[Under Section 45ZL of the Reserve Bank of India Act, 1934]

The twenty ninth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held from June 2 to 4, 2021.

2. The meeting was attended by all the members – Dr. Shashanka Bhide, Senior Advisor, National Council of Applied Economic Research, Delhi; Dr. Ashima Goyal, Professor, Indira Gandhi Institute of Development Research, Mumbai; Prof. Jayanth R. Varma, Professor, Indian Institute of Management, Ahmedabad; Dr. Mridul K. Saggar, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Michael Debabrata Patra, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. Dr. Shashanka Bhide, Dr. Ashima Goyal and Prof. Jayanth R. Varma joined the meeting through video conference.

3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely:

-

the resolution adopted at the meeting of the Monetary Policy Committee;

-

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and

-

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting.

4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below.

Resolution

5. On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (June 4, 2021) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

Consequently, the reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

- The MPC also decided to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

6. Since the MPC’s meeting in April, the global economic recovery has been gaining momentum, driven mainly by major advanced economies (AEs) and powered by massive vaccination programmes and stimulus packages. Activity remains uneven in major emerging market economies (EMEs), with downside risks from renewed waves of infections due to contagious mutants of the virus and the relatively slow progress in vaccination. World merchandise trade continues to recover as external demand resumes, though elevated freight rates and container dislocations are emerging as constraints. CPI inflation is firming up in most AEs, driven by release of pent-up demand, elevated input prices and unfavourable base effects. Inflation in major EMEs has been generally close to or above official targets in recent months, pushed up by the sustained rise in global food and commodity prices. Global financial conditions remain benign.

Domestic Economy

7. Turning to the domestic economy, provisional estimates of national income released by the National Statistical Office (NSO) on May 31, 2021 placed India’s real gross domestic product (GDP) contraction at 7.3 per cent for 2020-21, with GDP growth in Q4 at 1.6 per cent year-on-year (y-o-y). On June 1, the India Meteorological Department (IMD) has forecast a normal south-west monsoon, with rainfall at 101 per cent of the long period average (LPA). This augurs well for agriculture. With the rise in infections in rural areas, however, indicators of rural demand – tractor sales and two-wheeler sales – posted sequential declines during April.

8. Industrial production registered a broad-based improvement in March 2021. While mining and electricity output surpassed March 2019 (pre-pandemic) levels, manufacturing did not catch up. The output of core industries registered a double digit y-o-y growth in April 2021, propelled by a weak base. Although GST collections were at their highest during April 2021, there are indications of moderation in May as reflected in lower E-way bills generation. Other high-frequency indicators – electricity generation; railway freight traffic; port cargo; steel consumption; cement production; and toll collections – recorded sequential moderation during April-May 2021, reflecting the impact of restrictions and localised lockdowns imposed by states with exemptions for specific activities. The manufacturing purchasing managers’ index (PMI) remained in expansion in May although it moderated to 50.8 from 55.5 in April due to a slowdown in output and new orders. The services PMI, which was 54.0 in April, entered into contraction (46.4) in May, after seven months of sustained expansion.

9. Headline inflation registered a moderation to 4.3 per cent in April from 5.5 per cent in March, largely on favourable base effects. Food inflation fell to 2.7 per cent in April from 5.2 per cent in March, with prices of cereals, vegetables and sugar continuing to decline on a y-o-y basis. While fuel inflation surged, core (CPI excluding food and fuel) inflation moderated in April across most sub-groups barring housing and health, mainly due to base effects. Inflation in transport and communication remained in double digits.

10. System liquidity remained in large surplus in April and May 2021, with average daily net absorption under the liquidity adjustment facility (LAF) amounting to ₹5.2 lakh crore. Reserve money (adjusted for the first-round impact of the change in the cash reserve ratio) expanded by 12.4 per cent (y-o-y) on May 28, 2021, driven by currency demand. Money supply (M3) and bank credit grew by 9.9 per cent and 6.0 per cent, respectively, as on May 21, 2021 as compared with growth of 11.7 per cent and 6.2 per cent, respectively, a year ago. India’s foreign exchange reserves increased by US$ 21.2 billion in 2021-22 (up to May 28) to US$ 598.2 billion.

Outlook

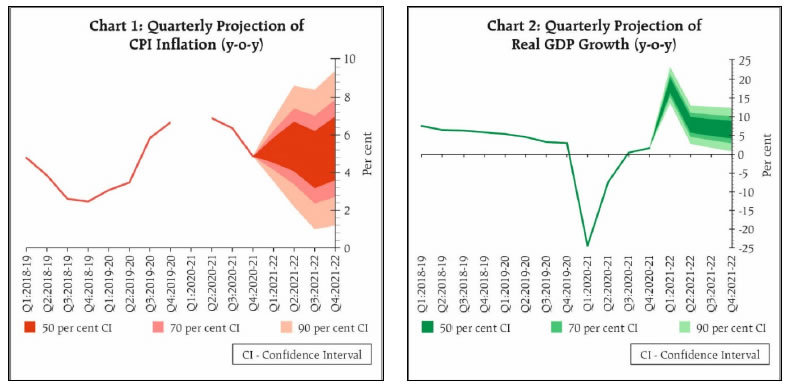

11. Going forward, the inflation trajectory is likely to be shaped by uncertainties impinging on the upside and the downside. The rising trajectory of international commodity prices, especially of crude, together with logistics costs, pose upside risks to the inflation outlook. Excise duties, cess and taxes imposed by the Centre and States need to be adjusted in a coordinated manner to contain input cost pressures emanating from petrol and diesel prices. A normal south-west monsoon along with comfortable buffer stocks should help to keep cereal price pressures in check. Recent supply side interventions are expected to ameliorate the tightness in the pulses market. Further supply side measures are needed to soften pressures on pulses and edible oil prices. With declining infections, restrictions and localised lockdowns across states could ease gradually and mitigate disruptions to supply chains, reducing cost pressures. Weak demand conditions may also temper the pass-through to core inflation. Taking into consideration all these factors, CPI inflation is projected at 5.1 per cent during 2021-22: 5.2 per cent in Q1; 5.4 per cent in Q2; 4.7 per cent in Q3; and 5.3 per cent in Q4:2021-22; with risks broadly balanced (Chart 1).

12. Turning to the growth outlook, rural demand remains strong and the expected normal monsoon bodes well for sustaining its buoyancy, going forward. The increased spread of COVID-19 infections in rural areas, however, poses downside risks. Urban demand has been dented by the second wave, but adoption of new COVID-compatible occupational models by businesses for an appropriate working environment may cushion the hit to economic activity, especially in manufacturing and services sectors that are not contact intensive. On the other hand, the strengthening global recovery should support the export sector. Domestic monetary and financial conditions remain highly accommodative and supportive of economic activity. Moreover, the vaccination process is expected to gather steam in the coming months and should help to normalise economic activity quickly. Taking these factors into consideration, real GDP growth is now projected at 9.5 per cent in 2021-22, consisting of 18.5 per cent in Q1; 7.9 per cent in Q2; 7.2 per cent in Q3; and 6.6 per cent in Q4:2021-22 (Chart 2).

13. The MPC notes that the second wave of COVID-19 has altered the near-term outlook, necessitating urgent policy interventions, active monitoring and further timely measures to prevent emergence of supply chain bottlenecks and build-up of retail margins. A hastened pace of the vaccination drive and quick ramping up of healthcare infrastructure across both urban and rural areas are critical to preserve lives and livelihoods and prevent a resurgence in new waves of infections. At this juncture, policy support from all sides – fiscal, monetary and sectoral – is required to nurture recovery and expedite return to normalcy. Accordingly, the MPC decided to retain the prevailing repo rate at 4 per cent and continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

14. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 4.0 per cent. Furthermore, all members of the MPC unanimously voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

15. The minutes of the MPC’s meeting will be published on June 18, 2021.

16. The next meeting of the MPC is scheduled during August 4 to 6, 2021.

| Voting on the Resolution to keep the policy repo rate unchanged at 4.0 per cent |

| Member |

Vote |

| Dr. Shashanka Bhide |

Yes |

| Dr. Ashima Goyal |

Yes |

| Prof. Jayanth R. Varma |

Yes |

| Dr. Mridul K. Saggar |

Yes |

| Dr. Michael Debabrata Patra |

Yes |

| Shri Shaktikanta Das |

Yes |

Statement by Dr. Shashanka Bhide

17. The strong recovery in economic activities registered in Q4: FY2021 raised expectations that the adverse impact of the Covid 19 pandemic is now behind us. The Provisional Estimates brought out by National Statistics Office (NSO) for 2020-21 on May 31 now place the real GDP growth at -7.3 per cent over the previous year, a lower rate of contraction than provided in the Second Advance Estimates. The year-on-year growth rates of key components of aggregate demand, Private Final Consumption and Government Final Consumption Expenditures, Exports and Gross Fixed Capital Formation registered substantial recovery in Q4 compared to the performance in the previous quarter. On the production side, construction sector registered double digit growth rate, year-on-year, in Q4. Data available on the performance of the corporate sector in Q4: FY2021 also shows improvement in sales realisations and Gross Value Added, particularly in the case of manufacturing sector. However, the subsequent second steep surge of the Covid 19 infections seen during April-May, led to far greater fatalities than in the previous wave and some disruptions of economic activities in the first two months of Q1: FY2022, which in turn have required re-assessment of the growth prospects in the immediate term.

18. The second wave of infections led to restrictions on the movement of people at a local level unlike the national level lockdown imposed during the first wave in 2020. But the fact that extent of the spread of the disease was large in many of the large cities also meant that commercial activities were disrupted in a significant manner. The rural areas were not insulated from the second wave to the extent it was the case during the first wave.

19. While data on the impact of the second wave of the pandemic is limited, qualitative data emerging from the surveys of households and enterprises suggest significant dent in the consumer and business sentiments. The survey of Consumer Confidence conducted by RBI in the last week of April and up to May 10, 2021 in 13 major cities in the country reveals a sharp rise in the percentage of respondents who perceive the current general economic conditions to be worse than a year back, compared to a similar survey conducted two months back. Importantly, 51.5 per cent of the respondents also say that they believe the general economic conditions would be worse a year-ahead. Early results of the quarterly Industrial Outlook Survey of the RBI for June 2021, show that in the case of the manufacturing sector, the summary index of current business conditions has declined for Q1: FY2022 and the index of expectations also has declined for Q2: FY 2022. These perceptions of business conditions point to the adverse economic conditions compared to the sentiments at the end of Q4: FY2021.

20. Further evolution of the economy would be affected by the decline in the spread of the disease on the back of adoption Covid appropriate behaviour by the population that increases protection from new infections. Acceleration in the vaccination program and availability of health care would be a key to boost the confidence of the consumers, workers and producers in the resumption of their economic lives. The projection of near-term economic growth, therefore, is conditioned by this unexpected shock from the second wave of the pandemic.

21. The global economic conditions in 2021 have been projected to be more favourable to trade and investment than in 2020, as the Advanced Economies are expected to regain the growth momentum. The Covid 19 pandemic is seen to be coming under control combined with fiscal stimulus measures to revive demand. However, the shadow of threat of the new strains of the virus and the slow progress of vaccinations globally will also limit the economic revival.

22. The initial impact of the second wave of the pandemic on the economy has been incorporated in the revised assessment of the GDP growth for FY2022 by many organisations and agencies. The median estimate of GDP growth for FY2022 from RBI’s Survey of Professional Forecasters carried out during May 2021 has declined to 9.8 per cent over the previous year from 11.0 per cent forecast in March 2021.

23. While the uncertainty over the short-term growth prospects has increased, there are also the positive triggers. The improved global demand conditions are expected to support the sustained improvement in export performance. The focus on improving capital expenditure in the central government budget also provides a stimulus to domestic demand. Agriculture is expected to contribute to economic growth based on a favourable monsoon. Response to these triggers by improvement in private consumption and investment spending will require the sustained reduction in the Covid 19 infections.

24. In this backdrop the projected growth of GDP in 2021-22 at 9.5 per cent, revised downward from the 10.5 per cent, projected in April 2021 will require continued fiscal and monetary policy support, besides other measures to enable expansion of economic activities and keeping the population safe from the pandemic.

25. The headline inflation rate for April 2021 is at 4.3 per cent, although fuel price index rose sharply by 7.9 per cent, year on year basis. The index of prices reflecting core inflation (excluding food and fuel) – which includes the effect of food and fuel prices indirectly through input linkages and that of transportation prices directly - increased by 5.4 per cent in April compared to 5.9 per cent in March 2021. The rising prices of fuel and global commodity prices push up the cost of production and distribution across supply chains. Besides the resumption of production across sectors that also create competitive pressures, easing of these price pressures will require more efficient operation of trade and logistics infrastructure, supported by easing of movement restrictions. Based on present trends, the projected headline inflation rate in 2021-22 at 5.1 per cent, is marginally higher than the projections in April 2021.

26. At this juncture, providing a policy environment supportive of sustained economic recovery from the second shock of the pandemic is necessary.

27. I vote in favour of keeping the policy repo rate unchanged at 4.0 per cent. I also vote in favour of continuing with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

Statement by Dr. Ashima Goyal

28. The human cost is incalculable in the country’s battle with the fearsome second wave of more infectious coronavirus variants. The economic cost, however, is likely to be limited. Compared to last year, the fall in demand far exceeds that in supply because of the decentralized structure of lockdowns that largely maintained inter-state goods movement and make possible calibrated, differentiated re-opening. Since vaccination in hot spots such as large cities and for corporates is likely to reach a critical mass by July-August normalization will be rapid. Although uncertainties remain regarding a possible third wave, vaccination cover in dense clusters will reduce its probability. The second wave peak in rural areas was in the slack season and is past. Sowing is likely to be normal with a good monsoon. Migrant labour is also available for work.

29. There are two major implications for monetary policy. First, since the fall in demand exceeds that in supply the output gap should widen, reducing demand side pressures on inflation. Second, a healthier supply-side combined with weak demand may damp firms pricing power and pass through, despite more concentration that increases it. In the past quarters output prices have risen with input prices and together with global commodity price rise and a low base, pushed WPI inflation into double digits. Firms have actually raised profit margins, even in a pandemic year. This may be partly due to low capacity utilization. They have not passed on a fall in wages and many other costs such as travel. Moreover, since normally the pass through from WPI to CPI headline is low and lagged, wage increases may remain muted, preventing persistent second round rise in inflation. The dominant current view is global price pressures are temporary and expected to reduce as supply chain disruptions and congestion are overcome. Moreover, uneven global recovery and uncertainties may somewhat restrain demand, despite the unprecedented stimulus given in a few major countries. Headline CPI, therefore, is widely predicted to remain within the MPC’s tolerance band, although seasonal and lockdown related spikes may occur.

30. But can the rise in household inflation expectations compared to March create persistence in inflation? Note, however, current surveys were conducted over 29th April to 11th May. Fresh coronavirus cases peaked at above 4 lakhs on 7th May. This was the period of highest fear and uncertainty that very likely affected consumer responses. A number of inconsistencies in responses also support this hypothesis. For example, inflation is expected to soften for all non-food groups, but is expected to increase in the aggregate. In the consumer confidence survey inflation is expected to reduce, albeit the level remains high. Therefore, robust inferences have to await surveys taken in more normal times.

31. The slump in consumer confidence in the second wave is slightly more than that in the first wave. It had, however, recovered to July 2019 levels in January 2021, and may show a similar V-shape this time. It is not yet clear if higher risk-aversion will dampen consumer demand more now or there will again be a desire to make up for forced abstention. But income and job loss, more indebtedness and impoverishment surely will shrink demand.

32. The MPC has moved to data-based guidance from time-based guidance. In times of such uncertainty, expectations and forecasts are less reliable. It is important, therefore, while remaining pre-emptive and forward looking, to wait for data on actual outcomes, watching for first signs of second round pass through in inflation as well as for alleviation on the supply-side. Over-reaction has to be avoided to minimize risks if expectations prove incorrect. Adjustment, therefore, has to be gradual but not too gradual as monetary policy acts with long lags.

33. At this juncture, since the output gap has widened and inflation is largely predicted to remain within the tolerance band, macroeconomic policy clearly has to further stimulate demand. The short-term real interest, however, is already negative and may be close to equilibrium levels, so it is liquidity that has to make additional contributions. Targeted schemes can smooth kinks in the yield curve ensuring that funds reach wherever required. Low demand is keeping credit growth low, with the excess durable liquidity parked by banks in the reverse repo so that broad money supply growth remains low at 9.9 per cent. The risk of excess money growth fuelling inflation is therefore minor as yet.

34. In the circumstances, I vote for keeping the policy repo rate unchanged and the stance accommodative as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while remaining watchful to ensure that inflation remains within the target going forward.

35. There is room for a supportive limited countercyclical rise in government deficits. This together with visibly better tax performance will prevent spikes in risk premium and help monetary policy keep real interest rates at levels that sustain the growth recovery. Growth rates that exceed the real interest rate bring down debt ratios over time1.

36. Recovering global growth has buoyed Indian exports supporting demand. But the asymmetric global recovery carries a potential threat of a recurrence of the taper tantrum. The beginnings of US exit from stimulus may provoke outflows from emerging markets. But India has the reserves to suit its interest rate policy to its domestic cycle instead of being forced to follow the US cycle. Moreover, at present there is some softening of US bond yields and the dollar is weakening, suggesting the exit may be smooth. A rise in inflation above the 2 per cent Fed target for a few months is unlikely to destabilize long run inflation expectations if inflation ruling below 2 per cent for many years after the global financial crisis could not do so. Moreover, there is the post taper learning that bond markets are less destabilized during exit if the Fed’s balance sheet is allowed to shrink very slowly as securities mature, while interest rates are raised only gradually with data that shows the recovery to be well established.

Statement by Prof. Jayanth R. Varma

37. The economic recovery that was visible in the early months of 2021 was arrested by the second wave of the pandemic which has been catastrophic in terms of lives lost. But the economic impact appears to have been less severe, and high frequency indicators provide some reason to hope that the economic recovery will resume soon as the second wave now appears to be well past its peak. However, ever since the onset of the pandemic, nowcasts and forecasts of economic growth have not been highly reliable. Moreover, there is a fear that the health shock is inducing high levels of precautionary savings that could depress demand for several quarters to come. All of this point to a need for monetary accommodation at this juncture to support economic recovery.

38. Turning to inflation, Indian inflation rates have been consistently well above the mid point of the tolerance zone for an extended period and are forecast to remain elevated for some time. Moreover, survey data and other indicators show that businesses have no difficulty in passing on cost increases to consumers, and are able to maintain (and even expand) their margins. The only source of comfort is that all the evidence at the moment suggests that inflation is being driven not by domestic demand, but by supply side factors including the global surge in commodity prices. This could change as the recovery gathers steam, and the MPC must be sensitive to the risk that inflation expectations could become entrenched if inflation remains elevated for too long. The MPC has been able to maintain monetary accommodation in the face of above-target inflation mainly because of its hard-earned credibility for successful inflation targeting. To maintain and enhance this credibility, the MPC needs to remain data driven so that it can respond rapidly and adequately to any unforeseen shocks that may arise in future.

39. Turning to the current policy statement, I believe that the balance of risk and reward continues to be in favour of monetary accommodation. Therefore, I support maintaining the policy rate at its current level, and I also support the accommodative stance.

Statement by Dr. Mridul K. Saggar

40. Let me provide an assessment of growth and inflation before discussing some policy trade-offs in the backdrop of decision at hand.

41. After a spike, daily new infections are now back at the levels that prevailed at the time of the last MPC meeting. Judging by the epidemiological models the wave will be flattened by end-June. Economic recovery is likely to ensue. With unclear probabilities and timings of any further waves, they are best kept as a risk factor rather than a baseline assumption.

42. The solace is that growth has not fallen off the cliff in Q1 as it did a year ago. Work-related Google and Apple mobility indicators, GST E-way bills issuances and wholesale and retail digital payments, despite sequential drops, have stayed much higher on a year-on-year basis than last year. This lends support to the Q1 growth projection that implies a smaller quarter-over-quarter decline of 18.0 per cent compared with 29.7 per cent a year ago. It is possible that that initial GDP estimates do not provide full visibility and the impact on informal and unorganised economy may be deeper. Also, if the economy does expand by 9.5 per cent this year, the output level in 2021-22 will be just 1.6 per cent higher than in the pre-pandemic year 2019-20. These are two reasons against pulling out policy support to growth prematurely. However, while monetary and fiscal policies can lend counter-cyclical support, a sustained revival will ultimately depend on health policies and how the limited fiscal space is used to augment potential output by tagging spending to capex and structural reforms.

43. World economy is picking steam and global growth beyond 6 per cent is possible powered by the strong bounce back in the U.S. and steady acceleration in the euro area. If the expected slowdown in China in the sequential quarters is arrested through policy interventions the global growth momentum can turn breathtaking. However, this would also carry the risk of increased passthrough from global inflation. Upside on net exports may also be limited by worldwide container shortages, though some moderation in capesize freight rates in May shows that efforts to decongest ports are working. Government directly produces about a fifth of the GDP and its’ spending will matter for growth. This year’s budget aims to shift spending further from consumption to investment. This augurs well for growth from a multi-year perspective given its much higher multiplier. Lastly, monsoon forecast at 101±4% of LPA, with a reasonably good spatial and temporal distribution, has diminished the downside risks though a clearer picture will be known only by the next MPC meeting in August.

44. Coming to inflation, the baseline suggests that inflation will stay within the tolerance band, though consistently above target. It may remain close to the upper tolerance level till August but recede thereafter if Kharif crop shapes well and if global commodity price pressures subside by then. Risks of elongated commodity pressures exist in face of piping-hot global economy but demand substitution across commodities supported by the ESG push might change relative prices thus halting or reversing the rising prices of crude oil, iron ore and steel. While prices of crude oil, pulses, edible oils and cotton are likely to put pressure on domestic inflation they can be contained by quick fiscal or supply-side responses.

45. Let me come to some policy trade-offs we face. First, as a baseline, inflation is expected to stay elevated from the target but below the upper tolerance level through the year. However, the probability distribution indicated in the fan chart shows that risks of breaching the upper tolerance level are not insignificant. But for the extra-ordinary circumstances that prevail, we would have moved to a neutral stance long back. I had earlier in my statements starting October 2020 stated that output gap will close towards the end of 2021-22. The second wave is likely to push back normalisation a bit but not a lot. A range of filtering techniques still suggest closure of output gap as a ratio of level of potential GDP by the end of this year but we cannot rely on them mechanically as these techniques have high dependence on the end points. Therefore, we need to make some allowance for the uncertainty around that. We can continue to support growth for now as the flexible inflation targeting framework allows temporary deviation from the target so long as inflation is expected to be within tolerance bands. There are risks to inflation as there have been general price pressures at the WPI level and its inflation as well as its momentum is at its highest for the index with the current base. However, the passthrough of cost-push inflation at the retail level has stayed muted amid demand deficiency. Also, credit growth remains anaemic and nominal broad money growth as well as money multiplier adjusted for reverse repo remain low. So, support to growth can continue at this juncture. In my view, clear signs of generalisation in CPI inflation setting in could be a tipping point where growth-inflation dynamics could alter. Also, with a further rise in elevated inflation expectations, policy may need to respond if these expectations are becoming unhinged. While the odds are that we can avert this as inflation softens back in H2, the uncertainties ahead provide a rationale to avert any time-based guidance, especially as transmission lags exist.

46. Secondly, we need to consider the policy trade-off between leaving policy rate unchanged and correcting it at some point for the negative real rates that have persisted for a spectrum of interest rates thus taxing savers. The frontier of the macroeconomics, especially in terms of Heterogenous Agents New Keynesian (HANK) models provide a good reason to think that not all savers may necessarily be worse off when central banks push down the interest rates. These models capture additional effects that are heterogenous. As demand increases with monetary expansion, firms ramp up production. This improves their survival rate amid a deep shock like the pandemic. It also protects job losses and pushes more wages and salaries in the hands of households most of whom may get more than compensated for a drop in their interest incomes on saving. With a large proportion of low income and other liquidity constrained households in India, these indirect second-round effects could turn very significant. Furthermore, low interest rates create space for fiscal action in support of growth. These multiplier effects are the raison d’etre for extant monetary and liquidity accommodation. My judgment is that the policy has worked well in dampening scarring, limiting job losses, generating wealth effects from higher asset prices, thus supporting incomes and consumption under some very difficult circumstances. Its continuation for long, though carries the hazard of unintended consequences as incomes may instead fall in real terms worsening its distribution as well. Monetary accommodation, when coordinated with expansionary fiscal policy has a greater impact on output gap but may also cause slope of the Phillips curve to turn steeper over time.

47. Nevertheless, retail inflation is not yet predominantly demand-driven and to accept output sacrifice at this stage may not be the best policy choice. Taking full cognisance of these policy trade-offs, I judge that withdrawing support to growth at this stage may be premature as it may dampen second-round effects. I, therefore, vote for retaining the policy rate at present level and continue with the stance as spelled out in resolution.

Statement by Dr. Michael Debabrata Patra

48. I vote to maintain status quo on the policy rate and on the stance of policy.

49. The growth-inflation trade-off and consequently, policy choices have shifted towards increasing accommodation. High frequency indicators for April and May 2021 point to a stalling of the recovery that was underway from the second half of 2020-21. Unlike in the first wave, supply conditions have remained relatively resilient in the second wave, but aggregate demand barring net exports has been dented and needs counter-pandemic policy support. Even the turnaround in net exports is fragile and heavily dependent on the strength of the vaccination- propelled revival in external demand, which may be partially offset by the terms of trade loss on account of the rise in international commodity prices, particularly crude oil.

50. April’s inflation afforded a window of respite, and more recent information suggests that price pressures on some constituents of the food category may remain benign in the near-term in spite of the usual pre-monsoon upturn. Input pressures will work towards keeping core inflation elevated, while some food prices will reflect persisting demand-supply imbalances, but in the absence of strong demand, the pass-through to retail inflation is likely to be incomplete and delayed, especially with respect to prices of services. The outlook for energy inflation is the main upside risk, especially as the timing and magnitude of reflation of global demand to pre-pandemic levels is uncertain. This warrants close and continuous watching, with preparedness to take countervailing action in the form of duty/tax reductions. The recent initiative of a Group of Ministers monitoring supply conditions with greater intensity is a welcome step in the right direction and should be matched by proactive actions as necessary to deflect imported input costs from adding to inflationary pressures.

51. The MPC has created the necessary conditions for supporting growth by maintaining the policy rate at its lowest level ever. It has also provided credible forward guidance matched by actions, committing to a path for future short-term interest rates that should re-engineer the recovery that was dented by the impact of the second wave of COVID-19, given the limited headroom from inflation remaining aligned with the target in April and forecast to stay within the tolerance band going forward. The onus is on the Reserve Bank to operationalize the MPC’s guidance on an ongoing basis by ensuring congenial financial conditions across the system as well as for specific sectors, instruments and institutions. With credit growth remaining subdued despite monetary transmission being reasonably full, the Reserve Bank is galvanising market-based channels of financing as well as off-market channels such as refinancing institutions. It is also proactively engaged in operations that convey the monetary policy stance directly across the term structure of interest rates. By keeping the policy rate unchanged and by persevering with the accommodative stance in this meeting, the MPC creates the space for further easing of financial conditions by the Reserve Bank.

Statement by Shri Shaktikanta Das

52. When we last met in early April, the second wave of COVID-19 infections had started increasing but was still restricted to a few states. In the subsequent weeks, however, the surge in new infections turned severe and broad-based both in its spread across states and in the intensity of the increase, putting enormous pressure on the health system with heavy toll on human lives. The lockdown restrictions and containment measures undertaken by the states have led to a significant moderation of new infections and active cases; at the same time, it has taken some toll on the economy, as reflected in high-frequency economic and mobility indicators. We have now started seeing a phased relaxation of the restrictions in some states and can expect activity across the country to normalise from the beginning of July, if this trend persists.

53. The indicators of rural as well as urban demand suggest that economic activity was normalising and gaining a strong foothold in Q4:2020-21 with broad-based recovery driven by revival in real estate, manufacturing, construction and trade and financial services. With decline in infections, there were nascent signs of revival in the capex cycle during Q4:2020-21 as reflected in indicators like steel consumption; cement production; imports and production of capital goods. The recovery also got reflected in the strong print of the real gross value added (GVA) growth for the same quarter. This momentum in activity got abruptly disrupted with the onset of the second wave.

54. The infection containment efforts this time around were localised and calibrated, which allowed manufacturing and industrial activity to operate in varying degrees across states during this period. At the same time, businesses and supply chains have increasingly adapted to working in the pandemic and restricted environment. Also, the reverse migration of labour to villages has been muted relative to last year and inter-state movement of goods continues smoothly. Overall, it is expected that the loss in momentum of activity could be temporary and restricted to the first quarter of 2021-22.

55. Going forward, agriculture is expected to be the bright spot in the current year as well after remaining the fulcrum of growth during 2020-21. The upward revision of monsoon forecast with good spatial distribution augurs well for this expectation. Further, exports have exhibited resilience in recent months and with global recovery strengthening, especially in India’s key export destinations, it is anticipated that net exports would remain a propellant of growth in the current year. Enhanced and targeted policy support to exports can buttress this process further. The central government capex, which is budgeted to expand at a robust pace for 2021-22 (overall capital expenditure is budgeted to increase by 30.5 per cent within which capital outlay is budgeted to increase by 63.4 per cent) along with infrastructure pipeline, should reignite investment cycle once restrictions are eased. As the vaccination coverage expands, the pent-up demand for contact-intensive services is likely to rebound sharply. They should also get a leg up from the on-tap liquidity window from the Reserve Bank for these sectors. Domestic monetary and financial conditions remain highly accommodative and are expected to continue to be so in view of the MPC’s forward guidance. Taking all these factors into account, economic activity can be expected to recover from Q2:2021-22 onwards and gather pace in H2:2021-22 (October-March). For the full year, however, with the dent in activity during Q1:2021-22, the projected growth for 2021-22 is 9.5 per cent instead of 10.5 per cent projected earlier.

56. Over the last two months, inflation evolved broadly in line with our expectations. Headline inflation moderated to 4.3 per cent in April from 5.5 per cent in March. Large base effects played a crucial role and inflation sobered across food as well as core groups. A softening inflation print provides some relief and policy space enabling the Reserve Bank to step up liquidity infusion into the system to provide further support to the weak domestic economy in line with the MPC’s stance of reviving and sustaining growth on a durable basis. Moreover, the fragile demand conditions could help limit the pass-through of input cost pressures across manufacturing and services to output prices. Going forward, CPI inflation for 2021-22 is projected to be at 5.1 per cent, which is well within the mandated tolerance band of 2-6 per cent; however, we would need to keep a close watch on the evolving trajectory considering the uncertainties, both on the upside and downside, to the baseline path. Given the predominant role of supply side factors in the recent inflation movements, active and timely supply side policy measures with regard to petrol and diesel, edible oil and pulses, among others, would be critical to bring about a durable softening of price pressures.

57. Overall, the second wave of COVID-19 has altered the near-term outlook, and policy support from all sides – fiscal, monetary and sectoral – is required to nurture recovery and expedite return to normalcy. The dent on economic activity due to the second wave of the virus has necessitated the continuation of monetary measures to support the process of economic recovery to make it durable. I therefore vote for a pause on the repo rate. At the same time, there is a need to strengthen forward guidance by stressing the aspect of revival of growth. Thus, the emphasis should be to continue with accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. In this context, the phrase ‘to revive’ needs to be brought in so as to strengthen the forward guidance and demonstrate the unambiguous commitment of the MPC to revive and sustain the growth process. In fact, focus on revival and sustenance of growth is the most desirable policy option while of course remaining watchful of the inflation trajectory.

58. Going forward, the pace of vaccination and the speed with which COVID-19 second wave can be brought under control will have considerable bearing on the evolving growth as well the inflation trajectory. The Reserve Bank remains committed to undertake pro-active conventional and unconventional measures and to effectively channelling the systemic liquidity to alleviate stress of critical sectors which have borne the brunt of the second wave. In addition to liquidity provided under G-SAP operations, the Reserve Bank will continue to conduct other regular market operations to ensure that liquidity and financial conditions remain congenial, consistent with the accommodative stance of the monetary policy.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/390

|