook highly uncertain, especially on account of global spillovers, the potential resurgence in COVID-19 infections with new mutations, persisting shortages and bottlenecks and the widening divergences in policy actions and stances across the world as inflationary pressures persist. A tightening of global financial conditions poses risks to global economic activity and to India’s prospects as well. Against this backdrop, the MPC has judged that the ongoing domestic recovery needs sustained policy support to make it more broad-based. Considering it appropriate to wait for growth signals to become solidly entrenched while remaining watchful on inflation dynamics, the MPC decided to keep the policy repo rate unchanged at 4 per cent and to continue with an accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

16. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 4.0 per cent.

17. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma, voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Prof. Jayanth R. Varma expressed reservations on this part of the resolution.

18. The minutes of the MPC’s meeting will be published on December 22, 2021.

19. The next meeting of the MPC is scheduled during February 7-9, 2022.

| Voting on the Resolution to keep the policy repo rate unchanged at 4.0 per cent |

| Member |

Vote |

| Dr. Shashanka Bhide |

Yes |

| Dr. Ashima Goyal |

Yes |

| Prof. Jayanth R. Varma |

Yes |

| Dr. Mridul K. Saggar |

Yes |

| Dr. Michael Debabrata Patra |

Yes |

| Shri Shaktikanta Das |

Yes |

Statement by Dr. Shashanka Bhide

20. The quarterly GDP estimates by NSO for July-September 2021 point to a continued expansion of the economy, YOY basis, with GDP at constant prices rising by 8.4%, following the increase of 20.1% in Q1FY22. The Q2FY22 GDP estimates are higher than 7.9% projected in the October meeting of MPC. The GDP estimate also reflects growth of 10.4% over the previous quarter. While these are significant positive trends, there are new concerns on the growth front on account of the implications of the emergence of the new variants of the Corona virus and uncertainty of global growth and inflation scenarios.

21. In terms of the return of the economy to the pre-pandemic level, progress has been significant but sustained improvement of this performance is critical to the economy. In this context, GDP growth in Q2FY22 is only 0.3% over the pre-pandemic Q2FY20. The improvement needed to return to the pre-pandemic levels is also reflected in the estimates of final consumption expenditure and investment. Although Private Final Consumption Expenditure grew by 8.6% in Q2FY22 YOY basis in constant prices, it was 3.5% below Q2FY20 level. The Gross Fixed Capital Formation, in constant prices, increased YOY basis by 11% in Q2FY22 and rose only 1.5% over Q2FY20. The quarter- on- quarter improvements in PFCE and GFCF in Q2FY22 are indicators of momentum in the economy that needs to be sustained for achieving further expansion of the economy leading to employment and income growth.

22. At a broad level, output levels of the various sectors in Q2FY22 measured by GVA at constant prices are above Q2FY21. But there is also unevenness in growth performance reflecting sectoral and other structural variations in the adjustments taking place in the economy in the ongoing recovery process. In the case of ‘Trade, hotels, transportation, communications and broadcasting services’, which had a share of 20.3% in total GVA in 2019-20, the gap from Q2FY20 is 9.2%. In general, the pace of output recovery in contact-intensive sectors is likely to be affected by both supply side constraints and weak demand, conditions which may abate only with further relief from the pandemic. The slower output growth is also contributed by supply disruptions as in the case of semiconductor chips affecting particularly production of passenger cars and the travel restrictions affecting the aviation sector and the related businesses. The IIP for manufacturing has shown only a modest YOY growth of 3.1% in September 2021. The overall weak demand conditions are reflected in the RBI’s Consumer Confidence Survey for November 2021, in which a large majority of the urban respondents presently remain cautious on ‘incurring non-essential consumption expenditure’.

23. The private investment, an important component of aggregate demand would be a key to sustaining the momentum of GDP growth. RBI’s enterprise survey for November 2021 points to improvement in business outlook for Q3FY21 but majority of the respondents remain cautious. NCAER’s Business Confidence Index based on a survey conducted in September registered improvement QOQ basis and also over Q2FY2020. The financial performance of the private corporate sector in Q2FY2022 suggests a steady growth in sales in Q2FY22 but investment indicators reflect a subdued investment activity. A key factor influencing the private investment in the manufacturing sectors appears to be the level of capacity utilisation, which is still below the long-term average reflecting both demand and supply constraints. While there are positive drivers such as FDI, the uncertainty surrounding the relief from the pandemic and global growth scenario are the other factors affecting caution in investment decisions.

24. Agricultural sector is expected to be supportive of the overall GDP growth in FY 2021-22, with normal rainfall conditions although they were also marked by uneven rainfall.

25. The export growth in October-November 2021 has continued to support overall GDP growth. The NSO estimates of rupee value of exports of goods and services at constant prices in Q2FY22 are 19.6% higher on YOY basis, following an increase of 39.1% in Q1FY22. The merchandise exports in dollar value during April-November 2021-22 is 262.5 billion compared to 174.2 billion in the same period of 2020-21. Imports have also increased sharply YOY basis in H1FY22 partly indicating the rising domestic economic growth but also reflecting the price increase in some of the critical imports such as the petroleum imports. The global uncertainty on economic growth, resulting from fresh surges of Covid infections is a challenge in sustaining export performance in the short term. In its October 2021 World Economic Outlook, IMF lowered world GDP growth projections for 2021 compared to its projections in July 2021. Going further, the projected growth in 2022 is one percentage point lower than in 2021.

26. A number of high frequency indicators of the economy do point to revival of the growth momentum in Q2FY22 and the subsequent months of October and November 2021. PMIs, cement production, GST collections, E-way bills, domestic and international air traffic, housing launches, housing sales, Google mobility indices show robust performance YOY basis. The government revenue expenditure in Q2FY22 for the Centre and States registered double digit growth YOY basis. Indicators such as railway freight, motor spirits consumption show improvement YOY basis and remain above 2019-20 levels or catching up with them. Some of these indicators also show some deceleration in YOY growth in the recent months. Port traffic data shows moderate growth and has reached 2019-20 level in October 2021. The key financial sector indicators, deposit and commercial credit by the banking sector, have shown steady improvement during 2021-22.

27. RBI’s Survey of Professional Forecasters for November 2021 provides a median forecast of YOY GDP growth for FY2021-22 at 9.5%, a slight upward revision from the September 2021 forecast of 9.4% with significant improvement in the growth of industrial output balanced by slower services growth. Based on the present trends and patterns of indicators of growth, and actual growth estimates for Q1 and Q2, the YOY GDP growth for 2021-22 has been retained at 9.5%. The growth rates for Q3 and Q4 for the present financial year are projected at 6.6% and 6.0%, respectively.

28. Achieving these growth projections in the face of concerns over the new variants of Corona virus and the return from accommodative monetary policy in the advanced economies suggest a need for policy measures supportive of growth drivers.

29. The inflation pressure measured in terms of YOY headline CPI in October is at 4.5 per cent, slightly higher than 4.3 per cent in September. CPI Food, YOY basis is at 1.8%, fuel at 14.3% and CPI core (excluding food and fuel) is at 5.9%. In the case of Food and Fuel, the YOY increase in October is higher than in September 2021 and remains more or less at its level in September and October 2021 in the case of core inflation. Between July and October 2021, the core inflation has remained at 5.8-5.9% in each month. CPI Fuel increased by 12.4% in July 2021 YOY basis, rising steadily reaching 14.3% in October. Food inflation dropped from 4.5% in July to 1.8% in October 2021. While the retail prices of fuel are affected by the various taxes and subsidies, it may be noted that average YOY increase in Brent crude oil prices in dollar value during October 2021 exceeded 100%. The rising fuel prices are clearly driving the cost of energy and transportation costs in every other sector. In the RBI’s enterprise surveys of October-December 2021 covering manufacturing, services and infrastructure sectors, a large majority of the respondents report cost increase and also increase in selling prices. The pickup in economic activity has also increased demand for inputs leading to higher prices to the consumer.

30. Taking into account the patterns of changes in prices in different components of CPI, the headline inflation rate for Q3 and Q4 is now projected at 5.1% and 5.7%, respectively and 5.3% for FY2021-22 as a whole. The high level of core inflation is a concern that affects both consumption expenditure and profitability of firms. Sustained improvement in output will require reduction in inflation rate achieved through easing of supply constraints and productivity improvement to revive consumer and investment demand. While there is ample liquidity in the system, bank credit to commercial sector as a ratio to money supply (M3) remains below the levels seen during 2019-20. Full transition from the two major disruptions inflicted by the pandemic on the supply and demand systems to normalcy will require policy support to both output growth and ease inflation pressures.

31. In view of the projected growth and inflation rates and the emerging uncertainty from the renewed surge of Covid infections and macroeconomic adjustments at a global level, I vote in favour of keeping the policy repo rate unchanged at 4.0 per cent. I also vote in favour of continuing with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

Statement by Dr. Ashima Goyal

32. Global risks are rising with the Omicron variant as well as with expectations of an earlier Fed taper. Markets are volatile as are oil prices. In such circumstances it is better for the MPC to remain steady and watchful through the next couple of months. International oil prices may fall further after the winter season. Their high volatility means collapse is possible. Some analysts expect an unwinding of demand because excess inventories were built for festival demand.

33. While US inflation is now expected to be less temporary because of the large fiscal stimulus and withdrawal from the labour force, these conditions do not hold in India. The differential between Indian and US real rates is high because of higher US inflation, so some Fed tightening in future does not necessarily require our policy rates to rise.

34. Indian household inflation expectations have fallen steeply in end November compared to their rise in early November following governments’ cut in fuel taxes and softening of international oil prices. The expectations are at or below their September levels. Firms’ price expectations have also somewhat reduced. Although core inflation is elevated the major share in the rise comes from transport and communication. Transport at least may soften with oil prices. There are signs of cost push in more commodities, but the contribution of services such as household goods and services, personal care and effects and education, which are demand driven remains low.

35. Government’s critical and just in time supply-side side action has enabled monetary policy accommodation. In the post Covid-19 world of supply shocks and high government debt monetary-fiscal coordination has become acceptable in advanced economies (AEs), while earlier it was regarded as compromising monetary policy independence. But a flexible inflation targeting regime has to respond to demand-side inflation and to supply-side inflation that has second round effects. This ensures central bank independence and contributes to anchor inflation expectations. Coordination is consistent with central bank independence since low rates are conditional on supply-side action.

36. In India, moreover, coordination normally does better because supply shocks dominate inflation and can be better influenced by state action. Monetary policy has more space to affect demand, while high debt and interest payments constrain fiscal spending. Policy rates can adjust more easily to appropriately fine-tune demand, watching to see if exports and pent-up demand moderate, or if there is overheating and persistent inflation.

37. Research shows that monetary transmission to output is effective in Indian conditions1. A semi-structural estimation with gap variables obtains an interest elasticity of aggregate demand (-0.21) as high as in AEs. This is intuitive because consumer durable and housing loan demand is interest elastic and induces demand for working capital and investment funds. Covid-19 naturally led to postponement of projects, as uncertainty increased and consumer confidence fell, so that time is required for revival. Even so investment in specific sectors did rise in 2020 itself, following softer monetary-financial conditions. By October 2021 there was a perceptible rise in credit. Although credit growth to overall industry was only 4%, that to medium industries was 48.6%. Large industries are deleveraged, cash rich and have access to the corporate bond market. Credit to MSMEs and personal loans grew above 11%, with that to consumer durables at 44%.

38. Q2 GDP data also shows signs of investment revival. Aggregate GDP has passed 2019 levels, but consumption and stressed sectors remain below it pointing to income loss that still has to be made-up. Excess capacity and unemployment continues to be high. Potential output is difficult to measure in the Indian context2 and is best defined by a persistent rise in inflation above the tolerance band, which is not the case at present, implying the output gap is negative. Real rates are less negative, to the extent one year ahead inflation projections have softened.

39. Estimated Indian aggregate supply shows a mixture of backward and forward looking behaviour. When there are some lags, stability requires monetary policy to respond early but slowly3. There is steady progress in fine-tuning and control of liquidity since early this year. Since the share of VRRR has gone up, the weighted average reverse repo rate is higher and some other short rates have risen. Additions to durable liquidity have stopped. But the next step is to decrease excess durable liquidity itself. Some of this will be absorbed as growth rises. Banks are already raising some deposit rates in anticipation of a rise in credit. Even as excess aggregate liquidity reduces, RBI policies targeting liquidity at stressed sectors must continue.

40. In view of these considerations I vote to continue with the current stance and repo rate.

Statement by Prof. Jayanth R. Varma

41. My views have not changed much since the August and October statements. I believe that monetary policy is no longer the right instrument to deal with the Covid-19 pandemic whose economic effects (as opposed to its health effects) have diminished greatly and become more concentrated in narrow pockets of the economy. There is no evidence so far to suggest that the Omicron variant of the Covid-19 virus would change the picture materially.

42. Economic activity appears to have surpassed its pre-pandemic level, continued recovery is likely during the rest of 2021-22, and the prognosis is for healthy growth in 2022-23 as well. On the other hand, there is increasing evidence of inflation becoming persistent in the upper region of the tolerance band, though it is projected to remain within the band.

43. In this environment, it is no longer appropriate to stick to the monetary policy stance first adopted in May 2020 when the adverse economic effects of the pandemic were at their peak. I am therefore not in favour of the decision to keep the reverse repo rate at 3.35%, and vote against the accommodative stance. Raising effective money market rates quickly towards 4% would demonstrate the MPC’s commitment to the inflation target, help anchor expectations, reduce risk premia, enhance macroeconomic stability, and allow lower long-term interest rates to be sustained for longer thereby aiding the economic recovery.

44. On the other hand, I vote for maintaining the repo rate at 4% for the following reasons. Economic growth was unsatisfactory long before the pandemic, and even if the economic ill effects of the pandemic abate to some extent, substantial monetary accommodation is warranted. The repo rate of 4% corresponds to a negative real rate in the range of 1-1.5% based on forward looking inflation forecasts. In my view, this level of rates is currently appropriate for reviving economic growth without excessive risk of an inflationary spiral. Needless to say, the MPC needs to remain data driven so that it can respond rapidly and adequately to any unforeseen shocks that may arise in future.

Statement by Dr. Mridul K. Saggar

45. At the October MPC, I had cautioned on the likelihood of significant headwinds from the shifting global macro-economic conditions. The Fed start of taper last month was at an envisaged pace as guided by it in September and as expected by the financial markets. However, there were three surprises since our last meeting. First, inflation in the US and across the globe surprised on the up indicating that inflation may persist longer than what may be traditionally viewed as “transitory”. Second, supply-side disruptions seem to be elongated and spilling over to several geographies running through oil, gas, minerals and metals and, together with climatic factors, is lately spilling over to agro-space in a significant manner reflected in food and fertiliser prices climbing up. Third, these two factors have combined to contribute to higher inflation and lower growth prospects, raising spectre of stagflationary impulses globally.

46. The uncertainties regarding each of these factors have risen markedly in recent period. Equities markets may see more of volatile adjustments of the type seen in the last week of November as analysts adjust multiples to the changed macroeconomic environment. Bonds steepening trades in the belly of the curve will contribute to flattening of the yield curve but will also generate cross-border trades which can cause portfolio outflows. These volatilities can spillover to exchange rates. Markets are already turbulent trying to price risks emanating from the high transmissibility and spike mutations of Omicron variant, some of which are already materialising in the form of fresh travel bans and intensified protocols to contain its spread. The risk to global growth in my view has already surfaced from the rapid rise in new Covid infections in Europe and the U.S, with the 7-day Moving Averages of daily new confirmed Covid-19 cases standing in the vicinity of 3.70 lakh and 1.20 lakh, respectively. The situation remains alarming. It is clear, that the pandemic is far from over yet, though learning effects and vaccinations will help us cope with it better. So, where is the global economy headed? In my view the risk of a return to stagflation of the 1970s is rather remote. However, global growth is slowing once more and central banks, including ours, will need to confront the inflation challenge with careful calibration and avoid impulses that may kindle or deepen stagflationary impulses. In my judgement, these impulses should be mild one but could turn into a moderate one if monetary policy is not well-calibrated. Policy errors in either direction on the part of the central banks at this stage are laden with serious risks.

47. Let me turn to India. Growth is picking up. The Q2:2021-22 GDP and GVA were 0.3 per cent and 0.5 per cent above the pre-pandemic Q2:2019-20. On the demand side, PFCE was slightly less (-3.5%) than pre-pandemic Q2, while gross capital formation was 7.8 per cent above it. On the supply side, agriculture and allied activities and all three sectors of industry were above the pre-pandemic levels, while services sector (including construction) was only 2.2 per cent below pre-pandemic Q2. Only trade, hotels, transport, communication and broadcasting services remained markedly below pre-pandemic Q2 (-9.2 per cent). Information from business sources suggests that hotel occupancy and restaurant utilisation rates, though improving, are just half of the pre-pandemic levels. Tourism and travel are faring even worse. This is also an indicator to suggest that informal sector faces an uphill task in normalising production.

48. Overall, out of the 59 high frequency indicators that have become available for October out of 67 that I track, 88 per cent of the indicators exhibited month-on-month improvement after a somewhat weak August and September. The momentum towards normalisation has picked up significantly, but a third of indicators have yet to cross their pre-pandemic levels. Moreover, the stress in informal sector is not adequately captured by these indicators.

49. On the consumption side, trade reports suggest that Diwali sales jumped 71 per cent this year compared with 17 per cent, 20 per cent and 16 per cent in the preceding three years. On the investment side, partial information for Q2 and informal feedback obtained from corporates and banks suggest that capacity utilization rates in manufacturing have improved and is likely to have crossed 70 per cent mark but will likely remain slightly below trend levels in Q3:2021-22. Though the pipeline investment from last year is weak, there is anecdotal evidence of new projects that are or can soon get into financial closures. The road sector stands out, but some investment is also seen in cement, iron and steel, textiles, solar power, chemical and chemical products.

50. On the inflation, the momentum in October was strong. CPI increased 1.4 per cent month-on-month in October, which is more than double the normal momentum. Seasonally adjusted annualised rate of CPI inflation touched 10.0 per cent and item level data indicates pickup in diffusion. Passthrough from WPI inflation will need to be closely watched with October momentum reaching an all-time high at 2.3 per cent month-on-month. Diffusion of price rise was also high at the wholesale price level. Core inflation remains elevated and sticky. In this milieu, we need to be eagle-eyed for the passthrough of producer prices to retail levels and be ready to act should the need arise. If growth improves further, we should use the opportunity to nudge inflation and inflation expectations down.

51. I finally turn to decisions at hand in this meeting. With inflation having bottomed out, the real interest rate adjustment assumes added importance. Macroeconomic adjustments of saving-investment balance will be critical as global interest rate cycle changes in face of tapers and lift offs. While we are very close to growth having revived, its durability is still not entirely clear. On the other hand, inflation has come back below upper tolerance level for the last four months and while the upside risks exist, the baseline affords some comfort that inflation should stay mid-way between the target and the upper tolerance band in H1:2022-23. If one were certain about a broad-based durable growth revival, monetary policy could have acted now to pre-empt the possibility of inflation resurgence. However, the key question is whether the economy can entail the output sacrifice it may bring at a time when the recovery is nascent. Therefore, it will be best not to risk strengthening stagflationary impulses that already are being propped up by supply disruptions mentioned upfront in my statement. Small moves towards policy normalisation may be sufficient now and one can decide to shift to a tightening monetary policy cycle at a point when it is clear that demand revival has acquired resilience and pandemic risks to growth have diminished or alternatively if inflation diffusion persists in near months which then can result in inflation getting generalised and persist next year, especially if inflation expectations get unanchored. Short-run Phillips curve can shift up and turn steeper in this case. Yet, at this juncture, it looks India will be able to contain inflationary pressures through better supply-side responses.

52. One month’s data suggesting strong growth and inflation momentums is not sufficient to change rate cycles or policy stance. This guiding rule has helped us avert the mistake of premature tightening on at least two earlier occasions. This, however, does not mean status quo. Central bank has an armoury of tools to calibrate monetary and financial conditions. The Pascal’s principle for transmission of fluid pressures very much holds and appropriate liquidity levels are key to monetary adjustment at this stage. This is also important to address unintended effects reflected in asset prices inflation, income inequalities and future risks of macro-financial imbalances. Keeping in view the Swiss knife-like policy tools the central bank possesses to deal appropriately with the emerging trends, I vote to leave the repo rate unchanged at 4.0 per cent and also vote for retaining the stance.

Statement by Dr. Michael Debabrata Patra

53. Suddenly, the global outlook has darkened. Three fundamental questions about Omicron have put national authorities on high alert – is it more transmissible than other variants? Can it evade immunity conferred by previous infections or vaccination? Does it cause more severe disease?

54. As countries race to contain Omicron with travel restraints and new quarantine and social distancing measures, the global recovery and the inflation outlook are at risk again.

55. Even before Omicron, the momentum of the global recovery and of world trade has been ebbing in the second half of 2021, including in countries with relatively high vaccination rates. With GDP prints coming in lower for several countries, estimates suggest that global GDP growth is slowing by a full percentage point in the second half of 2021 on a sequential seasonally adjusted annualised basis. In some countries, the level of GDP may have reached pre-pandemic levels, but that is of little comfort as activity worldwide had been slowing since 2018. In many other countries, negative output and employment gaps are still too wide, and that is sapping global aggregate demand. The path of the recovery is still being shaped by the pandemic and its second order effects. The question that is uppermost is: Has the global recovery peaked prematurely, leaving behind the scars of the pandemic?

56. Fears about the new variant triggered the biggest Black Friday plunge on record in global equity markets on November 26, 2021. Even earlier, financial market volatility had surged in recent weeks on fears of a policy pivot towards faster normalisation. Clearly, financial conditions are highly fragile, vulnerable to volatile shifts and not conducive to a strong and broad-based recovery.

57. The pretext underlying financial market volatility – what I term the cynicism of bonds and the ‘fomo’ of equities – is that inflation has checked in as if it is here to stay. In some countries, the dogs of second order transmission have begun to bark – wages; rents; education fees; transportation costs. The world helplessly stares at what have become household terms - supply and logistics disruptions, shortages and bottlenecks – but the need of the hour is coordinated action. Consequently, markets and analysts get increasingly certain that inflation may remain elevated through the greater part of 2022 and growth will slow further absent policy action to unclog supply bottlenecks.

58. Yet, it is important to be cognisant of the bullwhip effect – when shortages turn into surpluses. Some evidence of this happening is already there. Finished goods inventories are piling up as shown in PMIs of several advanced countries and promises of discounts, sales and faster deliveries are getting louder. When these inventories will be wound down, they will reduce new orders and economic activity will slow. An excess of finished goods may also lead to weak pricing power, which will moderate inflation. It is likely that this will happen in the first half of 2022. Meanwhile, final private consumption expenditure seems to be weakening in individual countries’ data releases. India’s November 30 release was no exception.

59. As far as the emerging markets as an asset class are concerned, the ebbing of yields globally during April-June this year seemed to suggest that markets had priced in the inevitability of monetary policy normalisation by systemic central banks, but the recent volatility has dispelled that comfort. Most emerging market currencies have depreciated, with retrenchment in capital flows amplifying the downswing. As macroeconomic conditions diverge further across countries, monetary policy actions and stances are getting dissonant, tightening global financial conditions and putting the global recovery further at risk.

60. The Indian economy has been treading a trajectory that diverges from the global situation. Bank credit is picking up, tax revenues are buoyant, exports are growing robustly and the current account balance is set to swing into a deficit on the back of strong import demand, but there are limits to decoupling. There are vulnerabilities too. The level of GDP in Q2:2021-22 is barely at the so-called pre-pandemic level of Q2:2019-20, which itself grew at the slowest pace in 6 years preceding it. Consumption spending is held back by households hesitant to incur discretionary expenditure. Private investment remains timid and is yet to participate in the recovery. Contact-intensive services are still convalescing from the wounds of the pandemic. In November, several high frequency indicators have slowed, suggesting that the second half of 2021-22 may not be the same as the first half and moderation in the recovery could set in.

61. On inflation, food inflation may ease with the usual winter softening, but core inflation will keep us awake, especially with the likely cost push from recent upward revisions of telecom tariffs and GST rates on clothing and footwear, the safe haven upswing in gold prices and the increasing likelihood of selling price revisions in respect of consumer durables, automobiles and the like by January 2022. India’s inflation developments reflect a scissor effect – rebound in demand colliding with supply bottlenecks; but shipping delays, delivery lags and semi-conductor shortages cannot last indefinitely and should certainly improve in the second half of 2022, as predicted by the IMF. The surge of pent-up demand should also normalise by then. Accordingly, elevated levels of inflation will persist till then, whether we like it or not, but not longer. By the projections, inflation in India will peak in the last quarter of this year and from there, it will moderate.

62. India is being lashed by global spillovers. The main conduit has been financial markets so far but the channels themselves are diversifying. The biggest risk of contagion is now from the new variant. Unless a clearer picture emerges on the near-term outlook, we must take guard and resume battle readiness again. In this highly unsettled environment, my vote for status quo on the policy rate and the accommodative stance as articulated in the resolution is fait accompli.

Statement by Shri Shaktikanta Das

63. Since the previous meeting of the MPC (October 6-8, 2021), domestic growth and inflation have unfolded broadly on projected lines, while the global environment has turned febrile. Risks stalking the global economy have amplified with rapid spread of the virus mutations, including the Omicron variant, leading to countries scrambling for restrictions. Concomitantly, sharp escalation in inflationary pressures across several major advanced economies is prompting their central banks to hasten winding down of their ultra-accommodative policies, which may impart volatility to the financial markets with associated spill overs for emerging market economies (EMEs) like India. These developments certainly have two major takeaways for central bankers. First, uncertainty is emerging as the only certainty with which central bankers will have to deal with in the period ahead. Second, since monetary policy is at an inflection point, the journey of monetary policy which is hardly smooth in the best of times, is going to get more challenging. These two factors necessitate judicious policy choices amidst trade-offs. Against this backdrop, let me set out my assessment.

64. The Indian economy is facing several headwinds emanating from global factors – some old ones getting prolonged compared with the initial assessment, coupled with new ones. The supply disruptions and other bottlenecks which were earlier anticipated to resolve by end of this year have gained additional shelf life stretching into 2022. Global trade, after rebounding strongly in the first half of 2021, is losing momentum on the back of stretched supply chain and logistics issues, shortages of key components and slowdown in key regions. The emergence of the Omicron variant may cast some shadow on the momentum of contact-intensive services that were just showing signs of recovery in recent months. The threat of Omicron is also imparting additional volatility to the financial markets.

65. While the Indian economy is on its way to achieve the projected growth of 9.5 per cent in 2021-22, there are still significant areas of concern. Private consumption – the mainstay of aggregate demand with a share of around 55 per cent – is languishing below its level recorded two years ago, suggesting that we still have a distance to go in nurturing a more durable recovery. Private sector capex remains sluggish even though pre-conditions for its acceleration have been engendered by increasing capacity utilisation, deleveraging of balance sheets and improved profitability of corporates. Based on the early results, capacity utilisation in the manufacturing sector increased to 68.8 per cent in Q2:2021-22 from 60.0 per cent in Q1:2021-22. As corporates get ready to invest, congenial financial conditions need to be in place to boost business sentiment.

66. As regards inflation, headline CPI after moderating sharply in September to 4.3 per cent, edged up in October to 4.5 per cent. On the domestic front, October saw unusually heavy rains, which led to loss of kharif crops as well as delayed harvest. This resulted in a flare up of vegetables prices. CPI fuel inflation continued to be in double digits with domestic LPG and kerosene prices being raised in response to increase in international prices. These price pressures in food and fuel resulted in a pick-up in CPI inflation in October despite large favourable base effects. Core inflation remained elevated.

67. Going forward, the heavy rainfalls in November are likely to keep vegetables prices elevated in the near-term; however, prices thereafter are expected to register seasonal declines on fresh winter arrivals. The recent supply side interventions by the Government would continue to restrain the pass-through of elevated international edible oil prices to domestic retail inflation. The outlook on cereals and pulses is also favourable with healthy progress of rabi sowing. Retail selling prices of fuel eased somewhat in early November with reduction in excise duty and VAT on petrol and diesel, which should lead to a durable reduction in inflation through both direct and indirect effects. This should also be supported by the fall in international crude oil prices observed towards end-November, albeit to the extent that it is passed on to the retail pump prices. The revision in mobile tariffs, however, would be an additional source of price pressures on core inflation from December 2021. Looking ahead, inflation is expected to moderate to 5.0 per cent in H1 of next financial year, remaining well within the tolerance band.

68. We, however, need to remain vigilant to incipient cost-push pressures to inflation as well as to the uncertainty imparted by Omicron. Its implication for inflation, going forward, are two-fold. First, increase in restrictions, if any, on activity and commerce to stymie COVID-19 spread could translate to continuing supply chain and logistics disruptions. Second, if the Omicron variant results in the onset of new waves of infection globally, this could derail the ongoing demand recovery. On the whole, at this stage it is too premature to gauge as to how the effects of the Omicron variant would pan out in the weeks and months ahead in terms of its effect on growth and inflation.

69. To sum up, there is growing uncertainty regarding the evolving global macroeconomic outlook. In the domestic front, even as the prospects for economic activity are improving, there is still a slack with key drivers like private consumption remaining well below their pre-pandemic levels. Given these uncertainties, continued policy support is warranted for a durable, broad-based and self-sustaining rebound, especially to nurture revival in sectors which are lagging and to safeguard those which are exposed to the evolving headwinds. In this scenario, it would be prudent to watch out for growth signals becoming well entrenched while remaining vigilant on inflation dynamics. There is also a necessity to have a firm understanding of the impact of the Omicron variant. The calibration and timing of a monetary policy response and preventing build-up of financial stability risks are very important in such an uncertain environment. Thus, I vote to keep the policy repo rate unchanged at 4 per cent and to continue with the same accommodative stance as spelt out by the MPC in its October 2021 meeting.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/1402

|