[Under Section 45ZL of the Reserve Bank of India Act, 1934] The fortieth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held during December 5-7, 2022. 2. The meeting was attended by all the members – Dr. Shashanka Bhide, Honorary Senior Advisor, National Council of Applied Economic Research, Delhi; Dr. Ashima Goyal, Emeritus Professor, Indira Gandhi Institute of Development Research, Mumbai; Prof. Jayanth R. Varma, Professor, Indian Institute of Management, Ahmedabad; Dr. Rajiv Ranjan, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Michael Debabrata Patra, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely: -

the resolution adopted at the meeting of the Monetary Policy Committee; -

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and -

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting. 4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail the staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (December 7, 2022) decided to: - Increase the policy repo rate under the liquidity adjustment facility (LAF) by 35 basis points to 6.25 per cent with immediate effect.

Consequently, the standing deposit facility (SDF) rate stands adjusted to 6.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 6.50 per cent. - The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 6. The global economic outlook is skewed to the downside. Global growth is set to lose momentum as monetary policy actions tighten financial conditions and as consumer confidence weakens with the rising cost of livelihood. Inflation remains elevated and persistent across countries as they grapple with food and energy price shocks and shortages. More recently, however, there are some signs of moderation in price pressures, which have raised expectations of an easing in the pace of monetary tightening. Alongside easing in sovereign bond yields, the US dollar has come off its highs. Capital flows to emerging market economies (EMEs) remain volatile and global spillovers pose risks to growth prospects. Domestic Economy 7. On the domestic front, real gross domestic product (GDP) increased by 6.3 per cent year-on-year (y-o-y) in Q2:2022-23 after an increase of 13.5 per cent in Q1. On the supply side, gross value added (GVA) rose by 5.6 per cent in Q2. 8. In Q3, economic activity is exhibiting resilience. In the agricultural sector, a pick-up in rabi sowing (6.4 per cent higher than a year ago on December 2) is supported by the good progress of the north-east monsoon and above average reservoir levels. Activity in the industry and services sectors is in expansion mode, as reflected in purchasing managers’ indices (PMIs) and other high frequency indicators. 9. Aggregate demand conditions have been supported by pent-up spending and discretionary expenditures during the festival season, although their evolution is somewhat uneven across sectors. Urban demand has remained buoyant, and rural demand is recovering. Investment activity is in modest expansion. Merchandise exports contracted in October after an expansion for 19 consecutive months. Growth in non-oil non-gold imports decelerated. 10. CPI inflation moderated to 6.8 per cent (y-o-y) in October 2022 from 7.4 per cent in September, with favourable base effects mitigating the impact of pick-up in price momentum in October. Food inflation softened, aided by easing inflation in vegetables and edible oils, despite sustained pressures from prices of cereals, milk and spices. Fuel inflation registered some easing in October, driven by softening of price inflation in LPG, kerosene (PDS) and firewood and chips. Core CPI (i.e., CPI excluding food and fuel) inflation persisted at elevated levels at 6 per cent, with price pressures across most of its constituent sub-groups. 11. The overall liquidity remains in surplus, with average daily absorption under the liquidity adjustment facility (LAF) at ₹1.4 lakh crore during October-November as compared with ₹2.2 lakh crore in August-September. On a y-o-y basis, money supply (M3) expanded by 8.9 per cent as on November 18, 2022 while bank credit rose by 17.2 per cent. India’s foreign exchange reserves were placed at US$ 561.2 billion as on December 2, 2022. Outlook 12. The inflation trajectory going ahead would be shaped by both global and domestic factors. In case of food, while vegetable prices are likely to see seasonal winter correction, prices of cereals and spices may stay elevated in the near-term on supply concerns. High feed costs could also keep inflation elevated in respect of milk. Adverse climate events – both domestic and global – are increasingly becoming a significant source of upside risk to food prices. Global demand is weakening. Unabating geopolitical tensions continue to impart uncertainty to the food and energy prices outlook. The correction in industrial input prices and supply chain pressures, if sustained, could help ease pressures on output prices; but the pending pass-through of input costs could keep core inflation firm. Imported inflation risks from the US dollar movements need to be watched closely. Taking into account these factors and assuming an average crude oil price (Indian basket) of US$ 100 per barrel, inflation is projected at 6.7 per cent in 2022-23, with Q3 at 6.6 per cent and Q4 at 5.9 per cent, and risks evenly balanced. CPI inflation for Q1:2023-24 is projected at 5.0 per cent and for Q2 at 5.4 per cent, on the assumption of a normal monsoon (Chart 1). 13. On growth, the agricultural outlook has brightened, with the prospects of a good rabi harvest. The sustained rebound in contact-intensive sectors is supporting urban consumption. Robust and broad-based credit growth and government’s thrust on capital spending and infrastructure should bolster investment activity. According to the RBI’s survey, consumer confidence is improving. The economy, however, faces accentuated headwinds from protracted geopolitical tensions, tightening global financial conditions and slowing external demand. Taking all these factors into consideration, the real GDP growth for 2022-23 is projected at 6.8 per cent with Q3 at 4.4 per cent and Q4 at 4.2 per cent, with risks evenly balanced. Real GDP growth is projected at 7.1 per cent for Q1:2023-24 and at 5.9 per cent for Q2 (Chart 2).  14. Inflation has ruled at or above the upper tolerance band since January 2022 and core inflation is persisting around 6 per cent. Headline inflation is expected to remain above or close to the upper threshold in Q3 and Q4:2022-23. It is likely to moderate in H1:2023-24 but will still remain well above the target. Meanwhile, economic activity has held up well and is expected to be resilient, supported by domestic demand. Net exports would remain subdued due to the drag from evolving external demand conditions. Further, the impact of monetary policy measures undertaken needs to be watched. On balance, the MPC is of the view that, further calibrated monetary policy action is warranted to keep inflation expectations anchored, break the core inflation persistence and contain second round effects, so as to strengthen medium-term growth prospects. Accordingly, the MPC decided to increase the policy repo rate by 35 basis points to 6.25 per cent. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. 15. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to increase the policy repo rate by 35 basis points. Prof. Jayanth R. Varma voted against the repo rate hike. 16. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted against this part of the resolution. 17. The minutes of the MPC’s meeting will be published on December 21, 2022. 18. The next meeting of the MPC is scheduled during February 6-8, 2023. Voting on the Resolution to increase the policy repo rate to 6.25 per cent | Member | Vote | | Dr. Shashanka Bhide | Yes | | Dr. Ashima Goyal | Yes | | Prof. Jayanth R. Varma | No | | Dr. Rajiv Ranjan | Yes | | Dr. Michael Debabrata Patra | Yes | | Shri Shaktikanta Das | Yes | Statement by Dr. Shashanka Bhide 19. The official estimate of year-on-year real GDP growth in Q2: FY 2022-23 at 6.3 per cent equals the September 2022 forecast by RBI. Although the YOY growth in Q2 is well below 13.5 per cent registered in Q1, it reflects a strong sequential momentum with QOQ growth at 3.6 per cent. Private Final Consumption Expenditure, Gross Fixed Capital Expenditure and exports of goods and services have shown sequential expansion over Q1. However, going forward, the growth scenario would be affected adversely by the slowing global growth even as growth-supportive policy measures provide new opportunities in the economy. 20. A review of wide range of indicators of the recent economic activity point to a mixed outlook for growth. The Index of industrial production (IIP) for September 2022, the latest month for which data are available, increased by 3.1 per cent YOY basis. However, the pattern has been uneven across sectors and also over time. In August the growth was negative after a modest growth of 2.2 per cent in July. IIP Consumer Non-durables declined in July, August and September, while it was negative in August and September for Consumer Durables. Gross Value Added from manufacturing and industry as a whole declined in Q2: FY 2022-23 and rose for Services. Value of merchandise exports declined in October by 12.1 per cent in US$ terms, after a sharp deceleration in Q2. Services exports have expanded YOY basis in October but declined relative to September. 21. On the positive note, IIP for Capital Goods and Infrastructure, and Construction registered acceleration on YOY basis in September. Purchasing Managers’ Index for manufacturing and services remained in expansion zone in October and November 2022. Although non-oil non-gold merchandise imports declined in October over September, they remained above the level in the same period in the previous year. GST collections registered YOY double digit growth in October and November. Non-food credit growth was high, averaging 17.6 per cent during September-November. 22. The qualitative indicators from the RBI’s surveys of urban households for September and November 2022 point to a gradual improvement in sentiments relating to overall economic conditions, employment and income. Increased consumer spending is supported by ‘non-essential’ items, with an expected improvement in sentiments for ‘discretionary’ spending only on one-year ahead basis. 23. While the economic activity levels moving into Q3: FY 2022-23 suggest resilience, outlook is, however, faced with the slowing global growth conditions. The global growth outlook has deteriorated since the last meeting of the MPC in late September. The IMF in its October 2022 World Economic Outlook projects a decline of world output growth YOY basis from 6.0 per cent in 2021 to 3.2 per cent in 2022 and 2.7 per cent in 2023, with downside risks to projections. The external demand conditions and capital flows to EMEs may weaken as a consequence. As the causes of the global growth slow down include the impact of COVID 19 related issues in China and the Ukraine war, besides the monetary policy tightening measures across countries, the outlook is also affected by the risk of high energy and food prices as their supply chains get disrupted. 24. Taking into account the trends in key exogenous global and domestic conditions, the revised real GDP growth rate, YOY basis, for FY 2022-23 is 6.8 per cent with Q3 and Q4 at 4.4 and 4.2 per cent, respectively. The revised growth rate for FY 2022-23 is lower by 20 basis points from the projections provided in the September MPC meeting. The GDP growth rate for FY 2023-24 is projected at 7.1 per cent for Q1 and 5.9 per cent for Q2. 25. The YOY CPI inflation moderated to 6.8 per cent in October from 7.4 per cent in September, with decline of 140 basis points in food inflation and 50 bps in fuel & light. The core inflation, based on CPI components excluding food and fuel remained at 6 per cent. The MOM momentum of prices, however, remained high. The headline CPI increased by 0.8 per cent in October over September, contributed by significant month-over-month increase in all the major components of CPI. 26. The general upward pressure on inflation may be attributed to incomplete transmission of previous input price hikes even as overall demand conditions show gradual improvement. The successive supply side shocks affecting the costs and prices beginning with the rising input and energy prices, food prices and strengthening US dollar may not have been fully offset by the rising selling prices in all sectors. The Wholesale Price Index (WPI) inflation, a measure of producer level prices, dropped to single digit (8.4 per cent) in October 2022 for the first time after a run of double-digit annual increase since April 2021. WPI YOY inflation for manufactured products category as a whole has been in single digits since June 2022 although for many energy items, the inflation rate remains in double digits. Declining profitability of firms seen in the corporate performance in Q2: FY 2022-23 in the manufacturing sector is one indication of the inability to recover all the cost increases fully. 27. The RBI Inflation Expectations Survey of Households in urban areas conducted in November indicates a drop in the median perceived headline inflation rate in November 2022 compared to September. The expectations of inflation rate three-month ahead and one-year ahead have also moderated in November compared to the expectations in September. However, the decline follows an upturn experienced in September and accordingly, the moderation of CPI inflation in October may have influenced the current household expectations. The Business Inflation Expectations Survey conducted by the Indian Institute of Management Ahmedabad1 points to a reduction of one-year ahead inflation based on unit costs to less than 5 per cent in August and September 2022, although 45 per cent of the respondents continue to see the one-year ahead inflation rate at 6 per cent or above. The survey has also reflected a declining pattern of one-year ahead CPI inflation rate. 28. Taking into account the current trends in both domestic and international commodity prices and their major determinants, the CPI inflation rate for the full current financial year has been retained at 6.7 per cent, the same level as in the September meeting. The projections of CPI inflation rate for Q2 and Q3 are at 6.6 and 5.9 per cent, respectively. The projected YOY inflation rates for Q1 and Q2 of 2023-24 are also below 6 per cent. The median headline inflation rate projected by the RBI survey of Professional Forecasters conducted in November 2022 is at 6.6 per cent for Q3: FY 2022-23 and 6.1 per cent for Q4: FY 2022-23, with 6.7 per cent for the financial year as a whole. 29. With overall domestic growth showing signs of resilience, the adverse global macroeconomic conditions require that domestic inflation rate is at moderate levels, within the tolerance band of the inflation target on a sustained basis. The persistence of core inflation at the upper limit of the tolerance band of the inflation target is of particular concern. Slippage on both growth and inflation objectives together would be a poor outcome. Keeping in view the need to achieve moderation in the inflationary pressures in a sustained manner, continuing with the monetary policy tightening measures is necessary at this stage. 30. Accordingly, (1) I vote to increase the policy repo rate by 35 basis points and also (2) I vote to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Statement by Dr. Ashima Goyal 31. Multiple global risks continue but as a growth slowdown threatens many countries, inflation and rate actions of major central banks are also slowing. While continuing to talk tough, even the US Fed has recognized the importance of monetary lags and of responding to economic and social developments. There is a view that since US long-term inflation expectations remain at 3 per cent, the ex-ante real rate is already restrictive. 32. Markets have priced in a possible pivot, although communication shocks continue to create volatility. The dollar is weakening especially as other advanced economy central banks also raise rates. The worst of the adjustment seems past. India saw a return of inflows in July, a few months before the reversal in other emerging markets (EMs) in November—indicating confidence in India’s outperformance. FX reserves are rising again. Large rupee depreciation is unlikely to add to inflation pressures in the months ahead. 33. Global commodity prices have softened. The index for Indian supply chain pressures has been falling since May 2021. It is now below the long-period average. The impact is visible in the sharp fall in India’s WPI. That this is falling without a substantial pass through to CPI, suggests that firms have not raised prices to the extent of input cost pressures. This may be partly due to soft demand and cost-saving measures, and hopefully the beginnings of the realization that cost shocks are temporary if the inflation target is working to anchor expectations. The IIM Ahmedabad business inflation expectation survey shows moderation in cost pressures and in sales, while one year ahead inflation expectation remains below 5%, although profit margins are expected to rise with the fall in costs. The gap between PMI input and output prices has almost closed for manufacturing while it has fallen significantly from its May peak levels for services. Good sowing despite extended rains is lowering food prices. 34. In core inflation the contribution of transport and communication is reducing, as is another dominant component, clothing, after cotton prices peaked in August. Persistence is due to multiple supply shocks more than to second round effects. RBI inflation forecasts are based on the assumption of the Indian crude oil basket at $100 but India’s current basket is ruling much below this level. Although domestic pass-through is yet to happen, downside risks to inflation are high. 35. Indian exports and manufacturing output are slowing with global demand; that imports are also decelerating, even with only about 60% pass through in fresh loans, suggests domestic demand is also shrinking. Anecdotal evidence indicates small firms are finding it too expensive to invest. Their contribution is necessary to reverse the investment slowdown of the last decade, to prevent future bottlenecks and rise in costs and to build export and employment capacity. India has excess non-oil imports partly because this capacity was not built in the last decade. 36. Inflation targeting anchors inflation if policy rates rise one for one with expected inflation, so the expected real rate is positive and close to the equilibrium rate. Second, lagged transmission of higher policy rates lowers demand. The MPC has made sure of the first and the second is in process. 37. The average inflation projection for the next four quarters is 5.7% and in Q2FY24 it is 5.4%. So the real policy rate is positive and will rise through the year. Since there are many factors working to chill demand, policy has to be careful in adding to these. Multiple estimations show that through the demand channel of transmission, Indian interest rates affect output first and inflation less and only with long lags. 38. Moreover, interest rate spreads in the Indian system are high. While the yield spread of investment grade G-secs over hard currency sovereign yields averaged 200bps for emerging markets2; the Indian 10 year G-sec spread over the US 10 year is about double this (rates were 7.21% compared to 3.5% on December 1). The 3 month commercial paper rate is above 7%. Higher spreads imply a larger demand reducing effect of a rise in the policy repo rate. Pass through to loan rates is also faster with the external benchmark for loan rates. 39. At present, however, Indian imports are still too high. A sticky terms of trade shock lowers potential output, requiring demand to fall. In addition, inflation still exceeds the MPC tolerance band for the 10th consecutive month. So I vote to raise the repo rate by 35bps to 6.25%. I would have preferred a smaller rise of 25bps, but 6.25% works well as a focal rate. 40. Other instruments are available, apart from a demand contraction, to attain a more sustainable current account deficit (CAD). These include export promotion, building domestic capacity and reducing dependence on oil imports. India’s remittances and software exports remain robust and the transition to a green economy is progressing well. Rising share of financial savings will also reduce the CAD. There are also multiple financing options for the CAD. 41. Since India does not have full capital account convertibility, the uncovered interest parity (UIP) relation that says nominal domestic interest rates must equal US nominal rates plus expected rupee depreciation does not hold in its pure form. Standard advice based on the UIP is a way to force other countries to follow US policy. They must either raise domestic rates with Fed rates to prevent depreciation; or under inflation targeting let the currency depreciate then raise rates as inflation rises. But this is the way to aggravate foreign shocks. 42. India has the space to suit policy to domestic needs and has done better because it has used it. Capital flow management and intervention has successfully prevented excess depreciation. Reserves are rising again. The interest gap is larger for longer periods and in real terms3. For short rates prudential measures such as reducing banks’ open position limits can be used if necessary, without following US rate hikes. 43. Coming to the stance, withdrawal of accommodation was alright as long as the large liquidity surpluses and excessive rate cuts of pandemic times persisted. But durable liquidity seems to have contracted so much that the LAF system has not been able to compensate for liquidity shocks during the last two months. The call money rate has exceeded the repo rate for much of the time. It is time to move to a neutral stance, where movement can be data-based in any required direction, as new information affects forward projections. Accordingly, I vote against the part of the resolution on remaining focused on the withdrawal of accommodation. 44. An EM faces large liquidity shocks, especially as major countries go in for quantitative tightening. The LAF system has made much progress and should be able to prevent excessive short-term liquidity tightening. If shocks are too large adequate surplus should be created in durable liquidity. An inflation targeting regime itself provides the inflation anchor; the anchor is not money or liquidity supply. 45. In response to market volatility after the Truss budget, the Bank of England has shown how clear communication can separate the market-making from the monetary policy function of liquidity. While market-making may be required in AEs with high leverage and under-regulation of the non-bank financial sector, in India it can be used to ensure financial conditions are able to support the creation of credit even as repo rates rise. Financial regulation and balance sheets have strengthened, lending is risk-based, corporates have de-leveraged. It is time for a reversal of the credit drought of the last decade. Statement by Prof. Jayanth R. Varma 46. Since the September meeting, the balance of risks has shifted decisively away from inflation to growth both globally and domestically. There are now clear signs that the global supply side shocks emanating from the pandemic and the Ukraine war are finally receding. The strongest signal is the sharp fall in crude prices in the second half of November. Global inflation seems to have peaked and is now probably heading lower. Added to this is the fact that it is only over the next few quarters that the real economy will experience the full brunt of the front-loaded tightening by central banks across the world. All in all, there is much reason to be optimistic about global inflationary pressures easing. 47. In this context, I would like to point out that the RBI’s inflation projections (as well as that of some professional forecasters surveyed by the RBI) are still based on the assumption of an average crude price (Indian basket) of $100. This is about 15-20% higher than the Brent crude futures curve at the time of this meeting. Perhaps, these forecasters believe that the Brent futures market is unreliable due to various behavioural biases. But an assumption so sharply at deviance from liquid market prices needs to be justified on the basis of economic and geopolitical fundamentals. In mid-November, the futures market appears to have reassessed the geopolitical pulls and pressures on OPEC in the light of observed political outcomes. If the forecasters disagree with this reassessment, they need to articulate and justify their alternative narrative. In the absence of such articulation, one could be pardoned for suggesting that the $100 Brent crude assumption reflects the well known behavioural biases of salience and conservatism. 48. On the domestic front also, there is strong evidence of easing of inflationary pressures. The pricing power of producers appears to have eroded dramatically as reflected in the sharp reduction in corporate profitability. Inflation has eased from the 7%+ levels witnessed in the middle of the year, and more importantly inflation expectations of both households and businesses have trended down. 49. On the other hand, growth concerns have become more troubling in recent months both globally and domestically. Financial markets are pricing in the likelihood of a recession in several advanced economies. During the pandemic, exports and government spending were the two growth engines that counteracted the headwinds confronting the Indian economy. Of these, the global slowdown has already led to the export growth engine grinding to a halt. Fiscal constraints limit the ability of government spending to hold up the economy on its own. Private investment is unlikely to be able to pick up the slack. Anecdotal evidence suggests that concerns about future growth prospects are deterring capital investment even by companies that have reached more than 80% capacity utilization. That leaves only private consumption which has remained buoyant, but it remains to be seen how much of this is due to pent up demand which could dissipate over the coming months. All of this means that economic growth is now extremely fragile and definitely not robust enough to withstand excessive monetary tightening. 50. I believe that the 35 basis point rate hike approved by the majority of the MPC is not warranted in this context of reduced inflationary pressures and heightened growth concerns. I therefore vote against this resolution. 51. Turning to the stance, my views are the same as in September when I argued for a pause. Because monetary policy acts with lags, it may take 3-4 quarters for the policy rate to be transmitted to the real economy, and the peak effect may take as long as 5-6 quarters. The MPC has raised the repo rate by 225 basis points in about eight months. Accounting for the fact that in 2021 money market rates were close to the reverse repo rate (65 basis points below the repo rate), the full magnitude of monetary tightening would be 290 basis points. Much of the impact of this large front-loaded monetary policy action is yet to be felt in the real economy. For these reasons, I believe that 6.25% itself very likely overshoots the repo rate needed to achieve price stability, and poses an unwarranted risk to economic growth. The majority of the MPC is saying that they intend to tighten even more by withdrawing accommodation. This stance would be even more damaging to the fragile growth outlook and I therefore vote against this resolution also. Statement by Dr. Rajiv Ranjan 52. In these uncertain and difficult times, monetary policy making is a daunting task. Achieving and maintaining credibility4 – a valuable asset for any central bank – is still a bigger challenge. In the quest to rein in inflation while supporting growth, central banks are, therefore, confronted with an important decision of ‘how fast, how far and how long’5 the ongoing tightening phase should continue. While entailing difficult trade-offs, these choices and its combinations, as would be eventually decided upon by the central banks, remain vital and would set the tone for the world economy in the ensuing year. Some central banks have already started considering a pivot towards slower pace and lesser quantum of rate hikes or taking a pause on the tightening cycle. 53. India is no different. There are several forces at work. One has to consider not only evolving domestic growth and inflation dynamics, while also accounting for related factors like cumulative tightening and its impact, lags in transmission, unexpected global and domestic shocks, the terminal rate itself, among others. Moving slowly and doing too little could lead to macroeconomic instability with the unhinging of inflation expectations which, more importantly, may warrant stronger actions later that could be much more detrimental than the costs of overtightening.6 On the contrary, doing too much could hurt growth. Conventionally, monetary policy credibility varies endogenously with the policy pursued and a non-gradualist approach leads to enhanced credibility, can bring faster disinflation that entails lower sacrifice ratio (Sargent, 1986; Ball, 1994).7 These outcomes are, however, subject to several rigidities and irrationality that may result in larger growth sacrifice. Therefore, monetary policy needs to be watchful depending upon evolving macroeconomic signals in balancing between gradualism and acting too fast, too soon. 54. As I had indicated in my statement of September 2022, there was a close call between increasing the policy repo rate by 35 bps or 50 bps. After frontloaded rate hikes since May 2022, there is a strong case now to take the foot off the accelerator while keeping a sharp vigil on the inflation trajectory. Moreover, with inflation trajectory panning out broadly along anticipated lines and also, considering the ongoing pass-through of earlier monetary policy actions and the evolving growth-inflation dynamics, monetary policy response can be calibrated to a lesser order. Thus, an increase of 35 bps is felt appropriate at the current juncture, while also continuing with the stance of withdrawal of accommodation, and I vote for the same. Any change in stance at this stage could be interpreted as weakening of our resolve to fight the inflation menace and will impede monetary policy transmission. The objective is to ensure a sustained disinflation that brings inflation down within the tolerance band in the short-run and closer to the target over the medium term, while supporting growth. These decisions are premised on the following considerations. 55. Though there has been moderation in inflation by 60 bps in October, certain underlying trends need to be closely watched. First, price momentum in October was at the highest level since May 2022 and has also showed a sequential increase since August 2022. Second, core (CPI excluding food and fuel) inflation remains sticky at 6 per cent, with its momentum in October being the highest since April 2022, even on a seasonally adjusted basis. In fact, deflation in petrol and diesel has masked the full extent of inflationary pressures in core. Excluding petrol and diesel, transportation and communication inflation was at 7.7 per cent. Trimmed mean measures of inflation remained elevated. Third, there is evidence of continuing generalisation of price pressures, especially in core. Diffusion indices for CPI headline and core continued to show strong expansion in prices across the CPI basket. These factors suggest persistent price pressures, which along with geo-political tensions and adverse climate events adds to uncertainty, warranting a continuation of calibrated monetary policy action. 56. Growth, on the other hand, remains resilient with drag coming mainly from net exports. Faster reopening of China, signs of deceleration in inflation in US and easing global commodity prices are tailwinds which may limit the downside to the world demand in 2023. From our perspective, signs of peaking of US dollar appreciation with lower crude prices, despite news of early reopening in China, are strong positives. Though lower crude prices would not help inflation immediately8 due to unchanged petrol and diesel pump prices as under-recoveries of Oil Marketing companies (OMCs) continue, but will help external sector balance with lower imports, which already is showing sign of tapering. Importantly, the trend in the momentum of the major components of GDP is assuring. For instance, the momentum of real GDP in Q2:2022-23 has been robust at 3.6 per cent as against pre-pandemic (2012-13 to 2019-20) average of 0.9 per cent; similarly, the two main drivers of GDP – private consumption and investment – recorded a momentum of 1.0 per cent and 3.4 per cent, respectively, in Q2, as against negative pre-pandemic average momentum for Q2 [(-)0.1 per cent and (-)1.4 per cent, respectively, during 2012-13 to 2019-20)]. On the supply side, a strong rebound in contact-intensive services (trade, hotels, transportation, communication and others) with a momentum of 16.0 per cent (as against pre-pandemic average momentum of (-)1.6 per cent during 2012-13 to 2019-20) underpinned the growth in real GVA in Q2. 57. The discussion on terminal rate in monetary policy is clouded by the uncertainty on the strength and direction of growth and inflation impulses. In this scenario, the important point to note is that the terminal rate is time varying and has to be discovered based on incoming data and evolving situation. With the rate hikes done so far, and considering the inflation outlook, it can be said with certainty that real rates have moved decisively towards positive territory, yet one cannot be sure of the same if one uses the realised current inflation argument, which is fast gaining ground under uncertain conditions.9 Ensuring monetary conditions and stance are appropriately calibrated to current growth-inflation dynamics is crucial as bank deposit and lending rates in real terms are much lower than pre-pandemic levels. 58. Overall, monetary policy geared towards price stability while taking into account output dynamics is the best guarantee to ensure lasting prosperity. Besides, in all probability, growth concerns globally and in India may assume primacy in 2023 as the global economy slows down on the back of tightening financial conditions even as global supply chains get restored and input cost pressures ease from current levels. Statement by Dr. Michael Debabrata Patra 59. Recent data arrivals point to a pick-up in seasonally adjusted momentum of real GDP growth into positive territory in the second quarter of 2022-23. Notably, this improvement has occurred on the strength of domestic drivers that overcame the contraction in net exports. Projections indicate that positive momentum will likely be sustained through the rest of the year. It remains to be seen if the strength of that momentum is able to offset strong, pandemic-induced unfavourable base effects. For 2023-24, a tempering of the pace of real GDP growth relative to this year’s rate needs to be factored in, given warnings of global slowdown and hence a rising drag from net exports for India; still muted domestic private investment in spite of capacity utilisation having crossed trend levels in a number of industries; and, tightening financial conditions. 60. On the other hand, inflation in India remains unconscionably elevated, persistent and generalised, despite a grudging let-up in October solely due to favourable base effects. The momentum of price increases was, in fact, the highest since May 2022. Core inflation remains unyielding and diffused, with a rising price momentum as it tests the upper tolerance band on its own, warranting resolute monetary policy resolve to quell it. Evolving global inflation movements juxtaposed with our projections would suggest that India’s headline inflation may ease slightly through the rest of the year. The effects of monetary policy actions taken so far, supported by improvements in supply responses, could break the 7 per cent plus drift in average headline inflation and at best contain it in the range of 5-6 per cent over the year ahead. Thus, inflation can be expected to remain above target over the next 12 months. 61. The longer inflation stays at current levels, the greater is the danger of expectations getting unhinged, frittering away the moderation reported in the most recent surveys of households, businesses and professional forecasters. The risk of inflation eroding purchasing power and weakening consumer spending, especially on discretionary items, is becoming significant. Inflation expectations may also be stalling private investment in capacity creation, as reflected in corporate performance during the second quarter of 2022-23. 62. Accordingly, further withdrawal of accommodation is warranted to re-balance aggregate demand against supply conditions and return inflation first into the tolerance band and then to alignment with the target. This is essential for sustaining the positive turn in the momentum of growth. 63. The size and pace of further increases in the policy rate should take into account this inflation objective. It is also necessary to incorporate the effects of cumulative rate increases undertaken so far, the transmission to longer-term rates achieved so far, the movements in real interest rates, and the ongoing impact on macroeconomic and financial conditions as they evolve. Accordingly, a modest reduction in the size of the policy rate increase in this meeting would provide the opportunity to weigh that assessment carefully. 64. Should the incoming information indicate that the recent small easing of inflation is transient rather than the onset of a durable downturn, the MPC should be prepared to respond appropriately in order to achieve the desired inflation objective. In essence, the MPC needs to see a decisive decline in inflation over a series of monthly readings before it shifts stance, which would otherwise be premature. 65. I vote for an increase in the policy rate by 35 basis points and a stance that remains focused on the withdrawal of accommodation. Statement by Shri Shaktikanta Das 66. Amidst headwinds from slowing global growth and trade, the Indian economy is exhibiting resilience and holding up well. Real GDP growth at 6.3 per cent in Q2:2022-23 was on the lines expected by us. Incoming information for Q3 indicates that economic activity remains strong. Living as we are in an interconnected world, we cannot remain entirely decoupled from adverse global spillovers. External demand is weakening and this is having its negative impact on our exports. Overall, India’s real GDP is expected to grow by 6.8 per cent in 2022-23 and India will remain amongst the fastest growing major economies, even as rising recession possibilities characterise the global economy. 67. Headline inflation is moderating, albeit slowly. While the worst of inflation is behind us, it remains above the upper tolerance level. It is expected to decline in H1:2023-24 but would still be well above the target. Uncertainties surrounding the inflation trajectory remain sizeable, given the geopolitical tensions, global financial market volatility, pending pass-through of input costs to domestic output prices and weather-related disruptions. Core inflation (CPI excluding food and fuel) is exhibiting persistence around 6 per cent for the past few months. Hence, there is no room for complacency and the battle against inflation is not over. This necessitates a constant vigil on prices. 68. Our successive rate actions since May 2022 are working through the system. Considering the elevated inflation levels, especially the stickiness in core inflation, further calibrated monetary policy action is warranted to contain build-up in underlying inflationary pressures, keep inflation expectations anchored, and bring inflation closer to the target rate of 4 per cent over the medium term. This would strengthen the medium-term growth prospects of the Indian economy. 69. I am, therefore, of the view that a premature pause in monetary policy action would be a costly policy error at this juncture. Given the uncertain outlook, it may engender a situation where we may find ourselves striving to do a catch-up through stronger policy actions in the subsequent meetings to ward-off accentuated inflationary pressures. I, therefore, vote for an increase of 35 basis points in the repo rate – a departure from 50 bps on three previous occasions – which itself conveys the signal of an improvement in the inflation outlook. 70. Considering the prevailing policy repo rate, liquidity conditions and the expected trajectory of inflation over the next several months, it is essential to persist with the stance of withdrawal of accommodation. Hence, I vote for the same. 71. To conclude, let me add that in a tightening cycle, especially in a world of high uncertainty, giving out explicit forward guidance on the future path of monetary policy would be counterproductive. This may result in the market and its participants overshooting the actual play out of real conditions. In such circumstances, it would be prudent to keep Arjuna’s eye on the evolving inflation dynamics and be ready to act as may be necessary. Monetary policy has to be nimble to address any emerging risk to the price stability, while keeping in mind the objective of growth. (Yogesh Dayal)

Chief General Manager Press Release: 2022-2023/1420

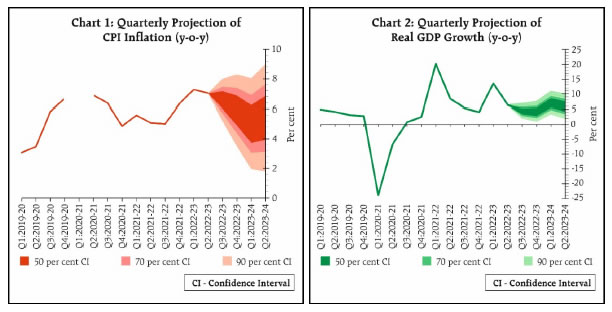

|