5.1 The government securities market is at the core of financial markets in most countries. It deals with tradeable debt instruments issued by the Government for meeting its financing requirements.1 The development of the primary segment of this market enables the managers of public debt to raise resources from the market in a cost effective manner with due recognition to associated risks. A vibrant secondary segment of the government securities market helps in the effective operation of monetary policy through application of indirect instruments such as open market operations, for which government securities act as collateral. The government securities market is also regarded as the backboneof fixed income securities markets as it provides the benchmark yield and imparts liquidity to other financial markets. The existence of an efficient government securities market is seen as an essential precursor, in particular, for development of the corporate debt market. Furthermore, the government securities market acts as a channel for integration of various segments of the domestic financial market and helps in establishing inter-linkages between the domestic and external financial markets.

5.2 The government securities market has witnessed significant transformation across countries over the years in terms of system of issuance, instruments, investors, and trading and settlement infrastructure. It has grown internationally in tune with the financing requirements of Governments. The fiscal discipline exercised by many countries in recent years has restricted the size of the market. Accordingly, countries have focussed on improving trading liquidity of the market through various measures. Many countries in the recent past have pursued a strategy of managing the cost of Government borrowing in the medium to long-term so as to reduce the rollover risk and other market risks in the debt stock, although this may entail higher debt service costs in the short run. Historically, in most countries, the central banks as managers of public debt have played a key role in developing the government securities markets. Although debt management authorities are increasingly being established outside the central banks in various countries, central banks continue to play a major role in developing the trading and settlement infrastructure of the government securities market.

5.3 The evolution of the government securities market in India has been in line with the developments in other countries. Slow development of the market in the 1970s and the 1980s was shaped by the need to meet the growing financing requirements of the Government. This essentially resulted in financial repression as progressively higher statutory requirements were stipulated, mandating banks to invest in government securities at administered interest rates. Although this captive financing provided low cost resources to the Government, it impeded the development of the market and distorted the interest rate structure. Furthermore, such arrangements, along with automatic monetisation of Government deficits, hampered the conduct of monetary policy.

5.4 Recognising the need for a well developed government securities market, the Reserve Bank, in coordination with the Government, initiated a series of measures from the early 1990s to deregulate the market of administered price and quantity controls. Consequently, the government securities market has witnessed significant transformation in various dimensions, viz., market-based price discovery, widening of investor base, introduction of new instruments, establishment of primary dealers, and electronic trading and settlement infrastructure. This, in turn, has enabled the Reserve Bank to perform its functions in tandem with the evolving economic and financial conditions.

5.5 Wide ranging reforms in the government securities market were largely undertaken in response to the changing economic environment. Increased borrowing requirements of the Government, stemming from high fiscal deficits, had to be met in a cost effective manner without distorting the financial system. The underlying perspective of the reform process was, therefore, to raise government debt at market related rates through an appropriate management of market borrowing. There was also a need to develop a benchmark for other fixed income instruments for the purposes of their pricing and valuation. An active secondary market for government securities was also needed for operating monetary policy through indirect instruments such as open market operations and repos. Reforms, therefore, focussed on the development of appropriate market infrastructure, elongation of maturity profile, increasing the width and depth of the market, improving risk management practices and increasing transparency.

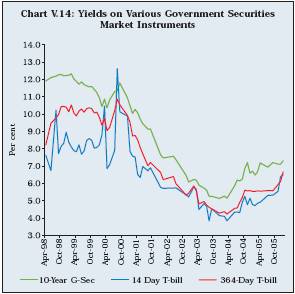

1 Governments issue securities with maturities ranging from less than a year to a very long-term stretching up to 50 years. Typically, short-term maturities up to one year, viz., Treasury Bills, form a part of the money market and facilitate the Government's cash management operations, while bonds with maturities more than a year facilitate its medium to long-term financing requirements. This chapter discusses developments with respect to bonds with maturities more than a year. Treasury Bills being short-term instruments are covered in Chapter III.

5.6 As stipulated under the Fiscal Responsibility and Budget Management Act, 2003, the Reserve Bank has withdrawn from participating in the primary market for government securities from April 1, 2006. The increasing move towards fuller capital account convertibility as recommended by the Committee on Fuller Capital Account Conver tibility (FCAC) (Chairman: Shri S.S. Tarapore) would necessitate measures that promote greater integration of the domestic financial markets with global markets. The deepening of the government securities market is, therefore, essential not only for transmission of policy signals but also for developing the derivatives market which would meet future challenges thrown up by further liberalisation of the capital account. Moreover, an environment of freer capital flows will also necessitate widening of the government securities market with further persification of the investor base

5.7 Against this backdrop, this chapter traces the development of the government securities market in India since the early 1990s, in order to identify the key issues that need to be addressed to meet the emerging challenges. The chapter is organised in six sections. Section I sets out the theoretical underpinnings, and principles and policy strategy for developing a deep and liquid government securities market. Section II presents international experiences in terms of key features of the government securities market in developed and developing countries. Section III outlines the developments in the government securities market in India since the early 1990s and the role played by the Reserve Bank in shaping it. An assessment of the government securities market in terms of various indicators is presented in Section IV. Drawing from the lessons from international experiences, Section V raises the key issues that need to be addressed for enabling the government securities market to play a more effective role in the emerging scenario. The final section presents concluding observations.

I. ROLE OF THE GOVERNMENT SECURITIES

MARKET

Theoretical underpinnings

5.8 The supply of government securities is generally exogenous to the market, determined mainly by the fiscal policy of the Government. The demand for government securities may be fragmented into several components implying that the demand curve is not uniformly downward sloping, but is rather kinked (Commonwealth of Australia, 2002). For instance, the demand by investors such as insurance companies and superannuation funds is in the nature of ‘buy and hold’ as the revenue streams from government securities generally match with their liability payment stream. These investors may have very few substitutes and, hence, their demand is less price sensitive. Mandated investments in government securities by banks and other institutions would also fall into the category of ‘buy and hold’. The demand from other investors in government securities is more for active trading and portfolio management. These investors may have many substitutes for government securities and, hence, their demand is generally more price elastic. The overall demand elasticity is, therefore, determined by the balance between these two groups of investors. Greater the share of active investors, higher is the demand elasticity or price sensitivity of government securities. Increased volume of government securities may increase concerns of a default by the Government which may affect the risk characteristics of the instrument. This may result in a fall in prices as yields steepen. At the other end of the spectrum, very limited supply of government securities may generate concerns over liquidity. Illiquidity premium can then drive down the prices, although there could be some resistance to the downward bias, if ‘buy and hold’ investors dominate the market. Thus, very high volumes as well as very low volumes of government securities may result in a fall in prices of government securities.

5.9 Activity in the government securities market can affect overall investment in the economy in two ways. First, it may adversely affect private investment by directly competing for the limited resources. As the interest rate on private bonds is determined by the usual downward sloping demand and upward sloping supply curves, the interest rate in the economy would be determined by the combined demand for and supply of government securities and private bonds. An increase in the supply of government securities in the face of high budget deficits would drive down their prices, leading to a substitution of private bonds with government securities, particularly, by investors whose demand is driven by trading and portfolio management requirements. This phenomenon is often described as ‘crowding out’.

5.10 Second, the government securities market can also have a positive influence on private investment by enabling the development of private bond market in two ways: (i) by putting in place a basic financial infrastructure, including laws, institutions, products, services, repo and derivatives markets; and (ii) by playing a role as an informational benchmark. A single private issuer of securities would never be of sufficient size to generate a complete yield curve and his securities would not be riskless because only supply of government securities and private bonds. An increase in the supply of government securities in the face of high budget deficits would drive down their prices, leading to a substitution of private bonds with government securities, particularly, by investors whose demand is driven by trading and portfolio management requirements. This phenomenon is often described as ‘crowding out’.

5.10 Second, the government securities market can also have a positive influence on private investment by enabling the development of private bond market in two ways: (i) by putting in place a basic financial infrastructure, including laws, institutions, products, services, repo and derivatives markets; and (ii) by playing a role as an informational benchmark. A single private issuer of securities would never be of sufficient size to generate a complete yield curve and his securities would not be riskless because only the Government has the power to print domestic currency (Herring and Chatusripitak, 2000). Thus, the yield curve of government securities serves as a public good in financial markets (Box V.1).

Box V.1

Role of Government Securities Yield Curve as a Public Good

Yield curve, also known as term structure of interest rates, is the representation of zero coupon yields of a series of maturities at a point of time. It is constructed by plotting the yields against the respective maturity periods of benchmark fixed-income securities. The yield curve is a measure of market’s expectations of future interest rates, given the current market conditions. Securities issued by the Government are considered risk-free, and as such, their yields are often used as the benchmarks for fixed-income securities with the same maturities.

Graphic Representation of a Normal Yield Curve

The difference between short and long ends of the yield curve (spread) determines the shape of the curve which is an important indicator of the expected performance of the economy and inflation. Since the government securities yield curve represents the risk-free interest rates, it is used for pricing other instruments of various maturities. The yield

The difference between short and long ends of the yield curve (spread) determines the shape of the curve which is an important indicator of the expected performance of the economy and inflation. Since the government securities yield curve represents the risk-free interest rates, it is used for pricing other instruments of various maturities. The yield curve has informational value to bond issuers for pricing as well as timing of their issue depending on the expected performance of the economy. Investors can also use the curve in choosing the right tenor of investment. For overseas investors, expected performance of different countries could be compared by looking at the respective yield curves to make investment decisions.

Most other interest rates are measured on the basis of the government securities yield curve, viz., credit curve and swap curve. Similarly pricing of other financial instrument uses the government securities yield curve in some form or the other. Thus, the yield curve acts as a kind of public good that is used constantly by participants in the financial system.

The efficiency of the yield curve as a public good is enhanced under the following two conditions. First, macroeconomic volatility, especially inflation volatility, must be low so that a nominal yield curve is informative about the real cost of borrowing. Second, the government must issue a sufficient volume of debt. Yield is described as an apparatus which allows abstraction of irrelevant factors and focuses on factors relevant for interest rate risk on portfolios (Krstic and Marinkovic,1997).

The fact that the yield curve acts as a public good enjoins upon all participants, in particular the regulators, the responsibility of ensuring that it is free from any undesirable and manipulative influence, as this would lead to a loss in its informational value and result in market inefficiency brought about by incorrect pricing of other financial instruments.

5.11 One of the key features of development of the government securities market is the evolution of yield curve over a reasonably long period. The upward sloping yield curve, which is considered to be the usual term structure, may reflect either the presence of interest rate risk premium or the so called Hicksian liquidity premiums, or it may simply reflect the market’s anticipation about the upward trend in the general level of interest rates over the period. Theoretical analysis confirms that in an efficient market, yield curve will solely depend upon the market’s response to collective beliefs about future interest rate movements, i.e., interest rates derived from the prevailing term structure of interest rates are correct forecast of future interest rates. Thus, development of the government securities market is essential for establishing the risk-free benchmarks in financial markets and ensuring their functioning in an efficient manner.

Significance of the Government Securities Market

5.12 The need to develop the government securities market emerges from the three roles it seeks to play, i.e., for the financial markets, for the Government and for the central bank (Reddy, 2002). As alluded to earlier, the government securities market serves as the backbone of fixed income markets through the creation of risk-free benchmarks of a sovereign borrower. Ipso facto, it acts as a channel of integration of various segments of the financial market. The government securities market constitutes a key segment of the financial market, offering virtually credit risk-free highly liquid financial instruments, which market participants are more willing to transact and take positions. The willingness of market participants to transact in government securities, in turn, imparts liquidity to these instruments, which benefits all segments of the financial market. Consequently, government securities are used by dealers as a major hedging tool for interest rate risk and as underlying assets and collateral for related markets, such as repo, futures and options (BIS,1999). Furthermore, large borrowings by the Government also provide an impetus to the development of the bond market.

5.13 From the perspective of an issuer, i.e., the Government, a deep and liquid government securities market facilitates its borrowings from the market at reasonable cost. A greater ability of the Government to raise resources from the market at market determined rates of interest allows it to refrain from monetisation of the deficit through central bank funding. It also obviates the need for a captive market for its borrowings. Instead, investor participation is voluntary and based on risk and return perception. A developed government securities market provides flexibility to the manager of public debt to optimise maturity and cost of even a lumpy government borrowing.

5.14 For the central bank, a developed government securities market allows greater application of indirect or market-based instruments of monetary policy such as open market (including repo) operations. A greater recourse to the market by the Government for meeting its funding requirements expands the eligible set of collaterals, thereby enabling the central bank to conduct monetary policy through indirect instruments. The expanding quantum of eligible collaterals has impar ted flexibility to central banks of many developing economies in their conduct of monetary policy, especially in sterilising the capital flows. As a part of reforms, even if the central bank’s participation in the primary market of government securities is phased out, the stock of government securities in the financial system would continue to enable the central bank to re-balance its portfolio through participation in the secondary market.

5.15 The government securities market, which is often the predominant segment of the overall debt market in many economies, plays a crucial role in the monetary policy transmission mechanism. Thus, irrespective of whether the central bank acts as manager of public debt or not, there are three main channels through which government debt structure might influence monetary conditions, viz., quantity of debt, composition of debt and ownership of debt (Box V.2).

Principles and Policy Strategy for a Liquid Market

5.16 In the aftermath of financial crises in the late 1990s in many economies, a consensus emerged on the need to develop deep and liquid financial markets, especially government securities markets. Studies suggested that the size is a key determinant of liquidity of the government securities market (McCauley and Remolona, 2000). A critical issue in this regard is trading liquidity, i.e., the ability of the market to execute transactions at short notice, low cost and with little impact on price (Lagana et al., 2006). The extent of liquidity in a market is usually captured by any or all of the four indicators, viz., width (width of the bid-ask spread), depth (the ability to carry out large trading without significant changes in price levels), immediacy (the ability to carry out large trading promptly without significant changes in price levels) and resilience (the ability of prices to quickly return to normal) (Harris, 1990). The Bank for International Settlements (BIS) identified four interrelated general principles for designing deep and liquid markets (Box V.3).

5.17 A five-pronged policy strategy can be pursued to promote liquidity in the government securities market (BIS, op.cit). First, there is a need to pursue a coherent public debt management strategy whereby distribution of government securities across various maturities and frequency of their issuances are modulated appropriately so as to facilitate sufficient supply of instruments for enhancing market liquidity. This can be ensured through large size of issuances, which, by creating of a homogeneous stock with a common maturity date, enhances liquidity. Alternatively, even where the government’s borrowing requirement is fixed, a debt manager can still enlarge the size of issuances of specific securities as demanded by investors at ‘key maturities’ across the yield curve by reducing the number of original maturities and/or reducing the frequency of issuances. A standard practice to enlarge the issue size, however, is to conduct regular reissuances of identical securities in several consecutive auctions instead of a single auction. Buyback of illiquid or older securities may also enable large sized issuances.

Box V.2

Government Debt Structure and Monetary Conditions

The absolute size of Government borrowings, especially when the financial markets are underdeveloped, often raises concerns about public debt management as there could be recourse to short-term financing from the central bank leading to monetary expansion. However, as the public debt/GDP ratio declines and government securities market develops with introduction of new instruments (like index-linked gilts), new issuing techniques (such as auctions) and improved market infrastructure, practical concerns about debt management impinging on monetary control get reduced. For instance, in the United Kingdom, a steady decline in the debt/GDP ratio and the emergence of a new structure in capital markets, after reforms of the London securities market in 1986, alleviated many of these concerns.

The composition of debt in terms of maturity pattern may also influence the conduct of monetary policy. One view is that monetary authorities may keep interest rates low when there is large short-term debt so as to reduce the rollover cost. A contrary view is that they may react more aggressively to inflationary shocks when maturity structure of debt is short so as to minimise the future rollover cost resulting from higher expected inflation and higher future nominal interest rates. The Government’s decision to issue short versus long maturity debt, or conventional versus index-linked debt may affect real yields, depending upon the substitutability of the instruments, thereby affecting the interest sensitive sectors of the economy.

The central policy concern about the ownership of public debt is related to the composition in terms of holding by banks and non-banks. Several empirical studies, using data mainly from the United States, found that increased debt issuances could lead to increase in bank holdings of debt. New issues of debt taken up by banks act as a substitute for lending to the private sector and, therefore, reduce the supply of bank credit to it. During monetary tightening, however, banks would extend loans to the private sector by running down their holdings of government debt. Thus, banks’ holding of public debt acts as a buffer. The experience in the United Kingdom was, however, contrary as the available evidence found that debt sales to banks had only a small impact on either money supply growth or bank lending.

Source:

Bank of England. 1999. “Government Debt Structure and Monetary Conditions.” Quarterly Bulletin, November.

5.18 Second, as taxes increase the transaction costs and hinder market liquidity, there is a need to weigh the potential increase in tax revenue against the potential decline in market liquidity. The liquidity impairing effect of transaction tax, however, could be mitigated by exempting the active market participants.

5.19 Third, there is a need to enhance transparency of issuers, issue schedule and market information. Greater transparency by Governments in furnishing of information plays an important role in improving liquidity of government securities. Adherence to a regular issuance cycle and pre-announcement of issue schedule provide an opportunity to investors to plan their portfolio management. In this regard, the existence of ‘when issued’ trading in government securities enables better market acceptability of issuances with availability of time between announcement and actual auction dates. A greater degree of transparency observed by market par ticipants also improves market liquidity. Dissemination of market information on a real time basis, without disclosing identity of market participants, narrows bid-ask spreads and improves market liquidity.

5.20 Fourth, standardisation, robust trading rules and safe infrastructure reduce transaction costs. Safety in trading and settlement is a pre-requisite for better liquidity. It is desirable to shorten settlement lags to T+3 or still shorter and adopt delivery-versus-payment (DvP) practices in the gover nment securities market. Standardisation of trading and settlement practices effectively enlarges supply of securities by removing fragmentation. It also encourages foreign participation. The permission to dealers to carry short sales also improves market liquidity as they can respond to customers’ buy orders quickly.

Box V.3

Principles of a Deep and Liquid Government Securities Market

A few general inter-related principles emerge from the experience of the mature markets that can guide the creation of deep and liquid government securities markets in countries after due adjustment to suit particular market situations (BIS, 1999). First, there is a need to maintain a competitive market structure in the government securities market to facilitate efficient price discovery. A government security, like any financial instrument, can be traded through a wide variety of mechanisms like over-the-counter (OTC) markets, organised exchanges and other platforms which cannot be placed in either of these categories. A fundamental strategy is to infuse competition among dealers which would narrow bid-ask spreads and increase liquidity of the market. In the case of exchanges, even when their number is limited, dynamic competition between the leading exchange and other exchanges, and between the OTC market and organised exchanges contribute to market liquidity. Thus, it is necessary to maintain a ‘contestable market’ where the dominant market participants can be challenged by new entrants if monopolistic or oligopolistic practices develop.

Second, the government securities market needs to have a low level of fragmentation offering instruments which have high degree of substitutability. Market liquidity tends to be enhanced when instruments can be substituted one for another since the market for each of them becomes less fragmented. A high degree of substitutability enhances trading supply of securities which facilitates in meeting the transaction demand. However, there is also a need to have some degree of heterogeneity in instruments for catering to specific investor needs. The trade-off between homogeneous product of large volume and some heterogeneity can be resolved by having a system of issuing government bonds at several ‘key maturities’ from the short end to the long end of the yield curve. Third, liquidity of the government securities market can be improved by lowering transaction costs, which include taxes, cost of sustaining necessary infrastructure and compensation for liquidity provision services. Higher transaction costs widen the gap between the effective price received by sellers of the instrument and that paid by buyers, thereby making it difficult to match sell and buy orders. This leads to low market liquidity. Some transaction costs, however, are inevitable such as those associated with ensuring sound payment and settlement infrastructure and improving overall robustness of the market. Thus, transaction costs need to be minimised as long as this does not reduce the security of the market in question. Fourth, there is a need to ensure a sound, robust and safe market infrastructure comprising (i) payment and settlement systems; (ii) the regulatory and supervisory framework; and (iii) market monitoring and surveillance. This increases the resilience of the government securities market against external shocks and contributes to continuous price discovery, thereby enhancing market liquidity.

Finally, there is a need to promote heterogeneity of market par ticipation in terms of transaction needs, risk assessments and investment horizons to promote liquidity in the government securities market. Furthermore, apart from varied domestic investor base, there is also a need to permit foreign participants. Non-residents may have risk appetite different from that of residents, which would prompt them to react differently to new information. However, liberalisation to encourage foreign participation has to be calibrated appropriately after paying due attention to sequential development of domestic markets.

Source:

BIS. 1999. “How Should We Design Deep and Liquid Markets? The Case for Government Securities.” Basel, October.

5.21 Finally, the development of related markets such as repo, futures and options also improves market liquidity of the government securities market by enabling participants to undertake hedging, arbitrage operations and speculative transactions. Repo transactions enable market participants to finance long positions and cover short positions. A well structured futures market reduces hedging costs and, thus, makes it easier to undertake cash transactions. An options market provides flexibility for hedging and arbitrage. 5.22 Central banks also impact liquidity of the government securities market through the various roles they perform. First, information on the policy decisions, release of data on various economic indicators and notification of open market operations (OMO) by central banks get incorporated into market prices. Second, as major market participants, central banks’ conduct of OMO using government securities affects supply of securities in the financial system. Third, central banks influence market liquidity by providing clearing and settlement services of government securities.

II. INTERNATIONAL EXPERIENCE

5.23 The government securities market has generally increased in size across countries in tandem with the growing financing requirements of Governments over the years. Notwithstanding the onset of fiscal consolidation processes and the consequent shrinking supply of issuances in the primary market in some countries in recent years, public debt managers have honed the development of the government securities market through various measures. Several Governments now raise funds through market-based mechanisms in a transparent and predictable fashion. They have also strived to broaden the investor base for the issuances of government securities. The Governments and central banks have adopted a strategy of jointly working with market participants to promote the development of the secondary market for government securities as also to establish sound clearing and settlement systems to handle transactions in government securities. While an abiding objective of public debt management in various countries has continued to be minimising the cost of government borrowings, a striking feature in the last two decades has been to pursue this objective with a focus particularly on managing risks inherent in the debt portfolio (IMF-World Bank, 2002).

Size and Liquidity of Government Securities Market

5.24 Historically, government securities markets grew with the need to finance government budget deficits. Since the 1970s, government securities markets in the United States (US) and in many other industrial countries underwent significant expansion in terms of size. Large fiscal deficits resulted in increased issuances of treasury bills and bonds. The US government securities market was, historically, the largest. However, as a result of fiscal consolidation in the 1990s, the government bond market shrank sharply in the US. On the other hand, the size of the Japanese Government Bonds (JGBs) market expanded substantially to about 150 per cent of GDP by 2005. In many other countries, including India, the size of the government securities market increased between 2000 and 2005 (Chart V.1).

5.25 Although the size continues to be a key determinant of liquidity of the government securities market, managers of public debt have pursued a strategy of keeping ‘trading liquidity’ sufficient even in countries where the size of issuances has shrunk in the primary market. Most studies analysing liquidity in the government securities market consider two measures of liquidity, viz., bid-offer or bid-ask spread and trading volume. Lower the bid-ask spread, lower is the transaction cost and hence, higher is the liquidity in the market. The bid-ask spread in the government securities market was one of the lowest in Japan, South Korea and Malaysia. In terms of the turnover ratio, the US treasuries market was the most liquid market in 2005, despite a fall in its size. The government securities market in the Peoples’ Republic of China (PRC) turned out to be one of the least liquid markets in terms of both the turnover ratio and the bid-ask spread (Table 5.1).

2 There are central banks which issue their own bonds, adding to the conflict between the monetary and fiscal policy operations and underlining the need for further coordination between the Ministry of Finance and the central bank. These instruments can also fragment the government bond market (Mohanty, 2001).

Management of Public Debt and Role of the Central Bank

5.26 The degree of involvement of central banks in the government bond market varies significantly across countries. At one end are countries such as Japan, the US, Australia, the UK (since 1998) and Republic of Korea, where the finance ministry solely decides the fiscal policy, government debt related issues and the course of operation of the government bond market. The Governments in these countries, however, co-ordinate with central banks, which may be independently pursuing monetary policy and selling/buying securities in the secondary market.2 At the other end are countries in which central banks, being statutory bodies under the jurisdiction of Ministry of Finance, operate in the government bond market at the behest of their Governments. For instance, in Malaysia, the central bank is one of the five statutory bodies under the Ministry of Finance. As a banker to the Government, it advises on the details of government securities issuances and facilitates such issuances through various market infrastructures that it owns and operates. Central banks in some countries assume twin responsibilities of conducting independent monetary policy and managing public debt. For instance, in Thailand, the central bank is responsible for monetary policy and developing the bond market for private and public saving and debt management. Hence, the monetary policy stance of the Bank of Thailand is set keeping in view certain objectives relating to fiscal deficit and future financing needs of the Government. The experiences of these countries indicate that the degree of independence of the central bank may be a necessary but not a sufficient condition for the development of the government bond market.

Table 5.1: Indicators of Liquidity in Domestic Currency Government Bond Markets – |

|

Select Countries - 2006 |

|

|

|

|

|

|

|

|

Country |

Generic term for

government securities |

Turnover |

Rank based |

Bid-ask spread |

Rank based on |

|

|

ratio |

on turnover ratio |

|

bid-ask spread |

1 |

2 |

3 |

4 |

5 |

6 |

Canada |

– |

4.0 *** |

7 |

5.00 * |

7 |

Japan |

Japanese Government Bonds |

6.0 |

6 |

0.58 |

1 |

US |

US treasuries

(Notes and Bonds) |

40.0 *** |

1 |

3.10 * |

5 |

Italy |

BTP |

10.8 ** |

3 |

6.00 * |

8 |

France |

OAT |

38.5 ** |

2 |

10.00 * |

10 |

Germany |

Bunds |

10.1 ** |

4 |

4.00 * |

6 |

Australia |

Commonwealth Government securities (CGS) |

9.0 *** |

5 |

– |

– |

UK |

Gilts |

9.0 *** |

5 |

4.00 * |

6 |

PRC |

Treasury bonds |

1.4 |

12 |

7.60 |

9 |

Korea |

Korea Treasury Bonds (KTB) |

2.6 |

8 |

1.30 |

2 |

Malaysia |

Malaysian Government securities (MGS) |

1.9 |

10 |

2.25 |

3 |

Thailand |

– |

1.7 |

11 |

3.00 |

4 |

Mexico |

CETES |

2.5 |

9 |

– |

– |

**, * and *** indicate data for 1997, 2002 and 2005, respectively.

– : Not available.

Source:

Ric Battelino (2004), Tomita (2002), Hattori et al (2001),

<www.adb.org>.; <www.asianbondsonline.adb.org>; and McCauley and Remolona (2000). |

5.27 The underlying objective of public debt management in various countries, regardless of whether the manager is the central bank or a government agency, continues to be minimisation of the cost of government borrowings. There has, however, been an increasing focus on management of risks in recent years. In particular, the debt management framework focuses on the need to undertake government borrowings at the lowest possible cost over a medium to long-term timeframe rather than taking recourse to risky debt structures, which may have lower costs in the short run but could be risky and trigger high debt servicing costs in the long run. At the same time, the Governments in some countries, which find the cost of issuing long-term securities at fixed rate very high, are opting for short-term securities while pursuing a strategy of developing the domestic debt market so as to reduce rollover risk and other market risks in the debt stock over time (IMF-World Bank, 2002).

Primary Market

Issuance Procedures

5.28 The issuance of government securities in countries, which are in the early stages of market development, is normally undertaken by way of discretionar y non-market placement such as underwriting by a syndicate of financial institutions. This route becomes preferable as free competition is impeded when there are fewer participants. In Korea, prior to the Asian crisis, a part of the bond issue was underwritten by some financial institutions and the Bank of Korea. The Bank of Korea, however, stopped underwriting government bonds from June 1998. The People’s Republic of China had adopted an underwriting syndicate system in 1991, which was abandoned in 1995 to make way for auctions. In Malaysia, government bonds are issued through auctions but they are also occasionally privately placed with specific financial institutions.

5.29 In cases where the government is uncertain about the full subscription to the issue and the price it would fetch, it may also ask the central bank of the country to underwrite a part of the fresh issue. In Malaysia, the central bank can participate in government bond auctions and can take up to 10 per cent of the total issue amount in order to obtain securities for market operations such as the repurchase agreements.

5.30 In order to improve the government securities market and to widen the investor base, it becomes essential for a country to move over time towards the market mechanism by way of competitive public auctions. Auctions are also used by some countries in combination with tap sales of securities. The Governments in most countries use pre-announced auctions to issue debt. The conventional auctions of government securities follow multiple-price auction system for issuances of conventional securities and uniform price auction system for securities with special features such as inflation-indexed bonds where there is market uncertainty (Box V.4). The US, however, has switched over to uniform price auction format so as to broaden its investor base as bidders tended to be more aggressive in this format due to a reduction in the ‘winner’s curse’. In 2000, the Korean Government moved to a uniform price auction format from multiple price auction system. Chinese treasury bonds are auctioned using the uniform price auction method. On the other hand, Thailand and Malaysia use multiple price auction for issuing government bonds. 5.31 Most Governments rely on underwriting syndicates for borrowings in foreign markets in order to help them price and place securities with foreign investors. This is because borrowings are usually not undertaken in sufficient volume or on a regular enough basis to warrant the use of an auction technique. For instance, smaller countries of the European Monetary Union (EMU) such as Portugal use syndications to launch first tranche of each new bond so as to have more control over the issue price and persify investor base to facilitate future issuances of government securities by the auction system.

5.32 There are also some countries such as Sweden and the UK, which raise foreign currency funds by issuing first domestic currency debt and then swapping it with foreign currency obligations. This technique has the added benefit of maintaining large issuances in the domestic markets even when domestic borrowing requirements are moderate. Large industrial countries such as the US and Japan issue only local currency denominated securities in their domestic markets and avoid raising funds offshore.

Transparency and Efficiency

5.33 Governments in most countries have become more transparent in their auction processes in the domestic market to reduce market uncertainty in the primary market and lower borrowing costs. Pre-announced borrowing plans and auction schedules enable the prospective investors to plan in advance their subscriptions to new issuances of government securities by adjusting their portfolios. The rules and regulations governing the primary auctions and the roles and responsibilities of primary dealers are disclosed well in advance to market participants. In Brazil and Poland, the Ministry of Finance disseminates the basic rules for issuances of government securities to market participants while the details of specific issuances are described in Letters of Issue placed on the website. While the Government in Poland announces the auction dates at the beginning of the year, in Brazil the dates are announced a month in advance.

5.34 The auction processes are also becoming more efficient through automation. The Governments in Ireland, Portugal and Jamaica are already using electronic auction system for issuance of securities, which has considerably reduced the time lag between the close of bidding and announcement of results.

Investor Base

5.35 Many countries such as Morocco and South Africa have moved progressively away from regulations that mandated investors to hold a prescribed portion of their assets in government securities. While the removal of such captive investor base may have increased interest rates to market-clearing levels in the short run, the ensuing deep and liquid government securities market in the medium to long-term is expected to reduce the debt service costs for the governments in future (IMF-World Bank, 2002). 5.36 Most countries have adopted a system of primary dealers (PDs) for ensuring that auctions are well-bid. PDs also act as a regular source of liquidity in the secondary market and provide useful information for managers of public debt on market developments and debt management issues. Some governments have felt the need to offer special privileges to PDs for promoting market development, especially at an early stage of development. As PDs continuously give two-way price quotes, they provide confidence to those who wish to buy or sell securities. Apart from the provision of liquidity to the market, the competition among PDs has facilitated efficient price discovery in the government bond market.

Box V.4

Auction Pricing – Uniform versus Multiple

Pricing in an auction can be on a multiple price basis (also called American auction or discriminatory price auction) or a uniform price basis (also called Dutch auction). In any auction, buyers typically submit bids that specify a quantity and a price (or a yield) at which they wish to purchase the quantity demanded. Once submitted, these bids are ranked from the highest to the lowest price (or from the lowest to the highest yield) and the quantity for sale is awarded to the best bids (i.e., highest prices or lowest yields).

Under the uniform price auction, each successful bidder pays the lowest price accepted by the debt manager, i.e., all the successful bidders will pay the same price, irrespective of their actual bid price. Under the multiple price auction, however, each successful bidder will pay the actual price at which he has bid (even if the cut-off price arrived at the auction may be lower). This results in ‘winner’s curse’, whereby successful bidders pay more than the common market value of the security after auctions. Uniform price auctions lead to a better distribution of auction awards. Under this system, the participants tend to bid more aggressively without fear of ‘winner’s curse’. This is because they will get the securities issued at the price quoted by the lowest accepted bid and not the actual that they have bid, unlike in the case of multiple price auctions. Hence, uniform price auctions are expected to enhance market efficiency. An important disadvantage of the uniform price system, however, is that of indiscriminate or irresponsible bidding which may be out of alignment with the market, as bidders are sure to succeed at the most favourable rate.

Under multiple or discriminatory price auctions, bidders get differential rates in accordance with their need and assessment of price. This is likely to ensure greater commitment to bidding than in the uniform system. The intensity of demand in the market is also clearly reflected in the bidding pattern.

An alternative to these two mechanisms that has been used in Spain since January 1987 is the so-called ‘Spanish auction’. It is a hybrid system combining the features of both the uniform-pricing and the discriminatory-pricing mechanisms. Under the Spanish auction system, winning bids that are above the weighted average winning bid will have to pay the same price, viz., the weighted average winning bid, as in a uniform-price auction. Winning bids that are below the weighted average winning bid will have to pay fully, as in a discriminatory-price auction.

By modelling auction behaviour, some researchers found that uniform price auctions are unfavourable to the issuer in terms of revenues, whether bidders are risk neutral or risk averse (Wilson, 1979). Some other researchers, however, found that discriminatory auctions yield unique equilibrium with greater expected revenues than the uniform auctions if bidders are risk neutral (Back and Zender, 1993 and Wang and Zender, 2002). Wang and Zender also found that uniform price auctions have a more favourable impact on revenue if the bidders are risk averse and the number of bidders are large in relation to the supply. Uniform price auctions are, however, found to permit self-enforcing collusive bidding strategies (Back and Zender, 1993), particularly under perfect information if buyers are allowed to communicate with one another before the auctions take place (Goswami, Noe and Rebello, 1996). Besides average revenue to the issuer, the choice of auction procedure may also affect the volatility of prices over time. Auction-to-auction volatility was found to increase significantly after the introduction of uniform pricing for select securities by the U.S. Treasury (Malvey, Archibald and Flynn, 1997). In the case of multiple price auctions, experiences indicate that volatility increases with the duration of assets (Sweden) and market uncertainty (Portugal) (Nyorborg, Rydqvist and Sundaresan, 2002 and Gordy, 1999). Experiments conducted on Spanish auctions show that both uniform and Spanish auctions raise significantly higher revenue than multiple price based auctions as the latter leads to less aggressive bidding than the other two. However, auction-to-auction volatility was higher both in uniform price and Spanish auctions compared to multiple price auctions (Abbink, Brandts and Pezanis-Christou, 2002). Thus, empirical evidence about the superiority of one type of auction over the other seems inconclusive. Cross-country experience shows that although both the methods are used, securities are mostly auctioned using discriminatory auction method.

5.37 In the US, PDs (though not designated as market makers), in existence from 1966, serve as a source of market intelligence to the Federal Reserve. They work with the Federal Reserve to develop a healthier treasury market. In the UK, a system of PDs or Gilt-Edged Market Makers (GEMM) has been in existence since 1986. These act as market makers, par ticipate in gilt auctions held by the Debt Management Office (DMO), give two-way quotes facilitating the secondary market activity in gilts and provide market information to the DMO. Similarly, in Malaysia and the Republic of Korea, the system of PDs as market makers was introduced in 1988 and 1999, respectively. In the Peoples’ Republic of China, there are two segments of the secondary market for government bonds, viz., the inter-bank market and the stock exchange market. A market making system in the inter-bank market has been established since 2004. Certain commercial banks and securities firms have been assigned the task of providing two-way quotes for government bonds.

5.38 Some industrial countries such as Denmark, Japan and New Zealand do not have a system of PDs. The IMF-World Bank survey reported that the abolition of the PD system had significantly reduced the Government’s borrowing costs in one particular country. In the case of some developing countries with small government securities market and a few participants, the preference is to let the market participants decide their own market makers. Even in large industrial countries, such as the US, the auction system is not restricted to PDs alone. Other market participants are allowed access as well, provided they have a payment system in place to facilitate settlement of auction obligations. Thus, each country needs to weigh the benefits of the PD system against the costs. The trade-off between the two is likely to depend on the state of market development.

5.39 In addition to banks, institutional investors such as employees’ provident funds and pension funds have also become important participants in the government bond market in several countries. Government bonds in Malaysia were, in fact, developed to cater to the investment needs of such institutions. In Australia, contractual institutions and even banks were given heavy tax incentives for investing in government bonds in the early phase of development. Institutional investors have normally a long-term horizon and hence, they can be a major source of investment in government (particularly infrastructure related) bonds. However, as a result of their long-term investment horizon, most of these institutions are ‘buy and hold’ investors, which can impede liquidity in the market.

5.40 Captive market arrangements that are adopted in some countries include mandating certain institutional investors, such as banks or contractual saving institutions, to hold a certain percentage of their assets in government bonds. Such arrangements also prevent investors from trading in government securities. Most developed countries, in the course of their market development, have discontinued any form of mandated investment in government bonds.

In OECD countries investments in government bonds are no longer mandated. However, in some developing countries, captive market arrangements continue to exist. For instance, in the People’s Republic of China, investment funds are subject to a mandatory 20 per cent investment in government bonds.

5.41 Retail investors do not make a significant contribution to trading activity in the market but as long-term investors, they impart stability to the market. Thus, many countries have drawn retail investors to broaden the market. For instance, the Japanese Government launched special Japanese Government Bond (JGB) issues in 2003 and 2006 exclusively for retail investors (floating and fixed rate) with tenor, rate and other features suiting their requirements. This instrument is available with banks and post offices. Brazil also began issuing securities to small investors over the Internet in January 2002.

5.42 Countries have also increasingly relaxed foreign participation in auctions of government securities. Among the developing countries, foreign ownership of government bonds is permitted in Malaysia, the Republic of Korea and Thailand. In the People’s Republic of China, foreign investors (institutional or individual), barring foreign institutional investors holding the Qualified Foreign Institutional Investors license, are not allowed to invest in government bonds.

Instrument Development

5.43 The profile of government securities differs across countries in terms of (i) maturity; (ii) ways of fixing coupon and principal payment; (iii) methods of coupon and principal settlement; and (iv) investor orientation. An analysis of evolution of various instruments in the government bond markets shows that normally countries in the nascent stage of development of government bond markets preferred to concentrate exclusively on simple and standardised instruments. Over the years, they moved towards a mix of conventional and, more advanced and complex instruments. The instrument development has become increasingly more sensitive to various risks associated with trading in government bonds.

5.44 Most of the government securities markets in developed countries are characterised by instruments with tenors ranging from short to long-term. For instance, the US treasuries market primarily offers two types of conventional government bonds, viz., treasury notes (maturing between two and 10 years) and bonds (with maturity of 10 years or above) with a semi-annual coupon or interest payment. The 10-year treasury note, the most traded US treasury security, is taken as an indicator of the government debt market in the US. The 30-year bond was reintroduced by the US government in 2006. In the UK, conventional government securities or gilts, with tenors of 5, 10 and 30 years, constitute the largest share of liabilities of the UK Government. It reintroduced the issue of its ‘ultra-long’ 50-year gilt in 2005. The Japanese Central Government issues JGBs with maturity ranging from 2 to 5-year (medium-term), 10-year (long-term), 15-year (floating), 20-year and 30-year fixed bonds (super long-term). 5.45 Generally, medium and long-term bonds issued by various Governments carry a fixed coupon rate. The rate of interest paid on such bonds is fixed at the time of issue. For instance, all medium, long and super-long JGBs, except the 15-year JGBs, are fixed interest rate instruments. The 15-year JGB is a floating rate instrument, the coupon rate of which is aligned to a reference rate plus a constant spread and varies in line with the changes in the reference rate. Value of fixed interest securities falls when the market rate of interest rises. The value of a floating interest bond, however, remains constant even in the face of a rise in the market rate of interest because its coupon payments also rise. This helps in mitigating interest or market risk. Given its less risky nature, the Governments initially issue securities with floating interest rates. As the market develops, however, the Governments move towards fixed interest rate long-term securities. Floating rate instruments have, historically, been used by some of the developed countries to lengthen the maturity of government debt (IMF-World Bank, 2001).

5.46 Inflation-indexed bonds have gained prominence over floating rate instruments as a better hedge against inflation. The UK introduced index linked gilts in 1981, followed by the issue of capital indexed bonds by Australia in 1985.3 The UK also issued a 50-year ‘ultra-long’ inflation indexed gilt in 2005. Canada, the US, France, and most recently, Japan have been some of the other countries from the developed world, which have started the issue of inflation-indexed bonds. Japan issues an inflation-indexed JGB only with one term, i.e., 10 years. The US issues treasury inflation protected securities (TIPS) and Canada issues real return bonds. In index-linked bonds, either both coupon and principal payment (as in the UK) or just the principal (as in Japan) are adjusted for changes in inflation. An adjustment for inflation is particularly beneficial in the case of long-term government bonds, as the risk of variation in price levels of such bonds is high. Most countries have been slowly moving towards the international best practice of a three-month indexation lag between the publication of the consumer price index information and the actual indexation of the bond as against an eight-month lag earlier.

5.47 The rationale behind issuing inflation-indexed government bonds by the developed countries is to enable the Governments to reduce borrowing costs by avoiding the need to compensate investors for the inflation uncertainty premium that exists in nominal bonds. Also, if the market for inflation-indexed securities is liquid and reasonably stable, then the spread between nominal and inflation-indexed yields of government debt can serve as a useful indicator of expected inflation for central banks in the conduct of monetary policy. Most countries, however, have found it difficult to develop a liquid secondary market for inflation-indexed government securities, implying that the yields paid by the Governments may include a premium to compensate investors for liquidity. The Governments in some developing countries have also introduced inflation-indexed bonds. Unlike the developed countries, however, the objective of introducing such bonds in the developing countries is to extend the yield curve.

5.48 Under the system of separate trading of registered interest and principal of securities (STRIPS), the interest and principal can be traded separately as zero coupon bonds, which help in improving liquidity and widening the investor base of the government securities market. Furthermore, STRIPS can also be reconstituted into a bond. As market participants constantly check the price of stripped bonds with the conventional bonds, strip bonds enable better pricing of traditional coupon bonds. The US began stripping of designated treasury securities in 1985. The UK introduced stripping of conventional fixed coupon in 1997, followed by Japan in 2003 for designated book entry securities. In the US, STRIPS are not issued by the Government directly. They are registered as book entry securities by the Government but are created by financial sector entities such as banks. In the UK, anyone can trade or hold STRIPS but only a market maker (Gilt Edged Market Maker), Debt Management Office (DMO) or Bank of England can strip a strippable gilt or reconstitute it.

3 The Australian capital indexed bonds, however, have been discontinued since 2003.

5.49 Most Asian countries such as South Korea did not rely significantly on government bonds prior to the Asian financial crisis. With deterioration of the fiscal position in the post-crisis period, the South Korean Government had to resort to heavy issue of bonds in order to bring the economy back on the path of recovery. This necessitated strengthening of the government bond market infrastructure. Initially, the Korean Government simplified a number of instruments that were earlier traded by converting them all into treasury bonds.4 In the Korean treasury bonds market, bonds with medium-term maturity, viz., three and five years have emerged as the benchmark bonds. Furthermore, Korea has allowed stripping of Korean Treasury Bonds (KTBs). In Thailand, the issuance of domestic government bonds dates back to 1933, though the market remained largely underdeveloped. After the Asian crisis, which highlighted the importance of the bond market, the Government started issuing bonds in large quantum to recapitalise the ailing banking sector in the economy.5 Thai government securities are issued as fixed rate coupon bonds or interest accumulated bonds and have a maturity profile of one to 10 years. However, there is little persity in the range of instruments available in the government bond market. Consequently, the Bank of Thailand is now in the process of developing inflation indexed bonds and STRIPS (zero coupon bonds). The Malaysian Government Securities (MGS) were, historically, issued to meet the investment needs of employees’ provident fund. By the 1990s, the Government began to use them as tools for financing part of its budget deficit. MGSs are coupon bearing instruments with a maturity period varying between three and 20 years. Coupon payments are made once in six months. In the People’s Republic of China, the need to develop the government bond market was seriously recognised when the overdrawing facility from the People’s Bank of China was discontinued in 1994. Treasury bonds in the People’s Republic of China, apart from treasury bills (with less than one year maturity), include fiscal bonds, special purchase bonds, construction bonds and inflation proof bonds (where principal is linked to the price index). These bonds are issued by the Chinese Government. Construction bonds are issued to raise funds for certain projects, while special purchase bonds are issued to pension fund and unemployment insurance funds for employees in the domestic enterprises. The Government of the Republic of China (Taiwan) also introduced STRIPS with a maturity of five years in 2005.

Benchmarking and Consolidation

5.50 Several governments have progressively strived to minimise the fragmentation of the government debt stock by creating a limited number of benchmark securities at key points of the yield curve. They generally use conventional government paper devoid of embedded options for this purpose. Typically, benchmark securities are constructed by issuing the same security in several auctions (‘reopenings’) and by repurchasing, prior to maturity, older issues that are no longer actively traded in the market. In Brazil, Denmark, Ireland, New Zealand, South Africa, Sweden and the UK, where domestic borrowing requirements are modest or have generally declined over time as a result of fiscal surpluses, debt managers have repurchased securities which are no longer actively traded in order to maximize the size of new debt issues. This has enabled them to minimise the fragmentation of debt and concentrate market liquidity in a small number of securities, thereby ensuring active trading even though the total debt stock may be declining. Denmark, Sweden and the UK also offer market participants a facility to borrow temporarily or obtain by repo, specific securities that are in short supply in the market though at penal rates so that the government securities market is not affected by the pricing distortions in the market. South Korea also has a system of fungible or reopened issues of KTBs, wherein on-the-run bonds issued over a certain period of time are given the same maturity and coupon rate. In the UK, the Debt Management Office (DMO) has recently introduced the conventional gilts with aligned coupon dates in order to facilitate fungibility between coupon STRIPS of various types of gilts. The US also permits such fungibility of coupon STRIPS, irrespective of the underlying US treasury bond but not of principal STRIPS.

Consultation with Market Participants

5.51 Many countries have adopted a consultative approach for developing the government securities market by maintaining an active investor relations programme. Under this programme, managers of public debt meet the major market participants regularly to discuss the funding requirements of the Government, market developments and devise ways to develop the primary market. Such programmes have proved useful, especially for countries managing their public debt under stress. For instance, public debt managers in South Africa operate an investor relations programme and conduct road shows to meet investors, PDs and other market participants for explaining developments in the South African government securities market and explain to them developments in government finances.

4 The Government converted various types of instruments, viz., Public Funds, Foreign Exchange Stabilisation Fund Bonds (FESFBs) and borrowings from funds like Post Office Deposits to Treasury Bonds.

5 These bonds were issued through the Financial Institutions Development Fund (FIDF).

Secondary Market

5.52 The secondary market for government securities provides a platform for original investors to trade their holdings before maturity. Traditionally, the trading platform was over-the-counter (OTC) before introduction of trading in stock exchanges in various countries. For instance, in China, trading in treasury bonds was banned till 1980. Subsequently, an OTC trading was initiated. Trading at the Shanghai Stock Exchange commenced in 1992. Banks trade in the inter-bank market, which is largely a repo and ‘buy and hold’ market. Since 1997, banks in China have been prohibited from trading in stock exchanges to avoid speculation. In Thailand, the Thai Bond Market Association began trading in government bonds in 1998. The central bank of Malaysia operates the centralised data base on Malaysian debt securities, i.e., Bond Information and Dissemination System (BIDS), which facilitates OTC trading of government bonds in Malaysia.

5.53 The public debt managers actively work with market participants and others to improve the secondary market for government securities through a system of intermediaries, a broad investor base and an efficient clearing system. For instance, Italy, Poland, Portugal, Sweden and the U.K. have worked closely with the market to introduce electronic trading in government securities. In Thailand, the Bond Electronic Exchange (BEX), a subsidiary of a stock exchange, began trading in government bonds in 2005. Furthermore, Italy has sought to work with the concerned participants to alleviate distortions caused by the tax treatment of returns on government securities. The debt mangers in Japan, New Zealand, South Africa and the U.K. have also jointly worked with market participants to develop ancillary markets such as futures, repo and STRIPS. These have helped in deepening the government securities market. 5.54 The managers of public debt also work with the relevant stakeholders to devise sound clearing and settlement systems for government securities markets. For instance, Brazil, Japan and Poland introduced real time gross settlement system (RTGS) for government securities transactions. The authorities in Jamaica are also working with market participants to dematerialise government securities within the central depository in order to increase efficiency of secondary market trading.

Market practices

5.55 Market practices have also been liberalised in many countries to improve liquidity in the secondary market of government securities.

Short Selling

5.56 Short selling is now permitted in many countries. For instance in Australia, a seller is allowed to sell securities to a purchaser without having the right of transfer of the ownership.6 In the US, as part of the legal requirement, the seller needs to confirm a broker the delivery of the shorted securities. In the People’s Republic of China, short selling of treasury bonds takes place in the Shanghai and Shenzhen stock exchanges through a repurchase agreement. Short selling is restricted to less than one year and is not allowed at the traditional OTC exchange of treasury bonds. In Malaysia, the right of short selling MGS, but in a covered way, has been given to all inter-bank participants, which include commercial banks, finance companies, merchant banks and discount houses registered under the Banking and Financial Institutions Act. However, there are restrictions on the type of securities that can be sold short and the extent to which the seller can take a short position.

‘When issued’ Trading of Government Securities

5.57 Trading of government securities between the time a new issue is announced and the time it is actually issued is generally called ‘when issued’ (WI) (or ‘when as and if issued’ in the US) trading. It works like future trading of securities where long and short positions are allowed prior to the issue date of the securities. The trading of WI is on a yield basis as coupon is determined only after the auction. WI trading facilitates price discovery and helps in improving liquidity in the government bond market. Furthermore, it substantially brings down the risk of underwriting. The restrictions on WI trading were removed by the US Treasury on treasury notes and bonds in the 1970s. Japan, however, considered WI trading as illegal until recently. Following the guidelines laid down by the Japanese Securities Dealers Association (JSDA) regarding the exact definition and legal perspectives of the WI trading of JGBs, WI trading of JGBs took shape in Japan in 2004. In Malaysia, the date of announcement of a primary issue is done on Fully Automated System for Issuing/Tendering (FAST) and the issue is opened for WI. The WI issues are automatically processed through FAST. The date of settlement of WI trades is within two business days after the issue date.

6 Short selling involves benefiting from the fall in price of a security. If the price of a security is declining, one can borrow a security in order to sell it, expecting that it would decline further, and then buy it at a lower price and make delivery. The difference between the sale and purchase price of the security is the profit. It involves four steps, viz., an investor borrowing a stock, selling that stock, then 'closing' his position by buying the stock and then returning it back to the lender. If the price falls, he makes a profit, otherwise a loss.

Risk Management

5.58 Although government bonds are free from credit risk, they are subject to market or interest rate risk. In the case of foreign currency bonds, they also carry exchange rate risk. Market participants have traditionally hedged market risks by trading in government bond futures. In futures trading, participants can hedge their positions, because they can fix prices at which the trade would settle in future. Development of futures has been instrumental in raising the trading turnover of physical securities in several countries.

5.59 In Australia, development of government bond futures was a part of the reform measures relating to the bond markets adopted in the 1980s. The Australian futures market has become the most active futures market for trading in fixed interest government bonds, particularly of three-year and 10-year maturities. Trading in Japanese Government Bonds (JGBs) futures began with a 10-year security in 1985, which has become one of the largest traded futures in the world. The Tokyo Stock Exchange introduced trading in options of JGB futures in 1990. The Republic of Korea introduced government bond futures in 1999. The two types of bond futures currently available in Korea are of 3-year and 5-year maturity. Similarly, Malaysia too has futures contracts on three-year, five-year and 10-year MGSs. The derivatives on treasury bonds in the People’s Republic of China, were earlier introduced in 1993. However, their trading was discontinued in 1995 due to excessive speculation and lack of knowledge about controlling the risks involved in such trading. In September 2005, the Chinese Securities Regulatory Commission (CSRC) declared that it would work towards the introduction of futures and other derivative products in the Chinese securities market.

5.60 The Governments are becoming increasingly aware of the need to manage financial and operational risks of their debt portfolio. The framework used to trade-off expected costs and risks in the debt portfolio differs across countries. Many countries use simple models based on deterministic scenarios, while only a few (Brazil, Denmark, Columbia, New Zealand and Sweden) use stochastic simulations. Several countries also use stress testing as a means to assess the market risk in the debt portfolio and robustness of different issuance strategies. Many of them adopt cash flow modelling for analysing costs and risks for associated debt issuance structures, whereby debt-service costs and their volatility in the medium to long-term are assessed. The rationale for this technique is that the cost of debt is best considered in terms of its impact on the Government’s budget, and that cash flow measures are a natural way of quantifying this impact. Risk is typically measured as the potential increase in costs resulting from financial and other shocks.

5.61 Some countries have adopted the asset-liability management (ALM) approach in a limited way by analysing the risk characteristics of government financial assets and debt jointly to determine the appropriate structure of debt and assets. The public debt management offices in many countries are addressing management of operational risk by putting in place a formal institutional framework. Middle offices are involved in analysing risk and designing as well as implementing risk control procedures. These debt offices are also trading their debt or taking tactical risk positions.

Development of Payment and Settlement System for Government Securities

5.62 Countries are striving for an efficient payment and settlement system of government securities transactions so as to reduce the market risk, default risk and systemic risk. The settlement system has migrated from the physical mode to the dematerialised mode, wherein securities are recorded in electronic book entry form. Several countries are now moving towards electronic trading of government securities. Countries have also introduced the DvP mechanism which ensures that delivery occurs if and only if payment occurs and vice versa. This settlement system has replaced designated-time net settlement system whereby only the net payment/receipt amounts were settled at a certain designated time by a RTGS system. These steps have virtually eliminated the settlement risk.

5.63 In many countries, which have adopted electronic transfers of government securities, central banks have been instrumental in providing a clearing and settlement platform for government securities. This is true even in those countries in which the central bank does not operate as the debt manager to the Government. For instance, the Reserve Bank of Australia has adopted the Reserve Bank Information and Transfer System (RITS) from the 1980s. DvP was introduced in the RITS in 1991. All operators in the market are members of the RITS and they use this system for settling transactions in government bonds. RITS has also been linked to the RTGS. Japan introduced DvP for JGBs in 1994 in its payment and settlement system, Bank of Japan NET (BOJ NET). It linked the BOJ NET JGB service and BOJ NET fund transfer system. Japan moved to RTGS in 2001. The securities in the UK are held in demat form and are transferred electronically on the basis of DvP through the settlement system operated by CREST, which is the central securities depository for UK gilts and Irish securities. The Bank of Thailand, which acts as a registrar and depository of Thai government bonds, restructured the Bank of Thailand Automated High Value Transfer Network (BAHTNET), the electronic settlement platform, to facilitate RTGS and DvP in government bonds in 2001. In the Peoples’ Republic of China, the Government Securities Trading System and People’s Bank of China’s large-value payment system were interconnected in 2004, making way for DvP settlements in the inter-bank bond market.

5.64 The Joint Task Force of the Committee of Payment and Settlement System (CPSS) and the Technical Committee of the International Organization of Securities Commissions (IOSCO) in its report released in 2001 recommended that countries adopt a rolling settlement, wherein the final settlement was not to exceed T+3 days.7 The report urged the countries to ultimately strive towards the same day settlement. Among the developed countries, the settlement cycle for outright sales is T+1 in the US and the UK and T+3 in Japan.

5.65 To sum up, international experience of various aspects of government securities markets shows some differences across the countries in terms of structure, instruments, trading and settlement practices, and risk management system. Nevertheless, some common lessons could be drawn. One, the development of the government securities market across the yield curve may entail some short-term costs as the governments move away from a purely captive market to a persified investor base in the medium to long-term. Two, debt issuance needs to be done in a predictable manner using standardised instruments so that the issuer’s behaviour doesn’t disrupt market activity. Three, a demonstrated commitment to develop the government securities market enhances the liquidity and reduces the costs of government borrowings.

5.66 A select cross-country review showed a mixed picture. In several countries, the function of issue and management of public debt no longer rests with central banks. This is more so in countries that have developed debt markets and where government debt issuance is not dominant. In many other countries, central banks continue to be debt managers for the government. However, in almost all countries central banks do play a vital role in developing the infrastructure for trading and settlement of government securities in the secondary market. They are regulators of PDs, who act as market markers for government securities. Furthermore, central banks have been instrumental in developing payment and settlement systems for government securities, which have contributed significantly towards an efficient and secure trading in government securities.

III. GOVERNMENT SECURITIES MARKET IN INDIA – POLICY DEVELOPMENTS